Global| Sep 04 2009

Global| Sep 04 2009U.S. Payroll Decline Eases But The Unemployment Rate Jumps To 26-Year High

by:Tom Moeller

|in:Economy in Brief

Summary

The August jobs figures from the Bureau of Labor Statistics gave conflicting signals. Suggesting some improvement in the labor market was payroll employment which declined the least of any month in a year, although the declines during [...]

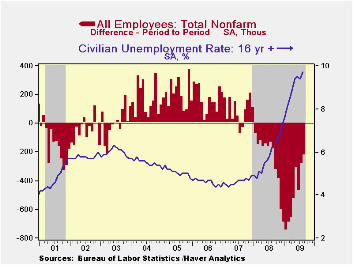

The August jobs figures from the Bureau of Labor Statistics gave conflicting signals. Suggesting some improvement in the labor market was payroll employment which declined the least of any month in a year, although the declines during the prior two months were revised deeper. Working the other way were the household survey figures. The unemployment rate, at 9.7%, jumped to its highest level since 1982. Together, the data hardly suggest that the recession is over, though downward momentum seems to have eased.

The length of the average workweek was stable m/m and q/q at 33.1. So far in the third quarter, aggregate hours worked (employment times hours) have fallen at a 2.6% annual rate after a 7.8% decline during 2Q.

Nonfarm payrolls fell 216,000 during August. That was less than the expected 228,000 decline however declines during the prior two months were revised deeper by a collective 49,000. The latest decline was the least since August of last year. Nevertheless, so far during this recession, employment has fallen by a total of 6.9 million, the record by far for a 20-month period. In percentage terms jobs are down 5.0% since the 2007 peak, also a record. Most recently, the payroll decline moderated to an average 318,000 over the last three months versus a peak three-month rate of 701,000 this past winter.

The jump in the unemployment rate to 9.7% from 9.4% compared with expectations for a smaller rise to 9.5%. The rate's cycle low of 4.4% occurred in October 2006. This level of the official unemployment rate pales, however, in comparison to the rate which includes "marginally attached workers" and those who are working part-time for economic reasons. It rose to 16.8%.

The increase in the overall jobless rate was due to a 392,000 (-3.9% y/y) fall in employment. That was easier than the worst monthly declines of this past winter but in-line with those of the last several months. It was accompanied by a modest 73,000 (-0.2% y/y) increase in the labor force after two months of sharp decline. The latest increase also saw a slight 38,000 decline in the number of "discouraged workers" after four months of increase. Also from the household survey, the median duration of unemployment slipped m/m to 15.4 weeks but that still was up from 8.3 weeks one year ago. The ranks of the long-term unemployed, however, rose slightly to 4.988 million.

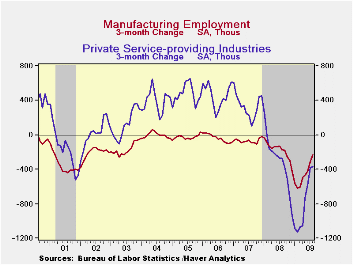

From the payroll survey, the moderation in the rate of job loss continued to stem from smaller declines in both factory sector and private service payrolls. Manufacturing sector jobs fell 63,000 last month after a 43,000 July decline. These shortfalls compare to an average 161,000 monthly decline during the prior nine months. Employment in the private service sector dropped 62,000 last month (-3.2% y/y) after a 126,000 July drop. Here again the declines are easier than 289,000 average during the prior nine months. Finally, job cuts in the construction sector also have moderated, but to a lesser extent. Employment here fell a reduced 65,000 last month after a 73,000 July decline and an average 100,000 during the nine months ended June.

In the government sector employment continued down as budgets shrank with lower tax revenues. Government jobs fell 18,000 (-0.3% y/y) after a downwardly-revised 28,000 July drop. Jobs with the federal government fell 5,000 (+1.9% y/y) for the third decline in the last four months. The number of state gov't jobs fell 5,000 (-1.1% y/y) and local gov't payrolls fell 8,000 (-0.5% y/y for the third consecutive down month. Should the federal government bail out the states? Lessons from past recessions from the Federal Reserve Bank of Chicago can be found here.

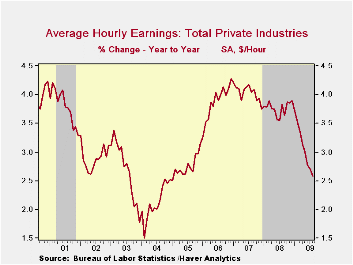

Average hourly earnings rose 0.3% during August for the second consecutive month. The 0.5% three-month growth rate is up off its low but compares to roughly 4% growth from 2006 to 2008. Earnings in the factory sector rose 0.2% and the three-month growth rate rose to 0.5%. Growth durable sector's earnings rose to 0.7%. Earnings in the private service sector recovered to 0.4% during the last three months.

The figures referenced above are available in Haver's USECON database. Additional detail can be found in the LABOR and in the EMPL databases.

| Employment: 000s | August | July | June | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Payroll Employment | -216 | -276 | -463 | -4.3% | -0.4% | 1.1% | 1.8% |

| Previous | -- | -247 | -443 | -- | -- | -- | -- |

| Manufacturing | -63 | -43 | -123 | -12.1% | -3.3% | -2.0% | -0.5% |

| Construction | -65 | -73 | -79 | -15.1% | -5.5% | -0.8% | 4.9% |

| Service Producing | -80 | -154 | -251 | -2.6% | 0.2% | 1.6% | 1.8% |

| Average Weekly Hours | 33.1 | 33.1 | 33.0 | 33.7 (Aug. '08) | 33.6 | 33.8 | 33.9 |

| Average Hourly Earnings | 0.3% | 0.3% | 0.1% | 2.6% | 3.8% | 4.0% | 3.9% |

| Unemployment Rate | 9.7% | 9.4% | 9.5% | 6.2% (Aug. '08) | 5.8% | 4.6% | 4.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief