Global| Dec 17 2009

Global| Dec 17 2009UK Retail Sales Take A Sett Back In November But Cling To Trend Rise

Summary

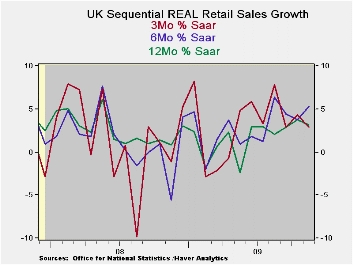

UK retail sales volumes fell by 0.3% in November after having rise in October. Sales volumes have risen twice in the last three-months and seven times in the last 12-months. The three-month rate of growth has dipped below the six- [...]

UK retail sales volumes fell by 0.3% in November after having

rise in October. Sales volumes have risen twice in the last

three-months and seven times in the last 12-months.

The three-month rate of growth has dipped below the six-month

rate of growth but still exceeds the 12-month growth pace. Clothing and

footwear sales, however, are clearly losing momentum having dropped in

the last three months. Retail ex-auto sales are off from their six

month pace but nearly even with their 12-month pace.

In the new quarter, Sales are growing at a pace of 3% to 3.5%.

That should help to underpin Q4 GDP growth.

In a separate report, the CBI survey of the distributive

trades produced diffusion results saying that November sales were flat

with those in October. That of course is more ambitious that the sales

count from National Statistics (above). The outlook in the CBI

framework was negative, however.

A poll of UK inflation expectations found that expectations

were stuck at 2.4% for the third consecutive quarter. While this is

above the BOE ceiling pace for inflation (of 2%) the Bank has admitted

that there would be some temporary overshoot to which it will not

respond. It is heartening that as inflation has risen in the UK,

inflation expectations have not. BOE credibility seems to be well

intact despite the damage done in the financial crisis.

| UK Real and Nominal Retail Sales | Quarter | |||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Nov-09 | Oct-09 | Sep-09 | 3-MO | 6-MO | 12-MO | YrAGo | 2-date |

| Retail Total | -0.3% | 0.5% | 0.4% | 2.9% | 4.0% | 2.6% | 2.0% | 3.2% |

| Food Bev & Tobacco | 0.2% | 0.2% | 0.1% | 2.3% | 2.2% | 3.4% | 7.3% | 2.5% |

| Clothing footwear | -2.0% | 1.5% | 0.4% | -0.7% | 1.5% | 1.4% | -1.7% | 0.3% |

| Real | ||||||||

| Retial Ex auto | -0.4% | 0.6% | 0.4% | 2.9% | 5.3% | 3.1% | 0.8% | 3.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief