Global| Nov 27 2017

Global| Nov 27 2017U.K. Services Survey Weakens As Brexit Forces Play Out

Summary

The quarterly U.K. service sector survey by the CBI weakened in Q4. The assessment is for weakness and the prognosis is for weakness. There is really only one response that is truly strong and it is inconsistent with the other [...]

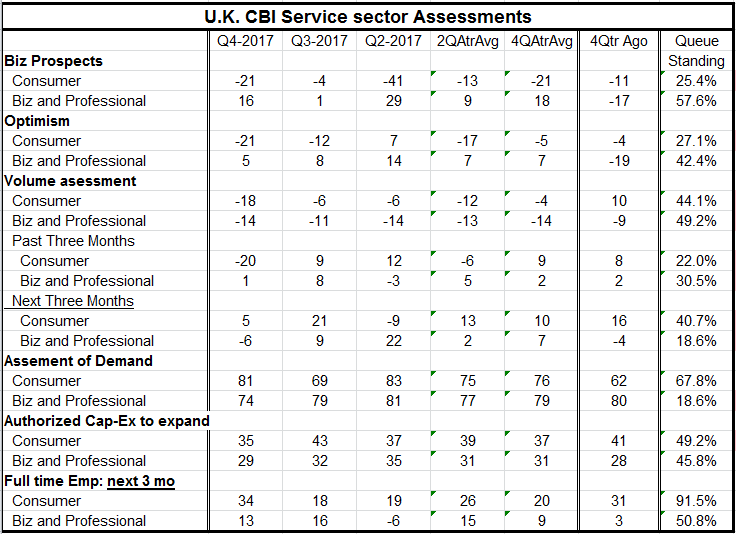

Of 16 metrics on the health of the sector only four bear readings above 50 on a queue standing basis. That means that only four of sixteen responses rate an above-median reading. Those four sectors and their respective standings are (1) full-time employment expectations for three-months ahead in the consumer sector (91.5%), (2) three-month ahead full-time employment expectations in business and professional occupations (50.8%), (3) the assessment of demand in the consumer sector (67.8%) and (4) business prospects for businesses and professionals (57.6%).

Two other sectors are on the cusp of their median values: The consumer sector for capital spending authorizations (49.2%) and the volume assessment for businesses and professionals (49.2%).

We assess five of sixteen of these readings as exceptionally weak (below a 30th percentile queue standing): (1) the assessment of demand for businesses and professionals (18.6%), (2) the volume assessment for the next three-months for businesses and professionals (18.6%), (3) the volume assessment for the past three-months for consumer industries (22%), (4) consumer business prospects (25.4%), and (5) consumer optimism (27.1%). Close to the draconian line of demarcation is the past three-months' of volume assessment for businesses and professional at 30.5%.

The rest of the readings are sluggish, below their medians but not disturbingly weak. Still, it is a relative down beat assessment for the service sector as a whole. The consumer sector has a litany of weak readings but also has a strong outlook for employment three-months out. The percentile standing for employment three-months out is more than double the standing for the volume assessment for expected business three months out. Business and professional employment expectations have the same sort of imbalance at a lower level with full time employment expectations at a 50.8 percentile standing while future volume assessments are at their 18.6 percentile, less than half the standing of employment expectations.

Still both sectors possess near median authorizations for capital expansion - that's not much of a counterpoint to anything except to extreme weakness.

On balance the CIPS survey is soft and its brightest readings are built on an inconsistent foundation. Employment expectations are solid to strong while future sales assessments are weak to nearly disastrous. Clearly there are concerns here about the state of domestic demand in a post Brexit world in the U.K. If we exclude the buoyant and seemingly out of place employment expectations, the average consumer Vs business and professional expectation stands at its 39.5 percentile for the consumer and at the 37.5 percentile for businesses and professionals. Those are highly similar and sour readings, ten points or more below their respective medians. The service sector which is for the most part a domestic oriented sector will have to survive on the income Britons are earning in the wake of Brexit whatever that is. For now there is a lot of skepticism and a good deal is unknown about that. Clearly the U.K. will be losing a lot of high-end jobs and incomes as EU organizations leave the U.K. and as much of the (high paid) financial sector finds another home so it can do business in the EU. All of this will deplete the income base in the U.K. which is what supports the service sector. The down beat assessment of the survey is not surprising. And the employment gauge may be an artifact reflecting that a number of foreign workers laboring in the U.K. are leaving and many are concerned about their prospects in the future since the U.K. will not be in the EU and the current reciprocity employment rules may not be maintained. The need to hire more in the future may be real and may only reflect the need to hire to replace workers that are leaving because of Brexit.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief