Global| Jul 31 2017

Global| Jul 31 2017Unemployment Drops Are Widespread and Persistent in EMU

Summary

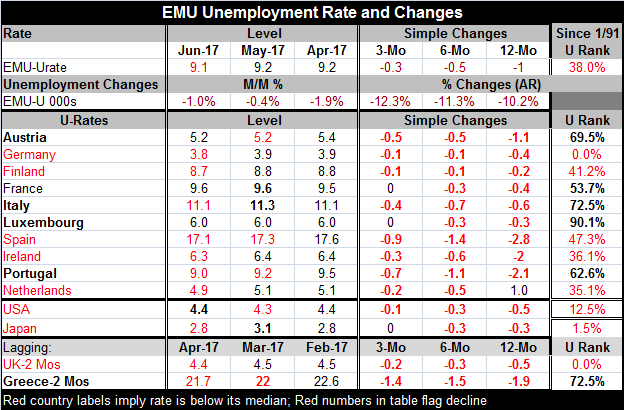

Unemployment in the EMU area fell in June and fell across a very broad front. Of the ten original EMU members that report June unemployment levels in this table, seven show unemployment declines in June, with none showing increases [...]

Unemployment in the EMU area fell in June and fell across a very broad front. Of the ten original EMU members that report June unemployment levels in this table, seven show unemployment declines in June, with none showing increases and three showing an unchanged unemployment rate. Over three months, eight of ten show unemployment rate declines, with only France and Luxembourg unchanged. Over six months, all show declines. Over 12 months, nine out of ten show declines with the Netherlands an exception as its rate is higher by 1 percentage point over 12 months.

Unemployment in the EMU area fell in June and fell across a very broad front. Of the ten original EMU members that report June unemployment levels in this table, seven show unemployment declines in June, with none showing increases and three showing an unchanged unemployment rate. Over three months, eight of ten show unemployment rate declines, with only France and Luxembourg unchanged. Over six months, all show declines. Over 12 months, nine out of ten show declines with the Netherlands an exception as its rate is higher by 1 percentage point over 12 months.

Global progress as well

All this unemployment rate declining is joined by the U.S., Japan, Greece and the U.K. as each of them also shows unemployment declines over three months, six months and 12 months with the Japan being the only exception as its unemployment rate over three months is only unchanged. For Greece and the U.K., we use the most recent unemployment data which involves a 2-month lag. Still, their rates on that timeline are declining broadly and consistently as well.

Unemployment rate declines accompanied by steadier inflation

In addition to the falling unemployment rates, inflation in the euro area remained unchanged in June at 1.3% although core inflation (excluding unprocessed food and energy) which had been lower upticked on the month to join the headline at a 1.3% pace. The combination of steady inflation and uptick in the core with a widespread unemployment rate drop in progress provides a solid back ground for the ECB to open the doors of its methadone clinic for monetary policy stimulus-addicted economies in the euro area. Of course, inflation is still well short of its policy goal, but here we are only looking for the ECB to begin to pare back its asset purchases gradually rather than to actually begin to hike rates. That is still a ways off. However, if economic progress like this continues, more eyes will focus on how close inflation is getting to 'target' and fewer will dwell on the fact that it is still a bit short of target. Even though inflation is the only actual mandate of the ECB, we know that the bank looks more broadly at the economy's needs as it sets policy. Central bankers don't wear blinders. Mario Draghi certainly has not.

The good and the bad

The EMU economy is making progress. The EMU unemployment rate has fallen to its lowest level since 2009 and the German rate is now at a new post-reunification low; there are also some very positive things to say about unemployment rate levels throughout the euro area. For all of the EMU, the unemployment level has been lower only 38% of the time since 1991. Germany and the U.K. (the latter, soon to be an EU independent economy) are all at lows on this timeline. The Netherlands, Ireland, Spain, Finland, the U.K. and Germany all have unemployment rates below their respective medians for this period (Spain at a 47th percentile standing by a small margin). France has its unemployment rate above its median by a small margin as its rate has a 53.7 percentile standing (50% is the place-setting for its median). The countries with still relatively high unemployment rates (above their medians since 1991) are (besides France) Portugal, Austria, Italy and Luxembourg. Greece is also high on lagging data; it is above its median with a 72.5 percentile standing.

The policy issues

Despite the very solid momentum and progress on unemployment in the EMU and the fact that there is so much progress in the largest economies that helps to move the markers forward for the EMU as a whole, there is a notable group of countries (five to seven here) with unemployment rates barely at or below their respective medians or still above their medians for whom taking the foot off the gas pedal may not be a popular decision. As with the U.S., there is still the question of what happens to growth if the degree of stimulus is reduced. That is to ask the question of how much the ongoing stimulus is really responsible for the degree of growth and economic progress we currently are witnessing. Is it a large proportion or not? If the stimulus is taken away, will the growth progress continue on a broad front? If there is a transition to rate hikes and to normalize rates, how much would growth be impacted? These are the hypothetical questions to which no one knows the answers and on which policymakers' judgement will ultimately turn.

Despite the fact that economic recovery is still substantial and seemingly impressive on a weighted EMU overall basis, there remains a group of countries trailing on this progress. I do not any more expect that to stop the ECB from shifting gears.

Getting ready

The ECB will probably press ahead with some small degree of policy change for several reasons. Countries in the lagging group are themselves still making progress. Some EMU members are getting really nervous about waiting so long to shift gears. There are some members ready to change policy regardless of short-term economic outcomes. But the ECB has not yet made up its mind although it will in a few months when it revisits the issue of the appropriateness of policy in September. If these trends are still in play, expect the ECB to start peeling back the layers of stimulus that Europe has become accustomed to. It is still true that money and credit growth in the EMU remain on very low growth profiles. The ECB at this point could consider current conditions to support arguments to stay the course or to begin to peel back stimulus. The policymakers public comments make it seem as though they are more ready not to begin to follow in the U.S. footsteps, albeit slowly and carefully rather than to dither any longer.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief