Global| Aug 21 2014

Global| Aug 21 2014U.S. LEI Begins to Accelerate

Summary

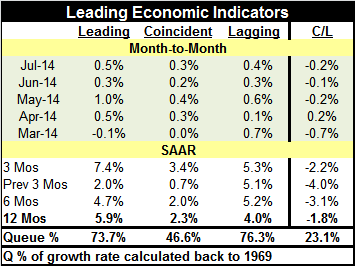

The index of leading economic indicators is beginning to accelerate. The three-month growth rate is 7.4% at an annual rate. Over the previous three months, it grew at a 2.0% annual rate. Over 12 months, it is growing at a 5.9% annual [...]

The index of leading economic indicators is beginning to accelerate. The three-month growth rate is 7.4% at an annual rate. Over the previous three months, it grew at a 2.0% annual rate. Over 12 months, it is growing at a 5.9% annual rate. At the same time, the coincident index is doing better; it's growing at a 3.4% annual rate over three months. That's up from 2% over six months and 2.3% over 12 months.

The index of leading economic indicators is beginning to accelerate. The three-month growth rate is 7.4% at an annual rate. Over the previous three months, it grew at a 2.0% annual rate. Over 12 months, it is growing at a 5.9% annual rate. At the same time, the coincident index is doing better; it's growing at a 3.4% annual rate over three months. That's up from 2% over six months and 2.3% over 12 months.

In July, the leading index rose by 0.5% after a 0.3% gain in June. The coincident index rose by 0.3% following June's 0.2% increase. There are steady increases in the LEI and the coincident index over the last four months.

How strong are these growth rates? The year-over-year growth rate for the LEI has been higher only about 26% of the time. The coincident index growth rate has been higher about 54% of the time. Neither one of these growth rates is exceptionally strong. The coincident economic index is still very pedestrian even though it has accelerated. The leading economic index is more in the category of being solid-to-strong; it's only higher about quarter of the time.

The question these metrics rates raise is this: is the economy strong enough to withstand interest-rate increases from the Federal Reserve? In the Fed's July meeting, we saw the most striking divide that we have seen in this recovery at a Fed meeting. There is now a group at the Fed that believes the time is right to begin raising rates. It's no longer a question of theory or the future. It's a question of here now. Just today Esther George, President of the Kansas City Fed who is hosting the annual Jackson Hole conference in Wyoming, said she thinks the economy is strong enough to stand up to a rate hike.

Charles Plosser of the Philadelphia Fed on record is critical about forward guidance that seems to stick out like a sore thumb of vague promises rather than to tie itself the economic data.

Jim Bullard of the St. Louis Fed has been producing graphics showing how the Fed is closing in on its objectives for inflation and unemployment, while its policy tools namely, the fed funds rate and the size the Fed's balance sheet, continue to push out at the extremes of their usage.

Both of these points got play on the recent FOMC minutes from the July meeting where some members called for forward guidance to link itself more clearly to data objectives. And of course there is the question of whether it's the right time to start raising rates. At that meeting, the Fed did not change policy statement, but members agreed that the Fed was closing in on its objectives faster than expected. But it began to entertain the idea that it might be right to start changing its policies faster than it had expected. Still, the actual language in the minutes said that that would depend upon the trajectory of economic growth, the unemployment rate and inflation, a three legged stool.

The LEI points to an economy that is gathering momentum. The coincident index is one measure that is getting brighter but is still moderate. While by historic standards the growth rates of these two components are not strong, both are showing strings of monthly increases. The leading index itself is flirting with strength. And LEI strength makes the coincident index look better.

As always trying to figure out what the Fed is going to do and when it's going to do it, is like trying to guess how many angels can stand on the head of a pin. The Fed clearly has pressures and tensions among its members about what the right policy should be. The leading economic index and its coincident component speak to growth and to expected growth. On that score, the economy seems to be doing adequately. However, the Fed is still lagging in terms of hitting its inflation variable. The Fed's objectives now are essentially a three legged stool. We can count the LEI is a positive factor in the outlook, and current growth as solid, but it's not strong enough to convince us about what the Fed will do because the question of inflation is still unresolved.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief