Global| Oct 21 2009

Global| Oct 21 2009UK Expected Output Turns The Corner As Total Orders Drop

Summary

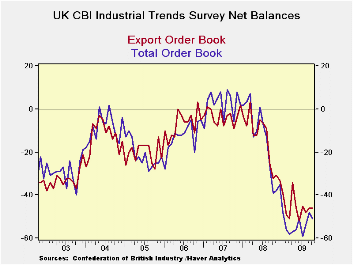

UK industrial orders according to the CBI up-minus-down net balance indicators fell in October. At a reading of -51 the orders index is above its cycle low of -59 but down from September’s -48. Export orders at a still weak -46 were [...]

UK industrial orders according to the CBI up-minus-down net

balance indicators fell in October. At a reading of -51 the orders

index is above its cycle low of -59 but down from September’s -48.

Export orders at a still weak -46 were flat at September’s level and

that strings the improvement out from the reading of -52 which was the

cycle low back in June. The volume outlook index crossed over from

negative to positive posting a +4 reading compared to the -2 it

registered in September. This switch ends a fifteen month string of

negative values for expected output.

The optimism on expected output is a good sign and one that has been long in coming. Still, the orders series remain very weak and lacks any real upward momentum. The orders series are holding their levels but these are still deeply negative readings that indicate orders are not stable but contracting. We have seen some recent readings on foreign orders elsewhere that have been spotty. In Germany, and more recently, Italy, their reports showed that ‘foreign’ orders have become irregular and progress has been set back at times. Of course, ‘foreign order’ has different meaning in different countries. While Germany rebounded from a one-month back track in its foreign orders reading, it is Italy’s newest reading that has gone negative. UK orders are weaker and its foreign orders are flat. There is more than one sign in the EU that the turn to growth may not be a smooth one. Still, UK firms are optimistic about future output trends. And that should count for something.

| UK Industrial volume data CBI Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Reported: | OCT-09 | SEP-09 | AUG-09 | JUL-09 | JUN-09 | 12MO Avg | Pcntle | Max | Min | Range |

| Total Orders | -51 | -48 | -54 | -59 | -51 | -50 | 12% | 9 | -59 | 68 |

| Export Orders | -46 | -46 | -48 | -45 | -52 | -42 | 11% | 3 | -52 | 55 |

| Stocks:FinGds | 10 | 13 | 13 | 20 | 22 | 24 | 36% | 31 | -2 | 33 |

| Looking ahead | ||||||||||

| Output Volume:Nxt 3M | 4 | -2 | -5 | -14 | -17 | -30 | 68% | 28 | -48 | 76 |

| Avg Prices 4Nxt 3m | -4 | -10 | -17 | -6 | -13 | -8 | 30% | 34 | -20 | 54 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief