Global| Dec 11 2008

Global| Dec 11 2008UK Industrial Sector Still Under Great Pressure

Summary

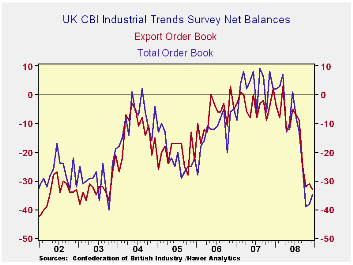

The chart above tells the story for UK manufacturing. The bottom fell out in Sept, then in Oct and Nov., things got worse and now negative conditions are remaining in force at levels near the bottom of their recent range. Orders stand [...]

The chart above tells the story for UK manufacturing. The bottom fell out in Sept, then in Oct and Nov., things got worse and now negative conditions are remaining in force at levels near the bottom of their recent range. Orders stand in the 4th percentile of their range (since 2000); they remain very weak. The volume index for the outlook is at a raw reading of -42, the lowest since 2000. On a broader front going back to 1988 the volume outlook index has been weaker than this only 3% of the time. Stocks are at the top of their range since 2000 but the same stocks number is in the top 9% of the data going back to 1988 – inventories by any comparison are top-heavy.

The orders and export order weakness also look low in broader comparisons. Orders are weaker than this only 15% of the time and foreign orders are weaker 26% of the time in data going back to 1988.

To combat weakness The UK has embarked on a stimulus plan. That plan came under attack today from German Finance Minister Steinbruck who characterized British stimulus as ‘breathtaking’ calling it ‘crass Keynesianism.’ In France , economy minister Lagarde was urging the EU to do more to stimulate the region as she warned that the slowdown could get much more severe. Lagarde says France is working and Germany is thinking, pointing out that different countries have different approaches while being much less confrontational than Steinbruck overall. In this environment it is Germany that is doing so much less and it is Germany that is the outlier much more than the UK .

| UK Industrial volume data CBI Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Reported: | Dec 08 |

Nov 08 |

Oct 08 |

Sep 08 |

Aug 08 |

12MO Avg | Pcntle | Max | Min | Range |

| Total Orders | -35 | -38 | -39 | -26 | -13 | -9 | 4% | 9 | -40 | 49 |

| Export Orders | -33 | -31 | -32 | -25 | -9 | -10 | 17% | 3 | -38 | 41 |

| Stocks:FinGds | 21 | 25 | 24 | 21 | 18 | 14 | 100% | 25 | -2 | 27 |

| Looking ahead | ||||||||||

| Output Volume:Nxt 3M | -42 | -42 | -31 | -16 | -13 | -2 | 0% | 28 | -42 | 70 |

| Avg Prices 4Nxt 3m | 0 | 10 | 23 | 31 | 34 | 24 | 55% | 34 | -19 | 53 |

| From end 2000 | ||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief