Global| Jun 25 2008

Global| Jun 25 2008UK CBI Sales/Order Survey Improves Slightly but Still Shows Decline

Summary

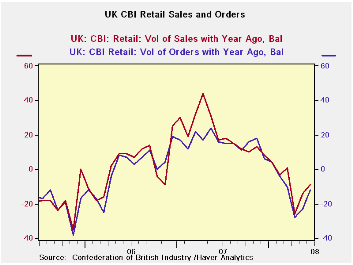

The CBI net balance diffusion presentation of its survey shows that sales in June were not as weak compared to a year ago as they were in May. But at -9 the result was still in the bottom quartile of the survey’s range of experience [...]

The CBI net balance diffusion presentation of its survey shows

that sales in June were not as weak compared to a year ago as they were

in May. But at -9 the result was still in the bottom quartile of the

survey’s range of experience and compares to an average response of +2.

Similarly orders at -12 were only ‘half as bad’ as the May result but

still registered in the lower 30% of their range. Some of this may have

been seasonal since sales for the ‘time of year’ scored a net reading

of -21 close to last month’s -25 reading, Inventories relative to sales

were elevated and stand in the 73rd percentile of their range.

The outlook for July is grim. At -7 the reading is loads worse

that the expectation of +6 that had been in place for June. Orders at

-13 are much weaker than June’s expectation for -2. Sales for the time

of year are expected to worsen to -17 compared to a -14 expectation for

June but an actual reading of -21 that emerged. Merchants appear to be

still downplaying the risk or maybe that is just normal bias, on their

part. The point is that the expectation for sales for the ‘time of

year’ is lower in July than it was in June so a worsening is expected

at least on that basis.

| UK Retail volume data CBI Survey | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Reported: | Jul-08 | Jun-08 | May-08 | Apr-08 | 12MO Avg | Pcntle | Max | Min | Range |

| Sales/Yr Ago | -- | -9 | -14 | -26 | 2 | 25% | 67 | -35 | 102 |

| Orders/Yr Ago | -- | -12 | -23 | -28 | 1 | 30% | 48 | -38 | 86 |

| Sales: Time/Yr | -- | -21 | -25 | -38 | -12 | 29% | 41 | -46 | 87 |

| Stocks:Sales | -- | 22 | 22 | 17 | 16 | 73% | 30 | 0 | 30 |

| Expected: | Jul-08 | ||||||||

| Sales/Yr Ago | -7 | 6 | -15 | -3 | 5 | 18% | 67 | -23 | 90 |

| Orders/Yr Ago | -13 | -2 | -14 | -6 | 2 | 26% | 47 | -34 | 81 |

| Sales: Time/Yr | -17 | -14 | -26 | -15 | -9 | 23% | 45 | -35 | 80 |

| Stocks:Sales | 13 | 16 | 18 | 11 | 12 | 43% | 26 | 3 | 23 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief