Global| Nov 16 2009

Global| Nov 16 2009U.S. Retail Sales Rise As Core Sales Improve Again

by:Tom Moeller

|in:Economy in Brief

Summary

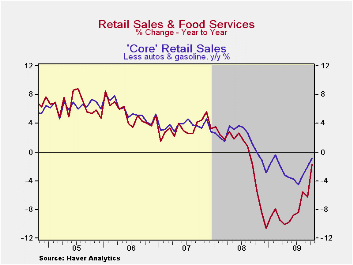

Consumers seem to be gaining back the inclination to spend. Retail sales last month rose 1.4% after a 2.3% September decline that was deeper than reported initially. A 0.9% October gain was the Consensus expectation. The increase [...]

Consumers

seem to be gaining back the inclination to spend. Retail sales last

month rose 1.4% after a 2.3% September decline that was deeper than

reported initially. A 0.9% October gain was the Consensus expectation.

The increase improved the y/y change in sales to -1.7% from declines of

roughly 10% earlier this year. Moreover, spending on "core" retail

sales has improved. Month-to-month changes in overall sales in recent

months have been quite volatile due to auto sales promotions and rising

gasoline prices. Aside from these distortions, gains in consumer

spending have been steady during the last three months and y/y growth

also improved. The retail sales data are available in Haver's USECON

database.

Consumers

seem to be gaining back the inclination to spend. Retail sales last

month rose 1.4% after a 2.3% September decline that was deeper than

reported initially. A 0.9% October gain was the Consensus expectation.

The increase improved the y/y change in sales to -1.7% from declines of

roughly 10% earlier this year. Moreover, spending on "core" retail

sales has improved. Month-to-month changes in overall sales in recent

months have been quite volatile due to auto sales promotions and rising

gasoline prices. Aside from these distortions, gains in consumer

spending have been steady during the last three months and y/y growth

also improved. The retail sales data are available in Haver's USECON

database.

Auto sales of late have been influenced by Detroit's sales

programs. Last month, retail sales of motor vehicles jumped 7.4% after

a 14.3% decline during September and a 10.2% August jump. Less autos,

sales rose 0.2% versus a 0.4% expected gain. Higher gasoline prices

also have influenced overall sales growth. Without autos &

gasoline, retail sales rose 0.3% last month, about as they did during

the prior two months. These gains raised the y/y change to

-0.8% from -4.4% as of July.

Auto sales of late have been influenced by Detroit's sales

programs. Last month, retail sales of motor vehicles jumped 7.4% after

a 14.3% decline during September and a 10.2% August jump. Less autos,

sales rose 0.2% versus a 0.4% expected gain. Higher gasoline prices

also have influenced overall sales growth. Without autos &

gasoline, retail sales rose 0.3% last month, about as they did during

the prior two months. These gains raised the y/y change to

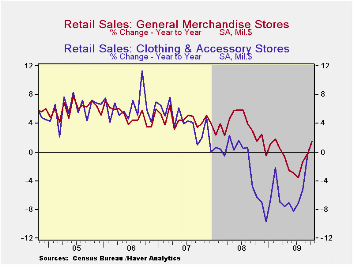

-0.8% from -4.4% as of July. In soft goods, the 0.4%

increase in apparel store sales was the fourth gain in as many months

and the y/y change of 1.5% was improved from -9.7% during December.

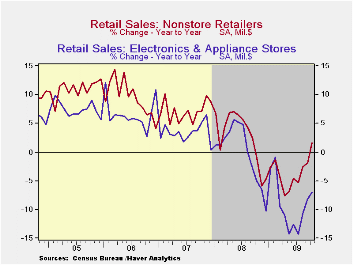

Finally, improvement in sales at furniture, electronics &

appliance store sales has been less impressive. Sales fell 0.7% last

month and the y/y change improved only to -7.3% from -14.3% at its

worst. Furniture store sales alone fell 0.8% (-7.6% y/y) after two

months of increase while sales of electronics & appliances

slipped 0.6% (-7.0% y/y), also after two months of increase.Internet

and catalogue purchases were firmer and rose 1.0% (1.6% y/y). The gain

contrasted with a 7.6% y/y decline as of April. Finally, restaurant

sales jumped 1.2% (1.5% y/y) after little change either m/m or y/y as

of September. Finally, building materials sales continued their slump

and fell 2.4% (-15.0% y/y).

In soft goods, the 0.4%

increase in apparel store sales was the fourth gain in as many months

and the y/y change of 1.5% was improved from -9.7% during December.

Finally, improvement in sales at furniture, electronics &

appliance store sales has been less impressive. Sales fell 0.7% last

month and the y/y change improved only to -7.3% from -14.3% at its

worst. Furniture store sales alone fell 0.8% (-7.6% y/y) after two

months of increase while sales of electronics & appliances

slipped 0.6% (-7.0% y/y), also after two months of increase.Internet

and catalogue purchases were firmer and rose 1.0% (1.6% y/y). The gain

contrasted with a 7.6% y/y decline as of April. Finally, restaurant

sales jumped 1.2% (1.5% y/y) after little change either m/m or y/y as

of September. Finally, building materials sales continued their slump

and fell 2.4% (-15.0% y/y).

| October | September | August | Y/Y | 2008 | 2007 | 2006 | |

|---|---|---|---|---|---|---|---|

| Retail Sales & Food Services (%) | 1.4 | -2.3 | 2.4 | -1.7 | -0.8 | 3.3 | 5.3 |

| Excluding Autos | 0.2 | 0.4 | 0.8 | -2.6 | 2.5 | 3.9 | 6.3 |

| Less Gasoline | 0.3 | 0.3 | 0.4 | -0.8 | 1.6 | 3.6 | 5.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief