Global| Nov 02 2009

Global| Nov 02 2009U.S. Home Prices On The Rise; Distressed Sales Matter

by:Tom Moeller

|in:Economy in Brief

Summary

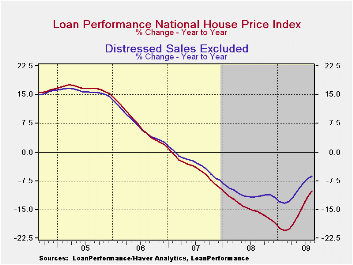

Without question, the sales price of most homes is under pressure. Demand is down and supply is up. Nevertheless, home prices recently have turned around after a decline that began early in 2006. On a month-to-month basis home prices [...]

Without question, the sales price of most homes is under

pressure. Demand is down and supply is up. Nevertheless, home prices

recently have turned around after a decline that began early in 2006.

On a month-to-month basis home prices have risen for the last five

months, as measured by First American CoreLogic. Moreover, the y/y

decline is half that logged early this year. Nevertheless, prices still

are down 10.1% from August of 2008 and they have fallen 28.1% from the

peak during the spring of 2006.

Without question, the sales price of most homes is under

pressure. Demand is down and supply is up. Nevertheless, home prices

recently have turned around after a decline that began early in 2006.

On a month-to-month basis home prices have risen for the last five

months, as measured by First American CoreLogic. Moreover, the y/y

decline is half that logged early this year. Nevertheless, prices still

are down 10.1% from August of 2008 and they have fallen 28.1% from the

peak during the spring of 2006.

Until 2006, measuring the degree to which prices were affected by distressed sales hadn't been much of an issue. Recently, however, it has become relevant in providing perspective on home price performance. When distressed sales are stripped out prices also are down y/y, but the depth of the decline is less dramatic than the total. These prices have risen for just the last four months, but the y/y change of -6.3% is notably moderate. Since the peak these prices have fallen 20.8%.

The Loan Performance House Price Index (HPI) is a repeat-sales index that tracks increases and decreases in sales prices for the same homes over time. This approach provides a more accurate "constant-quality" view of pricing trends than basing analysis on all home sales. The data are developed by First American CoreLogic and are available from Haver's USECON database. Seasonal adjustment of the data is done by Haver Analytics.

Residential

and commercial real estate is the title of this morning's

testimony by Jon

D. Greenlee, Associate Director, Division of Banking Supervision and

Regulation

and it can be found here here.

| House Price (SA) | August | July | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|

| Total (year-to-year) | -10.1 | -11.7 | -14.6 | -4.4 | -7.1 |

| month-to-month | 0.7 | 1.5 | |||

| Distress Sales Excluded (y/y) | -6.3 | -6.9 | -10.9 | -3.0 | -6.8 |

| month-to-month | 0.1 | 0.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief