Global| Apr 02 2010

Global| Apr 02 2010U.S. Job Market Firms; JoblessRate Is Steady And Payrolls Rise

by:Tom Moeller

|in:Economy in Brief

Summary

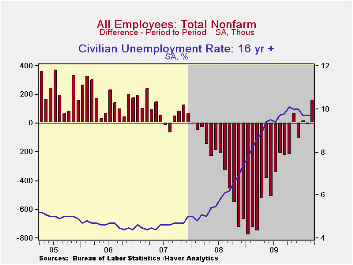

The Bureau of Labor Statistics reported that, all-in-all, labor market conditions firmed somewhat more-than-expected last month. From the household survey, the unemployment rate held steady for the third month at an expected 9.7%, [...]

The Bureau of Labor Statistics reported that, all-in-all, labor market conditions firmed somewhat more-than-expected last month. From the household survey, the unemployment rate held steady for the third month at an expected 9.7%, down from the October high of 10.1%. That stability owed to improved hiring. Employment rose 264,000 (-1.4% y/y) for the third consecutive monthly gain. These increases follow monthly declines of as much as 967,000 during the recession. In addition, improved hiring is prompting an expansion of the labor force. The 398,000 gain (-0.2% y/y) was the largest of three consecutive monthly increases. Throughout 2009 the labor force contracted slightly. The gain reflects a rise in the labor force participation rate to 64.9%, its third month of increase following steady declines last year.

The establishment survey also painted a picture of an improved job market. To start, payrolls expanded 162,000. Though the gain was slightly less-than-expected, the increase followed a lessened decline of 14,000 in February. Also, a slight decline in January payrolls was revised to a small increase. The real surprise, however, was that Census workers contributed just 48,000 to last month's payroll gain and that raised government hiring by 39,000 (-0.3% y/y). Therefore, private-sector jobs expanded 123,000 (-2.1% y/y), the biggest of four gains in the last five months.

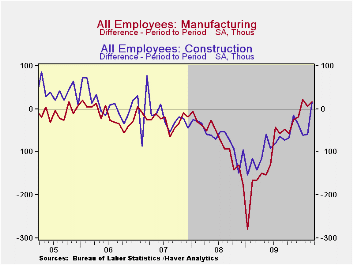

The payroll gain reflected an 82,000 increase in private-services. It was the fourth increase in the last five months after severe weather dampened February hiring. Temporary jobs rose 40,200 (8.9% y/y) for the sixth consecutive monthly increase. Construction jobs benefitted from the weather as well with a 15,000 increase, though it was the first gain since early-2007. Factory sector employment also firmed and the 17,000 rise was the third consecutive monthly increase.

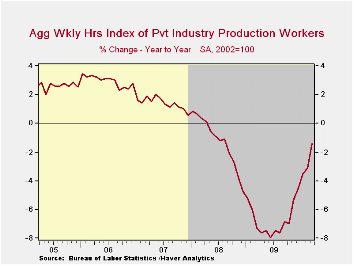

The total workweek bounced back after the storm and earlier numbers were upwardly-revised. The gain to 34.0 hours pulled the workweek to its longest in twelve months. Combined with the gain in employment, aggregate hours worked rose 0.7% and by 0.4% last quarter.

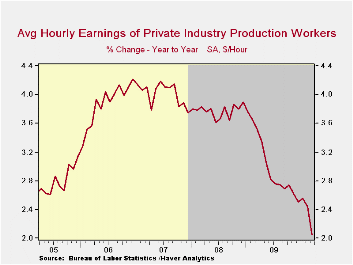

Average hourly earnings fell 0.1% and reversed the February increase. It was the first monthly decline since 2003 and lowered the y/y gain to 2.1%, its weakest since early-2004.

| Employment: 000s | March | February | January | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Payroll Employment | 162 | -14 | 14 | -1.8% | -4.3% | -0.6% | 1.1% |

| Previous | -- | -36 | -26 | -- | -- | -- | -- |

| Manufacturing | 17 | 6 | 22 | -5.2% | -11.3% | -3.4% | -2.0% |

| Construction | 15 | -59 | -60 | -11.1% | -15.7% | -6.1% | -0.8% |

| Private Service Producing | 82 | 55 | 46 | -1.0% | -3.4% | -0.2% | 1.7% |

| Government | 39 | -22 | -2 | -0.3% | 0.2% | 1.3% | 1.1% |

| Average Weekly Hours | 34.0 | 33.9 | 34.0 | 34.0(March '09) | 33.1 | 33.6 | 33.8 |

| Average Hourly Earnings | -0.1% | 0.1% | 0.3% | 2.1% | 3.0% | 3.8% | 4.0% |

| Unemployment Rate | 9.7% | 9.7% | 9.7% | 8.6%(March '09) | 9.3% | 5.8% | 4.6% |

by Robert Brusca April 2, 2010

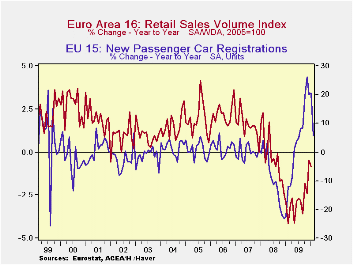

Policymakers around the world have used the auto sector as a lever to try and pry growth out of their respective economies. It may seem strange that such a ‘big ticket item’ would be uses so universally, but that is partly the result of the type of crisis governments and central banks have been fighting. Few buy cars without bank financing. And bank financing had retracted sharply in the crisis.

Auto incentives ladened with tax breaks helped to get the sector moving ahead. Now the incentives have been removed and sales are falling back to economically supportable levels. In the e-Zone we can see that while car sales are falling back retail sales have been steadily cutting their losses. It’s not great but its progress.

France and Italy are the early auto sales (actually registrations are recorded in Europe) reporters. They each show that sales have advanced in March more than compensating for the sales drop in February. Although the drop off in overall auto sales seems severe, it is only sales getting back to normal after some very successful incentives. The reduction in the rate of decline in retail sales underscores that there is some progress on the part of the Euro-consumer. France and Italy are showing that m/m sales can still rise in this environment in which has the growth rate of Yr/Yr sales dropping so sharply.

| Euro-Area Car Registrations | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Mo/Mo % | 3-Mo Trend From | 6-Mo Trend From | 12-Mo Trend From | ||||||

| All Seas Adj | Mar-10 | Feb-10 | Jan-10 | Mar-10 | Feb-10 | Mar-10 | Feb-10 | Mar-10 | Feb-10 |

| France(&WDA) | 1.0% | -0.2% | -17.0% | -50.8% | -46.2% | 6.2% | 23.6% | 12.7% | 18.8% |

| Italy | 5.1% | -2.9% | -2.5% | -2.0% | -19.2% | 11.6% | 7.1% | 12.2% | 21.6% |

| base Month of Calc | Feb-10 | Jan-10 | Dec-09 | Dec-09 | Nov-09 | Sep-09 | Aug-09 | Mar-09 | Feb-09 |

by Tom Moeller April 2, 2010

Making up

sales which earlier had suffered from "special" factors, U.S.

unit sales of light vehicles during March jumped to

11.78M units (SAAR) from 10.38M in February. The latest was the highest

level since last August when aggressive sales promotions lifted sales.

March sales fell slightly short of Consensus expectations for 12.0M.

(Seasonal adjustment of these figures is provided by the U.S. Bureau of

Economic Analysis).

Making up

sales which earlier had suffered from "special" factors, U.S.

unit sales of light vehicles during March jumped to

11.78M units (SAAR) from 10.38M in February. The latest was the highest

level since last August when aggressive sales promotions lifted sales.

March sales fell slightly short of Consensus expectations for 12.0M.

(Seasonal adjustment of these figures is provided by the U.S. Bureau of

Economic Analysis).

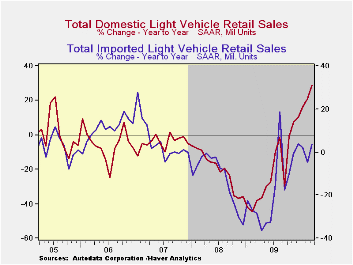

Sales of domestically produced

vehicles

jumped 14.0% last month to 8.79M units (28.5% y/y)

from 7.71M in February. Sales of fuel efficient cars rose 11.8% for the

month (28.8% y/y) while light truck sales also posted a solid 16.0% m/m

gain (28.3% y/y). Imported light vehicle sales

recovered 12.0% (3.7% y/y) after a sharp February decline, due in part

to the recall of some Toyota models. With a 5.9% gain, sales of

imported autos recovered all of the February loss while light truck

sales were stronger with a m/m gain of 24.9%, though just 1.7% y/y.

vehicles

jumped 14.0% last month to 8.79M units (28.5% y/y)

from 7.71M in February. Sales of fuel efficient cars rose 11.8% for the

month (28.8% y/y) while light truck sales also posted a solid 16.0% m/m

gain (28.3% y/y). Imported light vehicle sales

recovered 12.0% (3.7% y/y) after a sharp February decline, due in part

to the recall of some Toyota models. With a 5.9% gain, sales of

imported autos recovered all of the February loss while light truck

sales were stronger with a m/m gain of 24.9%, though just 1.7% y/y.

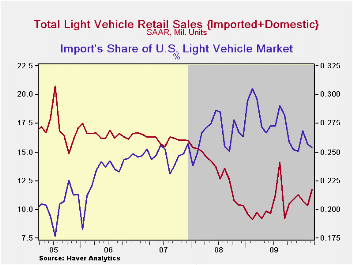

Overall, import's share of the U.S. light vehicle market during February fell to 25.4%. The share has been declining erratically from its high of 30.5% in February '09 and from 27.6% during all of last year. (Imported vehicles are those produced outside the United States.) Imports' share of the U.S. car market fell m/m to 31.8% and that was below 34.8% during 2009. Imports' share of the light truck market improved to 18.7% but remained below the 19.6% last year.

The U.S. vehicle sales figures can be found in Haver's USECON database.

| Light Vehicle Sales (SAAR, Mil. Units) | March | February | January | March Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Total | 11.78 | 10.38 | 10.78 | 21.2% | 10.37 | 13.22 | 16.16 |

| Autos | 6.04 | 5.49 | 5.70 | 20.1 | 5.46 | 6.76 | 7.58 |

| Domestic | 4.12 | 3.68 | 3.78 | 28.8 | 3.56 | 4.44 | 5.06 |

| Imported | 1.92 | 1.81 | 1.92 | 4.8 | 1.90 | 2.32 | 2.52 |

| Light Trucks | 5.74 | 4.88 | 5.08 | 22.4 | 4.91 | 6.46 | 8.60 |

| Domestic | 4.67 | 4.03 | 4.11 | 28.3 | 3.95 | 5.28 | 7.10 |

| Imported | 1.07 | 0.86 | 0.97 | 1.7 | 0.96 | 1.18 | 1.47 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief