Global| Sep 01 2017

Global| Sep 01 2017U.S. ISM Manufacturing Jumps in August

Summary

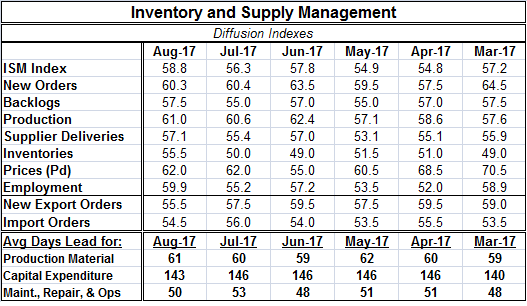

The ISM manufacturing index moved up sharply to 58.8 in August from 56.3 in July. The regional Fed manufacturing surveys have been very strong and are fully consistent with this result. This month was unusual as the U.S. employment [...]

The ISM manufacturing index moved up sharply to 58.8 in August from 56.3 in July. The regional Fed manufacturing surveys have been very strong and are fully consistent with this result. This month was unusual as the U.S. employment report preceded the manufacturing ISM. In it, manufacturing employment was very strong plus the BLS labor diffusion index in manufacturing was at a cycle high. The ISM employment component is similarly strong in August. So we have agreement on this between the ISM and the BLS. But the manufacturing survey from Markit on U.S. manufacturing is like a gauge for different economy. It was lower in August and ranked over the last five and one-half years its August standing is only in about the 37th percentile of its queue of data - relatively weak. In short, it has been misleading while the ISM and regional Fed reports have been pointing in the right direction.

The ISM manufacturing index moved up sharply to 58.8 in August from 56.3 in July. The regional Fed manufacturing surveys have been very strong and are fully consistent with this result. This month was unusual as the U.S. employment report preceded the manufacturing ISM. In it, manufacturing employment was very strong plus the BLS labor diffusion index in manufacturing was at a cycle high. The ISM employment component is similarly strong in August. So we have agreement on this between the ISM and the BLS. But the manufacturing survey from Markit on U.S. manufacturing is like a gauge for different economy. It was lower in August and ranked over the last five and one-half years its August standing is only in about the 37th percentile of its queue of data - relatively weak. In short, it has been misleading while the ISM and regional Fed reports have been pointing in the right direction.

New orders, export orders and import orders were the only components to fall month-to month. But prices paid were unchanged month-to-month and remain tepid.

One developing theme for the U.S. economy is that the goods sector is carrying the day for jobs growth. Mining, construction and manufacturing were exceptionally strong job sectors in August while the services sector was sluggish. Manufacturing trends are swinging up while services jobs trends are swinging down. The goods sector added 70K jobs in August while private services added only 95K.

The job creating in manufacturing is a new story. Manufacturing has created over 80K jobs in the last three months in the U.S. This is as many jobs as it created in the previous 24 months. Since September of 2007, the three-month gain in manufacturing jobs has been greater than the last three months only four times. It would appear that U.S. manufacturing job creation is now a real phenomenon. Taken as a whole, the goods sector has 16% of total jobs, but this month it created 45% of all the month's job growth. It is an unusually high proportion.

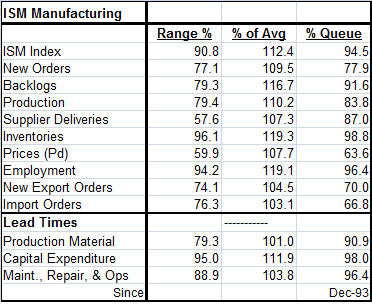

The small table below shows the various components of the ISM evaluated using several comparison schemes. In the queue of values since 1993, the ISM itself has a 94.5 percentile standing, implying that it has been this high or higher only 5.5% of the time on this timeline. Only the job component has a relatively higher gauge at a 96.4 percentile standing. The economy still is not building inflation pressure as the index for prices paid has only a 63.6 percentile standing. Prices are rising; they are above their median gain (which occurs at a value of 50 on the queue standing) but not by a lot. After prices imports and exports are the next weakest components, but they still have firm queue standings. There is no evidence that the U.S. rebound is led by trade in any way or by international forces since exports and imports both lag other components (and do so on all the gauges in the table). In fact, it appears that the U.S. manufacturing recovery is home-grown and that may be because of the President's strong language and forceful stance to dissuade US-based firms from moving operations overseas. This is one place where despite many other challenges, the President may be able to claim a clear victory. Still, time will tell if these metrics hold up.

In the discussion above, I have evaluated the ISM and its components as a queue standing among its historic data points. They can also be evaluated in the table as a percentage of average or as percentile position in its historic high-low range. All these metrics in the table show strong readings.

On balance, the ISM manufacturing index was stronger than expectations and is now at a relatively elevated position. In its history back to 1950, the index has been higher about 16% of the time, but the employment reading still has only been higher about 5% of the time. Order backlogs also are exceptionally high. The ISM is turning out some historically impressive signals. There has been some revival in the sector that is not explained by the mediocre health of the economy or by productivity. And retaining jobs and bringing them back home has been a focus of this President. This is a nice surprise on Labor Day weekend.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief