Global| Nov 04 2004

Global| Nov 04 2004U.S. Productivity Growth Slowed From Strengthened 2Q Pace

by:Tom Moeller

|in:Economy in Brief

Summary

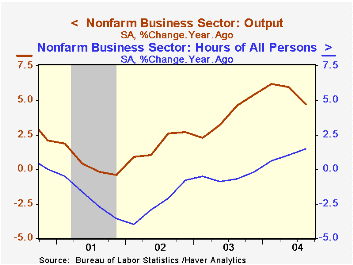

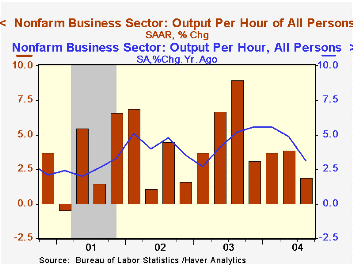

In 3Q04, non-farm labor productivity growth slowed to 1.9% but growth in 2Q was revised up to 3.9% from 2.5% estimated earlier. Consensus expectations had been for 2.0% growth in 3Q. The slowdown reflected improvement in the labor [...]

In 3Q04, non-farm labor productivity growth slowed to 1.9% but growth in 2Q was revised up to 3.9% from 2.5% estimated earlier. Consensus expectations had been for 2.0% growth in 3Q.

The slowdown reflected improvement in the labor market where growth in hours worked by all persons (employment times hours) accelerated to 2.1% (1.5% y/y) from 0.3% in 2Q. Output grew at a 4.1% rate (4.7% y/y), roughly the same as in 2Q.

Unit labor cost growth accelerated to 1.6% from 1.0% in 2Q due to the productivity slowdown even though compensation also slowed to 3.6% (3.7% y/y) from 4.9%.

Productivity in the manufacturing sector slipped sharply to 4.3% (4.6% y/y) from 8.3% in 2Q which was pegged earlier at 6.9%. Unit labor costs in the factory sector grew 0.1% (-2.1% y/y), the first quarterly increase this year.

| Non-farm Business Sector (SAAR) | 3Q '04 | 2Q '04 (Revised) | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Output per Hour | 1.9% | 3.9% | 3.1% | 4.4% | 4.4% | 2.5% |

| Compensation | 3.6% | 4.9% | 3.7% | 4.1% | 3.3% | 4.0% |

| Unit Labor Costs | 1.6% | 1.0% | 0.6% | -0.4% | -1.1% | 1.5% |

by Tom Moeller November 4, 2004

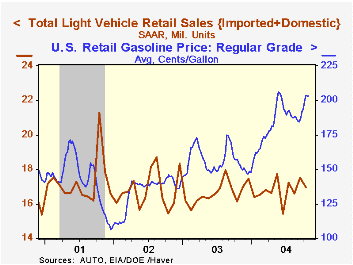

Unit sales of light vehicles dropped 3.1% m/m in October to a 16.96M selling rate. Consensus expectations had been for sales of 16.7M.

Sales of light trucks gave back all of September's gain with a 7.3% m/m drop as sweetened sales incentives were scaled back and also as gasoline prices breeched $2.00 per gallon. Domestic light truck sales dropped 9.2% m/m but imported light truck sales rose 6.9%.

Total auto sales rose 2.8% m/m for the second consecutive monthly gain on the strength of a 19.4% rise in imported auto sales. Sales of domestic autos fell 3.7%.

Imports' share of the US market for new vehicles ballooned to 22.1%, the highest since early 1991.

| Light Vehicle Sales (SAAR, Mil.Units) | Oct | Sept | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Total | 16.96 | 17.51 | 3.1% | 16.69 | 16.81 | 17.26 |

| Autos | 7.53 | 7.33 | -3.9% | 7.63 | 8.07 | 8.48 |

| Trucks | 9.43 | 10.18 | 8.9% | 9.06 | 8.74 | 8.78 |

by Tom Moeller November 4, 2004

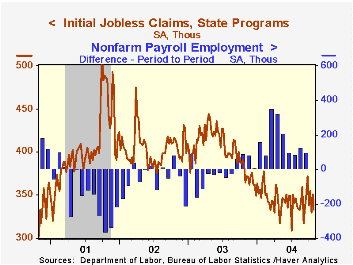

Last week, initial claims for unemployment insurance again reversed the prior period's change with a 19,000 decline to 332,000.The Consensus expectation had been for 340,000 claims.

Back and forth weekly gyrations of this order were the rule during October and the average level of initial claims for the month settled at 341,000, down slightly from 344,000 in September.

During the last ten years there has been a (negative) 73% correlation between the level of initial claims and the m/m change in payroll employment.

Continuing claims for unemployment insurance dropped 20,000 and reversed most of the prior week's gain.

The insured rate of unemployment remained at 2.2% for the fourth week.

| Unemployment Insurance (000s) | 10/30/04 | 10/23/04 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Initial Claims | 332 | 351 | -9.0% | 402 | 404 | 406 |

| Continuing Claims | -- | 2,800 | -19.1% | 3,531 | 3,570 | 3,018 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief