Global| Feb 16 2018

Global| Feb 16 2018U.K. Retail Sales Slip Again

Summary

U.K. retail sales growth rates have been slipping steadily since late 2016. As the U.K. gets closer to the Brexit action point, it loses more business, more jobs and more confidence. As one of the new strategies, Britain will try to [...]

U.K. retail sales growth rates have been slipping steadily since late 2016. As the U.K. gets closer to the Brexit action point, it loses more business, more jobs and more confidence.

U.K. retail sales growth rates have been slipping steadily since late 2016. As the U.K. gets closer to the Brexit action point, it loses more business, more jobs and more confidence.

As one of the new strategies, Britain will try to purse a plan more favorable to London that the City has backed for some time. Still, Brussels has showed no receptivity to a more favorable treatment of London.

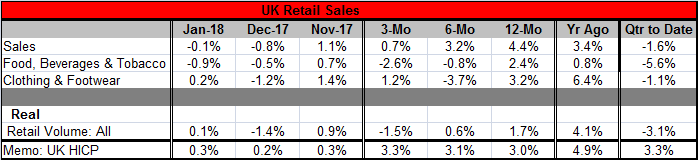

U.K. retail sales fell by 0.1% in January after a 0.8% decline in December. There 12- to 6- to 3-month growth rates have ratcheted sequentially lower. Sales are up by 4.4% over 12 months, but that pace has slowed to 0.7% (annualized) over three months.

Real retail sales volume is doing much worse. Retail volumes are up by 1.7% over 12 months, at a 0.6% pace over six months and at a -1.5% pace over three months.

The Bank of England has got off its easing track and begun to hike rates. However, after setting that course, it did not follow up its initial move with a second hike. It has since warned that it may need to raise rates sooner and more substantially than it earlier planned. That announcement boosted sterling, a result that by itself will help to stifle stubborn inflation. Still, inflation is running at a 3.3% pace over three months and it is also on an accelerating path from 12-month to six-month to three-month, but that path has a very flat gradient of acceleration.

The question for the BOE is whether it sees the economy as strong enough to be able to absorb rate hikes. The BOE itself kicked off the inflation cycle by dropping rates sharply in the wake of the Brexit vote to cushion the economy. That undercut the pound sterling and helped to ignite inflation. To raise rates more aggressively now and push sterling back up as the deadline for the introduction of the de-integration process get closer hardly seems like a wise move.

The question for the BOE is whether it sees the economy as strong enough to be able to absorb rate hikes. The BOE itself kicked off the inflation cycle by dropping rates sharply in the wake of the Brexit vote to cushion the economy. That undercut the pound sterling and helped to ignite inflation. To raise rates more aggressively now and push sterling back up as the deadline for the introduction of the de-integration process get closer hardly seems like a wise move.

While Governor Mark Carney generally gets very high marks for his leadership, accelerating the path of rate hikes now for the U.K. would be a blot on his resume. Winter is coming. Brexit's day of reckoning is coming. It is not time to throw water on the hearth fire. The 'Agents survey' is reporting some plans for stepped up wage agreements at 3.1% for the year ahead. Thus far, there has been little evidence of knock on effects from the rising import prices that have fueled the domestic inflation measures. But if the wage gains are too large, the BOE may have no choice but to lean against them.

I suppose one lesson from this is the old expression that 'no good deed goes unpunished.' Carney and Co at the BOE thought their forward-looking assistance for the economy was necessary. Instead, U.K. growth has held up better than expected and their move instead introduced a jolt of inflation. The presence of inflation changes the risk matrix for policy. Now inflation seems to have become a bit more entrenched- not seriously entrenched- still it is more of a feature of the economy than it was before. And with this new hum of inflation, the BOE is looking at a different menu of tradeoffs. Unfortunately, retail sales growth that has started to contract in real terms and slower vehicle sales are not exactly the preferred backdrop for rate hikes. Overall GDP is slowing too. Inflation continues to be stubborn. The tick up in wage inflation is more uncomfortable than it is dangerous since in most Brexit scenarios businesses and jobs will leave the U.K.; that is another reason to show policy forbearance now. However, it all puts the BOE on the horns of a dilemma. And this one is a synthetic dilemma created by the BOE's own attempts to cushion the economy and extend growth. And so this is just another example of how hard it is to do that and to balance artificially induced stimulus even with well-known and well-timed policy shocks. Even when you know more or less what is coming and when it can be hard to avoid some realities or even to diminish their impact without making things worse.

Think of it this way. It's like watching your favorite football team slowly lose a game. You may see it and be uncomfortable and even think you could go out there and help. But you know that if you did that, things would only get much worse. Sometimes policy, like the football fan, needs to sit in the stands and let the game unfold in front of it. Sometimes cheering for the right thing or even picking up the pieces after a failed event is all that you can do. Of course, you can always step in and make things worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief