Global| Jul 20 2006

Global| Jul 20 2006UK GDP: Unexpected Pick-Up in Q2 Growth

Summary

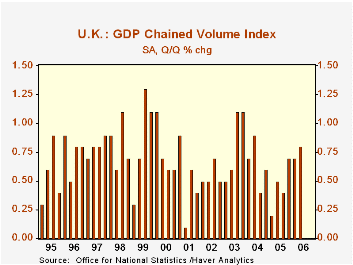

GDP growth in the UK ticked up to 0.8% in Q2 from 0.7% in Q1. The initial report of Q1 in late April was 0.6% so interim revisions were upward, with history also somewhat stronger than was thought at that time. This "preliminary" [...]

GDP growth in the UK ticked up to 0.8% in Q2 from 0.7% in Q1. The initial report of Q1 in late April was 0.6% so interim revisions were upward, with history also somewhat stronger than was thought at that time.

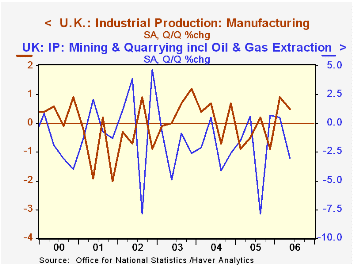

This "preliminary" estimate is compiled from industry data only. The full array of income and expenditure data will be published August 25. Among the sectors, today's report shows that, after a surge in Q1, production industries fell back by 0.1%. This was concentrated in the mining sector (including oil and gas extraction), where output was off 3.0% in the quarter and in energy supply, down 2.8%. However, manufacturing advanced 0.5%; although this was less than in Q1, it added enough to put that sector up 0.7% over a year ago, its first year-on-year increase since Q4 2004.

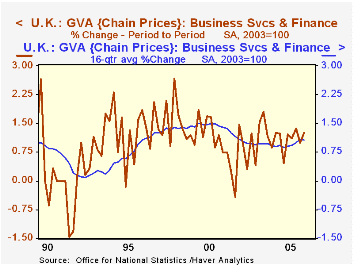

The real source of growth was the services, particularly business and financial services. Total services expanded 1.0%, with business services up 1.2%. This latter industry group is up 4.8% from a year ago. Consumer-oriented services, such as distribution, hotels & restaurants and repairs also gained 1.2% in Q2, yielding 3.3% growth over the past year. Transportation and communications are up 3.0% on the year and government and "other", 2.5%.

We are slightly surprised at this pick-up in UK growth. Just a little over a week ago, we wrote here about employment patterns that were no better than "stable", accompanied by rising unemployment. News reports this morning indicated that forecasters in a widely watched survey had projected 0.7%, the same as Q1, suggesting that our qualitative judgment was hardly unique. The flatness in production was evident from previously available production data for April and May. Just yesterday, retail trade data for the quarter showed strength (2.1%), but that, of course, is only one industry. As we mentioned last quarter, growth in Q1 was widespread across industries, giving the benefits of diversity to the economy as a whole. So this period, when production industries and mining tailed off, service businesses kept up the total.

| United Kingdom (Chained, SA, 2002=100) |

Q2 2006 | Q1 2006 | Q4 2005 | Year/ Year | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| GDP* | 0.8 | 0.7 | 0.7 | 2.6 | 1.9 | 3.3 | 2.7 |

| Production Industries | -0.1 | 0.8 | -0.6 | -0.8 | -1.8 | 0.7 | -0.3 |

| Service Industries | 1.0 | 0.7 | 1.1 | 3.6 | 2.8 | 3.9 | 3.1 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief