Global| Jan 27 2010

Global| Jan 27 2010U.S. New Home Sales Drop Again& Remain 75% Below Peak

by:Tom Moeller

|in:Economy in Brief

Summary

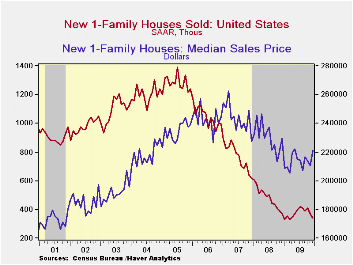

For new or existing home sales, December was a bleak month. Following Monday's report that existing home sales dropped sharply, the Commerce Department reported today that new home sales fell 7.6% m/m to 342,000 from an upwardly [...]

For

new or existing home sales, December was a bleak month. Following

Monday's report that existing home sales dropped sharply, the Commerce

Department reported today that new home sales fell 7.6% m/m to 342,000

from an upwardly revised November level. The latest was the fourth

decline in the last five months. December sales were the lowest since

last March and off 75.4% from the 2005 peak. Near term home sales

should be helped by the recent extension of the Federal government's

tax credit which now it is for all home buyers and not just first-time

purchases. The December sales figure fell well short of Consensus

expectations for 370,000 sales.

For

new or existing home sales, December was a bleak month. Following

Monday's report that existing home sales dropped sharply, the Commerce

Department reported today that new home sales fell 7.6% m/m to 342,000

from an upwardly revised November level. The latest was the fourth

decline in the last five months. December sales were the lowest since

last March and off 75.4% from the 2005 peak. Near term home sales

should be helped by the recent extension of the Federal government's

tax credit which now it is for all home buyers and not just first-time

purchases. The December sales figure fell well short of Consensus

expectations for 370,000 sales.

The December results capped a dismal year. For 2009 as a whole new home sales totaled 372,000 which was the lowest level since the numbers were first tallied in 1963.

Home prices firmed during December though the November figure was revised down. The median price of a new single-family home rose to $221,300 which was the highest level since May. The increase pared the y/y decline to 3.6% from its worst of -14.5% this past February. For all of 2009 median home prices fell 7.3% after a 5.5% decline during 2008.

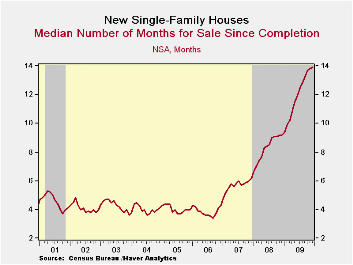

Price discounts and lower housing starts drove down the inventory of unsold homes by more than one-third y/y to its lowest since early-1971. The months' supply of unsold homes rose modestly to 8.1 months but remained down from the high of 12.4 months in January '09. Despite the shrinkage of inventory, it still took a record median 13.9 months to sell a new home.

Inflation: Mind the Gap from the Federal Reserve Bank of San Francisco is available here.

| US New Homes | December | November | October | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Total Sales (SAAR, 000s) | 342 | 370 | 408 | -8.6% | 372 | 481 | 769 |

| Northeast | 40 | 28 | 33 | 33.3 | 31 | 35 | 64 |

| Midwest | 43 | 73 | 56 | -27.1 | 54 | 69 | 118 |

| South | 178 | 192 | 224 | -7.8 | 201 | 264 | 409 |

| West | 81 | 77 | 95 | -12.0 | 87 | 113 | 178 |

| Median Price (NSA, $) | 221,300 | 210,300 | 213,700 | -3.6 | 213,567 | 230,408 | 243,742 |

by Robert Brusca January 27, 2010

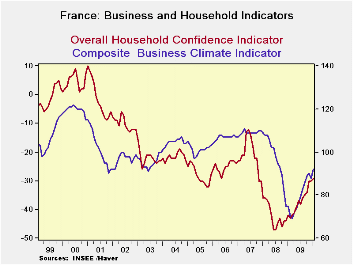

Despite great strides made in the improvement in business and household confidence since the pit of the recession, levels of confidence for business and households remain at levels that are below par. Both series, while still climbing, are showing signs of slowing the pace of that advance.

The industry climate reading stands in the 43rd percentile of its range well below the mid point and at an index of 92 it stands well below the mean value of 100 as well. The only reading that stands above its mean is the RECENT trend for production. Unfortunately the likely trend is at the 47th percentile of its range, below the midpoint and at a reading of -7 it is below its mean reading of +5. The orders trends are improving but they have a very long way to go just to get back to neutral.

The story for the household sector is much the same as for business, except weaker. At -29 the confidence reading for households is below neutral and in fact is much weaker than that standing short of the one-third mark of its range. The mean reading stands at -19 but confidence reads -29 in January.

While the strongest reading from the consumer is a positive reading on the household’s current financial standing (a reading in the 81st percentile of its range) the next highest reading is a 77th percentile reading on the prospect for unemployment. These two readings are diametrically opposed. French consumers fear unemployment yet see that they are in a relatively strong current financial situation, even as the economy is putting its worst days behind it. This is surely a prescription for the consumer to keep his wallet locked up tightly.

Responses show that living standards are thought to have improved and to be improving. Yet these readings are low in their respective ranges and well short of historic median values.

Savings is one of the bright spots. While standing in the 59th and 65th percentiles both the responses for ‘favorable to save’ and ‘ability to save’ are near or above historic median values.

Spending, a key parameter for getting recovery in gear is still rated as subpar. Households’ response to the question ‘is it a favorable time to spend?’ resides just short of the 40th range percentile and at a raw reading of -19 that is short of its median value of -14.

In short the business sector and the consumer sector see ongoing progress

| INSEE Industry Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1990 | Since Jan 1990 | |||||||||

| Jan 10 |

Dec 09 |

Nov 09 |

Oct 09 |

Percentile | Rank | Max | Min | Range | Mean | |

| Climate | 92 | 88 | 90 | 89 | 43.4 | 186 | 122 | 69 | 53 | 100 |

| Production | ||||||||||

| Recent Trend | -4 | -10 | -8 | -8 | 59.3 | 111 | 44 | -74 | 118 | -8 |

| Likely trend | -7 | -5 | -1 | -1 | 47.1 | 211 | 30 | -40 | 70 | 5 |

| Orders/Demand | ||||||||||

| Orders&Demand | -45 | -52 | -52 | -52 | 22.2 | 215 | 25 | -65 | 90 | -17 |

| Fgn Orders&Demand | -45 | -54 | -46 | -49 | 25.5 | 215 | 31 | -71 | 102 | -13 |

| Prices | ||||||||||

| Likely Sales Price Trend | -11 | -18 | -13 | -9 | 25.5 | 205 | 24 | -23 | 47 | 0 |

The consumer is still not solidly underpinned by the notion that government has stabilized the economic environment. Even though consumers are feeling relatively financially settled they are fearful of the future and therefore are not very prone to spend. Spending proclivity is lagging behind improvements in financial well being. This is an issue for policymakers. It is not necessarily a call out for any new program but for leadership to take steps to reassure an economically frightened public that is better off than it suspects and whose fear could become a catalyst for backsliding.

As for business its progress is steady and there is no concern about inflation. But even as current conditions have improved, here again we see reluctance to extrapolate ongoing improvement into the future. The orders data manifest this result with still weak (although improving) readings for orders and demand that seem to get a greater weight than their improving trend. What is lacking in France is confidence and more certainty about the future.

That predicament may also be a statement about the e-Zone in which France is firmly embedded. The whole of the e-zone is still struggling with several states still battling horrific issues. In this environment the euro, the strap that binds Europe together may be more of a corset that restrains optimism since the healthy countries are more afraid of being pulled down by or made to assist those that are struggling. Europe seems to have been able to cobble together an economic structure that has doe it more harm than good. The area is bound together by a common currency that protects the imprudent from the consequences of their own actions. Fiscal transgression is not easily exported since fiscal accounts are kept separate. There is no sharing of the public expenditure pot in Europe except for certain consolidated government funding. Still there is a stigma. And you may recall how the Latin American Debt crisis brought down all of Latin America despite there being no common currency and no shared fiscal responsibility of any type – just proximity and shared culture. Europe is walking a very shaking tightrope and has not figured out yet how to remedy its problems. France is but an example.

| INSEE Household Monthly Survey | |||||||

|---|---|---|---|---|---|---|---|

| Since Jan 1990 | |||||||

| Jan 10 |

Dec 09 |

Nov 09 |

Oct 09 |

Percentile | Rank % | Mean | |

| Household Confidence | -29 | -30 | -30 | -34 | 31.6 | 21.6 | -19 |

| Living Standards | |||||||

| past 12 Mos | -62 | -65 | -65 | -70 | 18.4 | 16.2 | -40 |

| Next 12-Mos | -34 | -36 | -35 | -39 | 33.3 | 24.9 | -21 |

| Unemployment: Next 12 | 64 | 62 | 63 | 65 | 77.7 | 88.4 | 33 |

| Price Developments | |||||||

| Past 12Mo | -22 | -25 | -27 | -28 | 28.9 | 55.2 | -16 |

| Next 12-Mos | -37 | -42 | -46 | -45 | 24.7 | 53.1 | -35 |

| Savings | |||||||

| Favorable to save | 21 | 12 | 13 | 8 | 59.1 | 46.1 | 22 |

| Ability to save Next 12 | -4 | -6 | -7 | -11 | 65.5 | 83.8 | -9 |

| Spending | |||||||

| Favorable for major purchase | -19 | -20 | -19 | -24 | 39.7 | 40.2 | -14 |

| Financial Situation | |||||||

| Current | 20 | 18 | 17 | 13 | 81.0 | 97.5 | 12 |

| Past 12 MOs | -21 | -21 | -22 | -25 | 48.4 | 29.0 | -17 |

| Next 12-Mos | -10 | -10 | -8 | -12 | 40.0 | 15.8 | -2 |

| Number of observations in the period = 241 | |||||||

by Tom Moeller January 27, 2010

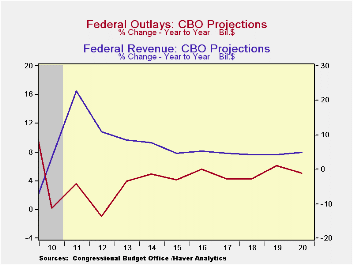

The

latest estimates of the federal government's budget deficit were

released yesterday by the Congressional Budget Office. Though this

fiscal year's deficit estimate of $1.3 trillion was down slightly from

2009 due to the end of the latest recession, it remained near a record.

As a percentage of GDP, the 9.2% deficit was near its peak and triple

the 2008 figure.

The

latest estimates of the federal government's budget deficit were

released yesterday by the Congressional Budget Office. Though this

fiscal year's deficit estimate of $1.3 trillion was down slightly from

2009 due to the end of the latest recession, it remained near a record.

As a percentage of GDP, the 9.2% deficit was near its peak and triple

the 2008 figure.

With the end of the recession revenues are expected to rise 3.3% after the huge decline last year. Thereafter, as the economic recovery matures revenue growth is expected in the double-digits for both 2011 and 2012. Subpar growth in employment is expected, however, to hold revenue growth below recoveries. A subpar recovery in corporate profits also would contribute to low federal revenue growth.

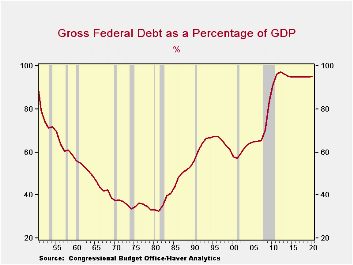

This year the projected deficit would lift the national debt to $13.3 trillion. At 91% of GDP that is the highest level since 1950.

The CBO's latest budget projections are available in Haver's USECON database.

Budget Outlook 2010 from the Congressional Budget Office can be found here.

| Ongressional Budget Office Projections | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|

| Federal Budget Deficit ($ Billion) | 1,414 | 1,349 | 980 | 650 | 539 |

| % of GDP | 10.0 | 9.2 | 6.5 | 4.1 | 3.2 |

| Revenues | -16.6 | 3.3 | 22.8 | 11.0 | 8.6 |

| Outlays | 17.9 | 0.2 | 3.6 | -1.0 | 4.0 |

| Underlying Assumptions | |||||

| Nominal GDP | -1.4 | 2.5 | 2.7 | 4.9 | 6.0 |

| Real GDP | -2.9 | 1.6 | 1.8 | 3.9 | 4.9 |

| Consumer Price Index | -0.3 | 2.4 | 1.4 | 1.2 | 1.1 |

| Unemployment Rate | 9.3 | 10.1 | 9.5 | 8.0 | 6.3 |

| 10-Year Treasury Note Rate | 3.2 | 3.6 | 3.9 | 4.2 | 4.5 |

by Tom Moeller January 27, 2010

The FOMC statement regarding the economy was upgraded slightly. "Information received since the Federal Open Market Committee met in December suggests that economic activity has continued to strengthen and that the deterioration in the labor market is abating."

Regarding inflation the statement was succinct. "With substantial resource slack continuing to restrain cost pressures and with longer-term inflation expectations stable, inflation is likely to be subdued for some time."

Finally, the Fed left little-changed its prior comments on the improved functioning of financial markets. Moreover, one board member indicated "that economic and financial conditions had changed sufficiently that the expectation of exceptionally low levels of the federal funds rate for an extended period was no longer warranted."

A complete text of the Fed's latest press release can be found here .

The Haver databases USECON, WEEKLY and DAILY contain the figures from the Federal Reserve Board.

| Current | Last | 2009 | 2008 | 2007 | |

|---|---|---|---|---|---|

| Federal Funds Rate, % (Target) | 0.00 - 0.25 | 0.00 - 0.25 | 0.16 | 1.93 | 5.02 |

| Discount Rate, % | 0.50 | 0.50 | 0.50 | 2.39 | 5.86 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief