Global| Aug 26 2014

Global| Aug 26 2014UK CBI Services Survey Weakens but May Not Point to a Slowdown

Summary

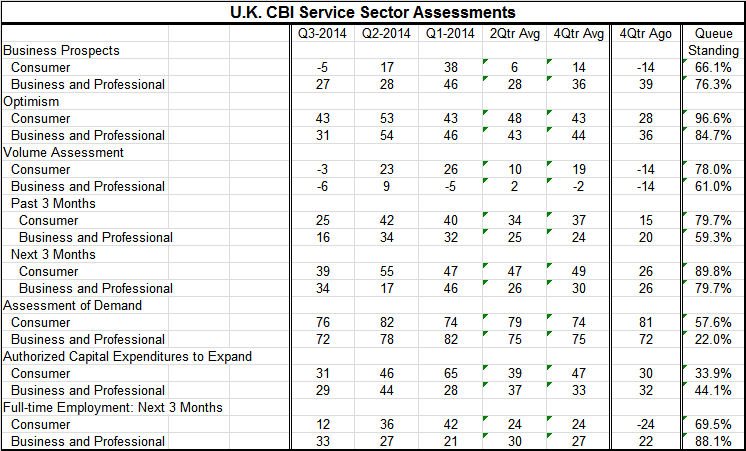

The U.K. services sector index for growth prospects turned lower in Q3, falling after nearly 2 years of improving trends. The CBI index is turned lower in the third quarter for both consumer and business and professional categories. [...]

The U.K. services sector index for growth prospects turned lower in Q3, falling after nearly 2 years of improving trends. The CBI index is turned lower in the third quarter for both consumer and business and professional categories. The nearly two-year string of improvements has not been monotonic, nor does the downturn this quarter necessarily point to the beginning of continuing erosion. However, the downturn in the consumer sector is relatively severe this quarter.

The U.K. services sector index for growth prospects turned lower in Q3, falling after nearly 2 years of improving trends. The CBI index is turned lower in the third quarter for both consumer and business and professional categories. The nearly two-year string of improvements has not been monotonic, nor does the downturn this quarter necessarily point to the beginning of continuing erosion. However, the downturn in the consumer sector is relatively severe this quarter.

As of the third quarter, the consumer sector standing for growth prospects is in its 66th percentile, whereas the standing for business and professional prospects stands in its 76th percentile. The nature of prospects in the business sector is slightly better than the consumer sector based on comparisons to each series history. We can also look at the raw scores for prospects where the consumer sector has turned to a reading of -5 in Q3, compared to a reading of 17 in Q2. This reading compared to average of 14 over four quarters. The business and professional raw score of 27 is only slightly lower than the Q2 reading of 28 and is below its fourth-quarter average of 36.

Optimism, however, is relatively stronger in the consumer sector. The consumer sector optimism reading stands in the 96th percentile of its historic queue, implying that it is better than this only 4% of the time. The business and professional standing is in about the 85th percentile of its historic queue, still a good reading for optimism, but slightly less than for the consumer sector. The raw reading for the consumer sector at 43 in Q3 is lower than its Q2 reading but it is back to its reading of the first quarter, which is also its fourth-quarter average. The reading for business and professional optimism is falling to a raw score of 31 in Q3 from 54 in Q2 and is below its fourth-quarter average of 44.

The raw volume assessment for the consumer sector has declined over the last two quarters to a reading of -3 in Q3 from 26 in Q1. This, however, is still a 78th percentile standing for that metric. The business and professional volume assessment is also negative at -6 in Q3 and it shows a slight deterioration from two quarters ago when its reading was -5. Its queue standing is in the 61st percentile.

The volume assessment over the past three months shows the consumer sector had stepped down in the quarter, its raw score of 25 compared to 42 in Q2 leaving it with its still strong, nearly 80th percentile standing. The past three month assessment for volume in the business and professional sector at 16 represented a drop from 34 in Q2 and a standing that's only in the 59th percentile of its historic queue. This tells us that over last three months, the business sector has been lagging behind the consumer sector.

Looking ahead to expectations for the next three months, the consumer sector has a reduced raw score of 39 compared to 55 in Q2. That's still an 89th percentile standing. The business and professional score has improved in Q3 from Q2 moving up to 34 from 17 where stands above its fourth-quarter average and it stands in the 79th percentile of its historic queue. Expectations for both sectors are relatively upbeat.

The assessment of demand in the consumer sector slipped slightly quarter to quarter but its raw 76 reading is above its fourth-quarter average of 74, but holds to a relatively moderate queue standing in the 57th percentile. The business and professional assessment of demand in Q3 is at a 72nd percentile, which is slightly below its fourth-quarter average of 75 and has a low 22nd percentile standing. The assessment of demand is a weak link in this survey and it contrasts with firm-to-strong volume assessments.

The authorization for capital expenditures for the purpose of expanding output shows a slippage to 31 in Q3 from 46 in Q2 for the consumer sector. It is below its four quarter-ago reading of 47 and has a low 33rd percentile standing. Business sector has capital expenditures slipping to 29 in Q3 from 44 in Q2 and standing slightly below their fourth-quarter average of 33. Their queue standing is in its 44th percentile, also a relatively weak reading.

Full-time employment for the next three months for the consumer sector has slipped to a net reading of 12 from 36 in the previous quarter and is only half its fourth-quarter average of 24. Still, its percentile standing is in the 70th percentile of its historic queue. For the business and professional sector, full-time employment demands are up to 33 from 27 a quarter ago and above their fourth-quarter average of 27. These metrics lead the current reading to a strong level in its 88th percentile.

While the readings for the services sector tend to show some slippage in the third quarter (only four of sixteen readings are above their respective four-quarter average), the readings for these metrics are still in the firm to strong region given an historic perspective (the average percentile standing is 67.9%). We find relative weakness in both sectors only for authorized capital expenditures for the purpose of expanding output and some moderation and weakness in the assessment of demand. It may be that it's just too early in the cycle and there is too much existing capacity for even the current rising level of demand to require capital expenditures. For the most part, the outlook for demand and full-time hiring is still relatively strong in the services sector. The quarter-to-quarter weakness in this report should not be construed as an indicator coming of weakness the services sector. There could be a seasonality issue, because out of 16 observations only 5 are lower from the same quarter of one year ago.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief