Global| Jan 05 2018

Global| Jan 05 2018U.S. ISM Nonmanufacturing Cools

Summary

The monthly snap-shot The ISM nonmanufacturing index receded to 55.9 in December from 57.4 in November. It is at its weakest level since August. Activity cooled in the overall index in terms of activity, new orders, order backlogs, [...]

The monthly snap-shot

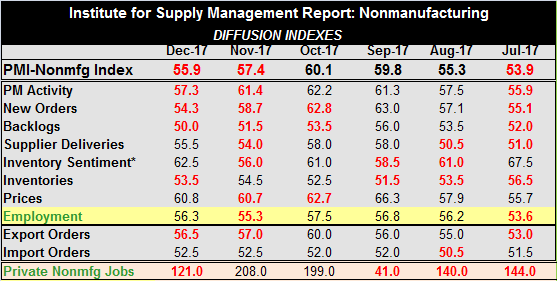

The ISM nonmanufacturing index receded to 55.9 in December from 57.4 in November. It is at its weakest level since August.

The monthly snap-shot

The ISM nonmanufacturing index receded to 55.9 in December from 57.4 in November. It is at its weakest level since August.

Activity cooled in the overall index in terms of activity, new orders, order backlogs, inventories and exports.

Contrarily, there were increases in supplier delivery lags, inventory sentiment, employment and a small uptick in prices. The import order series was flat on the month.

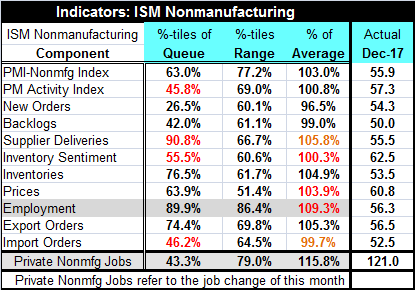

What these metrics mean: The table below presents several different ways to evaluate the strength in the PMI and its various components. Of course, the raw numbers are evaluated relative to a value of '50' which marks the difference between expansion and contraction. But apart from that, each series has its own mean and tendency to vary. I will use the first column in the table below on the percentile queue standings to put each reading some proper historic perspective. It tells where the latest month's observation ranks in an ordered queue of historic results.

First, the overall ISM nonmanufacturing index is moderately firm with a 63rd percentile standing. That standing means that the index is this high or higher about 37% of the time. At its current level, the ISM nonmanufacturing index resides just outside of the top one third of its historic range of values, a firm but not strong standing.

Activity, despite its high-sounding diffusion value of 57.3, has a 45.8 percentile queue standing which leaves it below its historic mean. Activity in the nonmanufacturing sector was not up to par in December.

New orders at 54.3 showed expansion. But orders were downright weak, being weaker only about 26.5% of the time historically. Despite what you heard about strong consumer spending and a robust December for retailers, the nonmanufacturing sector overall was weak in December when it comes to new order volume.

Order backlogs also were weak with a 42nd percentile standing. They also are below their historic median (which occurs at '50' for all these categories by construction).

Supplier delivery speeds, however, show heat. At a diffusion value of 55.5, they have been stronger than that less than 10% of the time historically.

Inventory sentiment has a very moderate 55.5 percentile standing in December while inventory levels have a 76.5 percentile standing.

Prices are moderate with a 63.9 percentile standing. Their 60.8 diffusion level looks high, but it is not high in historic context.

The employment reading is still strong in December with an 89.9 percentile standing. That metric has been higher only about 10% of the time. It contrasts with the data on actual nonfarm jobs in the month which has a percentile standing of 36.2 over the same period. So firms are reporting higher staffing levels that aggregate job creating affirms for the month. That is an interesting disconnect

Export orders are relatively strong with a 74.4 percentile standing, nearly a top 25th percentile standing. Imports orders contrarily are below their median with a 46.2 percentile standing.

Summing up On balance, we see the ebb and flow of business in these numbers. I suspect that the ranking of the details in the various categories are somewhat surprising to many. The nonmanufacturing ISM headline looks strong at 55.9, but in fact this index cannot be compared in absolute value to the manufacturing index. The series' surveyed components are simply losing some steam. Prices had spiked earlier but are now coming off their boil. Orders too had surged but are now settling back. The weakness in orders may be the most surprising element in December's report.

Of course, it is an odd time of year. It was the end of the year. We are in the wake of a period in which various activities had been interrupted by hurricanes then enhanced by the rebuilding and asset restocking. There is forest fire destruction and there will be rebuilding out West. And to complete matters, 2018 is starting out with an Arctic freeze that may make January not very representative of the economy's health. It is always something. But the ISM momentum that had welled up in October and November has now past and we are on the downslope.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief