Global| Oct 21 2005

Global| Oct 21 2005UK GDP Rises 0.4%, Helped by Upturn in Manufacturing

Summary

UK GDP grew 0.4% in Q3, according to Office of National Statistics "Preliminary Estimate", following 0.5% in Q2. This early estimate is compiled from industrial production and other industry data. It shows that manufacturing gained [...]

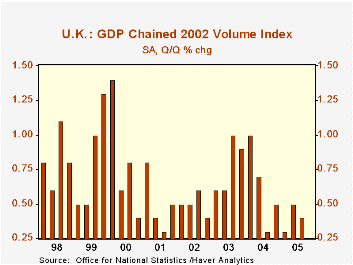

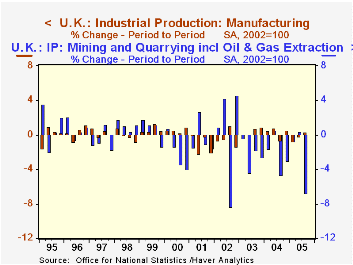

UK GDP grew 0.4% in Q3, according to Office of National Statistics "Preliminary Estimate", following 0.5% in Q2. This early estimate is compiled from industrial production and other industry data. It shows that manufacturing gained 0.3% on the quarter, after Q2's 0.2% decrease. Services maintained their 0.6% quarterly pace for a third straight time. Mining, including oil and gas extraction, and utility output, both of which had been supports in Q2, fell by significant amounts in Q3, 6.7% and 1.8%, respectively.

The upturn in manufacturing was generated by a number of largely unrelated sectors. Wood products, petroleum output and electrical and optical equipment, for examples, all turned up after Q2 declines. Nonmetallic minerals stabilized after a steep decline and rubber and plastics have been virtually flat for about six months. Food and textiles fell in Q3 after rising in Q2. Thus, it's hard to characterize the performance of manufacturing as a whole and therefore to look for any sustaining force -- one direction or the other.

Another sign of precariousness in these UK data comes from a look at the revisions for Q2 compared with its "preliminary" estimate. Three months ago, when we wrote about the Q2 preliminary report, we noted the support from the mining sector, but also that recent irregular downtrends there suggested that the 1.4% gain reported then might be transitory. Indeed. The growth there has now been revised to just 0.4% and the sector resumed a long-term contraction in this latest quarter. This change shouldn't be much of a surprise in this industry. But the broad manufacturing sector also seems to be subject to transitory forces. Already seen above to have a scattered performance reported so far for Q3, the sector experienced a notable revision of Q2 data. As seen in the table below, the "preliminary" Q2 report showed a 0.7% decline, which now has been recalculated at just 0.2%. This is a favorable revision, of course, but at the same time, it points out the skittishness in these data. The analysts at the UK Office of National Statistics include a warning in their press release about the preliminary GDP data, expressing their concern that users put too much store in the preliminary figures. Our examination here describes a couple of good reasons we might agree with that sentiment and suggests that caution is needed as business planners and investors apply them to decision-making and actions.

| United Kingdom: | Q3 2005 "Prel" | Q2 2005Year/Year | 2004 | 2003 | 2002 | ||

|---|---|---|---|---|---|---|---|

| Latest | "Prel" | ||||||

| GDP | 0.4 | 0.5 | 0.4 | 1.6 | 3.2 | 2.5 | 2.0 |

| Manufacturing | 0.3 | -0.2 | -0.7 | -0.1 | 1.9 | 0.1 | -3.1 |

| Mining inc Oil Extraction | -6.8 | 0.4 | 1.4 | -9.9 | -8.0 | -5.2 | -0.3 |

| Electricity, Gas & Water Supply | -1.8 | 1.0 | 1.1 | -2.8 | 2.2 | 1.1 | -0.4 |

| Services | 0.6 | 0.6 | 0.6 | 2.2 | 3.7 | 2.7 | 2.7 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief