U.S. Q1 GDP Revised Weaker in Third Estimate

by:Sandy Batten

|in:Economy in Brief

Summary

- The previously reported 0.2% q/q saar decline was revised to -0.5%.

- Consumer spending weakened markedly to a tepid 0.5% from 1.2% previously.

- Net exports were still the major drag while inventory investment still made a key contribution.

- GDP and PCE inflation were each revised up slightly.

The 0.2% q/q saar decline in Q1 real GDP was revised significantly weaker to a 0.5% saar quarterly decline. The Action Economics Forecast Survey looked for no revision. The major factor behind the downward revision was much weaker personal consumption expenditures (PCE) than previously estimated. PCE advanced only 0.5% q/q, down from 1.2% in the previous estimate and 1.8% in the advance estimate. Within PCE, spending on services slowed markedly, increasingly just 0.6%, the slowest advance since Q2 2020 when spending collapsed after the COVID lockdown. The BEA noted that the revision to spending on services reflected new data from the Quarterly Services Survey. In the second estimate, spending on services had risen 1.7%.

The sharp widening of the trade deficit continued to be a major drag on GDP in Q1. Goods imports were revised down slightly from a 53.3% q/q saar surge in the second estimate to a still gigantic 51.6% quarterly increase. Export growth was revised markedly slower at 0.4% from 2.4% previously. The net effect was that net exports subtracted 4.6%-points after this revision, down from 4.9%-points previously. Some of the surge in imports landed in inventories, which rose $154 billion 2017$ and boosted GDP by 2.6%-points, essentially unchanged from the previous estimate.

The underlying health of the economy was not as good as previously estimated as domestic demand measures were revised down again. Final sales to domestic purchasers growth was revised down to 1.5% q/q saar from 2.0% in the second estimate, 2.3% in the advance report and 3.0% in last year’s Q4. Final sales to private domestic purchasers (a favorite measure of the Fed) slowed to 1.9% from 2.5% in the previous estimate, 3.0% in the advance report and 2.9% in Q4. After this revision, it is now clear that the economy has slowed markedly since the end of last year.

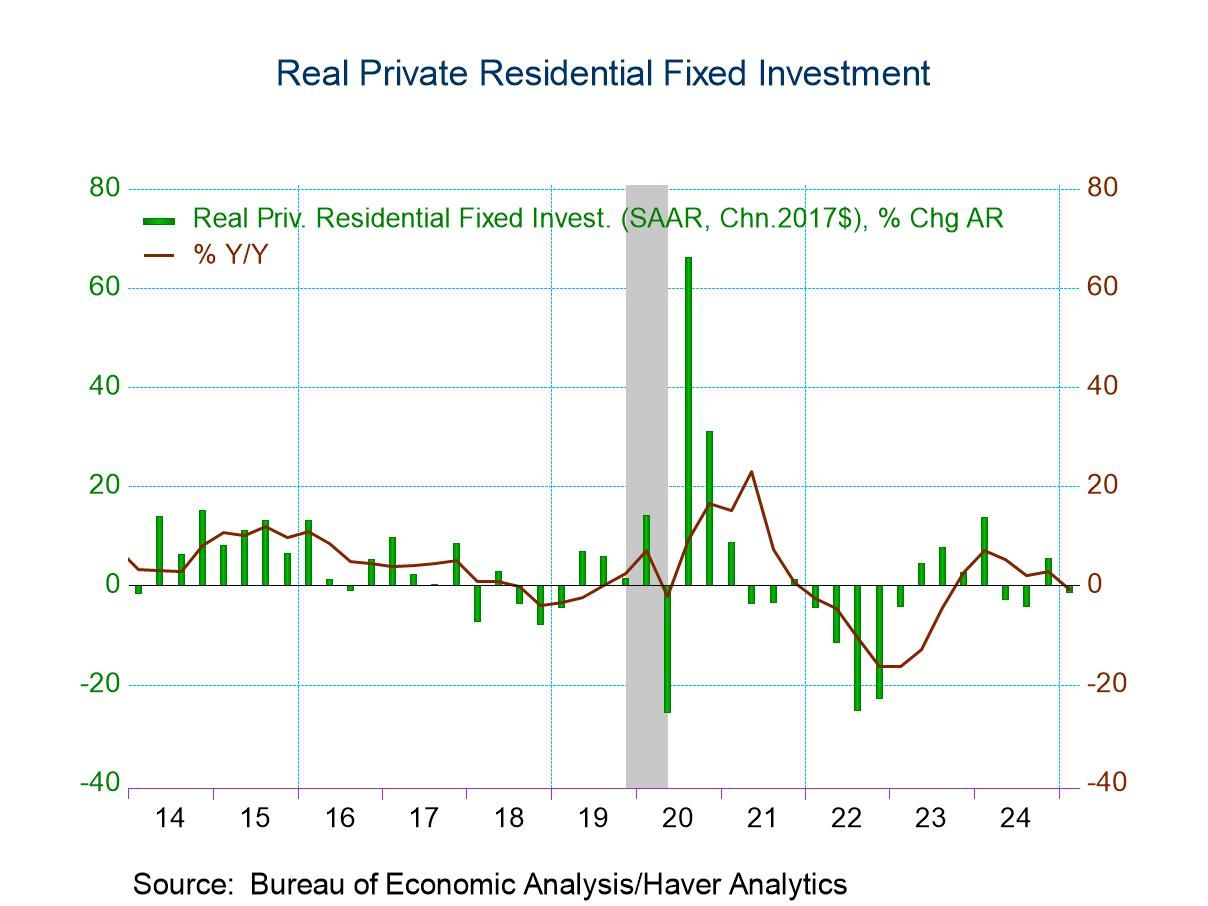

On a more positive note, nonresidential fixed investment continued to provide a meaningful boost to Q1 GDP. Growth of total nonresidential fixed investment was unrevised at 10.3% q/q saar, the largest quarterly advance since Q1 2022. This was led by a 23.7% quarterly surge in business spending on equipment, revised down slightly from 24.6% in the second estimate. This was still the fastest pace of equipment spending since the rebound from COVID lockdown in Q3 2020. By contrast, residential investment in Q1 was revised weaker in this estimate, falling 1.3% versus the previously estimated -0.6%.

Government spending was essentially unrevised, falling 0.6%q/q saar, led by an unrevised 7.1% decline in spending on national defense. Spending by state and local governments was revised slightly stronger with a 2.0% quarterly gain versus 1.7% in the previous estimate.

GDP price inflation was revised up a tick to 3.8% q/q saar from 3.7% previously and still a marked acceleration from 2.3% in Q4. PCE price inflation was also revised up a tick to 3.7%, well above the Fed’s 2% target, from 3.6% previously.

The previously reported 2.9% q/q not annualized decline in corporate profits was revised up to a 2.3% decrease. Domestic profits slipped 1.5% versus -2.5% previously while foreign profits slumped 7.3% versus -5.9% previously.

The GDP data can be found in Haver’s USECON and USNA databases. USNA contains virtually all the Bureau of Economic Analysis detail in the national accounts. The Action Economics consensus estimates can be found in AS1REPNA.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Asia

Asia