Global| Oct 22 2015

Global| Oct 22 2015U.K. Retail Sales Show Some Life

Summary

U.K. retail sales surged in September, rising by 1.4% after a 0.8% August decline. Clothing and footwear sales remained weak in August as they fell by 1.8%, their second fall in three months. Food and beverage spending rose by 2.3% in [...]

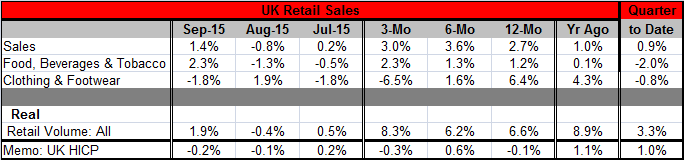

U.K. retail sales surged in September, rising by 1.4% after a 0.8% August decline. Clothing and footwear sales remained weak in August as they fell by 1.8%, their second fall in three months. Food and beverage spending rose by 2.3% in September, but that was after two straight months of declines. Overall, however, sales have been much more consistent and consistently positive. Overall sales show one decline in three months and firm growth over three months, six months and 12 months at a pace ranging from 2.7% to 3.6%.

U.K. retail sales surged in September, rising by 1.4% after a 0.8% August decline. Clothing and footwear sales remained weak in August as they fell by 1.8%, their second fall in three months. Food and beverage spending rose by 2.3% in September, but that was after two straight months of declines. Overall, however, sales have been much more consistent and consistently positive. Overall sales show one decline in three months and firm growth over three months, six months and 12 months at a pace ranging from 2.7% to 3.6%.

Real retail sales rose by 1.9% in September, rebounding from a 0.4% August drop. Real sales are very strong, rising at a pace ranging from 6.2% to 8.3% over 12 months, six months and three months.

Over this period, U.K. prices have been weak and declining on many horizons. Deflation is back.

Other retail signals are somewhat mixed even if not negative. U.K. consumer confidence declined in September and is now at its lowest level since May of this year. However, in a broader framework, confidence is still in the top 10% of its historic range and in the top 18% of its two-year range; very solid standings. Moreover, the CBI retail survey is very upbeat with September sales as well as the October outlook in the top 5% of their historic queues of observations.

The Bank of England has kept policy unchanged, but now there is one dissent to this stability on the monetary policy committee. In the U.K. as in the U.S. (where the last policy meeting also brought forth one dissent), there is some restlessness about keeping interest rates so low for so long. Just as that theme of patience-lost was starting to play out, however, weakness in China triggered global market declines and it is no longer clear if there is more than one vote for tighter policy in the U.S. or in the U.K.

To be sure central bankers and policymakers of all stripes are watching global events. The unhinging of growth in China - which now claims to have essentially hit its new growth target of 7% - has set shivers across the global economy. Weaker demand for oil and other commodities has weakened prices and set a wave of weakness through developing economies that earn their growth through the sales of these goods.

The BOE's policies have helped to keep the U.K. economy on an even keel; nevertheless, now deflation has visited again, muddying the outlook. In Europe, the ECB's policies, which brought quantitative easing late to the game, have yet to bear fruit. But Mario Draghi talks positively about these policies being effective. In Japan, monetary policy seems to have lost its punch as trade deterioration is the newest impediment to growth there. In the U.S., conditions that had seemed to turn on the greenlight for a Fed rate hike have receded. The Fed is now in a quandary. International monetary policy is at a crossroads.

Because of the global environment, the U.K. is also on an uncertain growth path. Conditions still seem to be pro-growth, but there is weakness all around and there is now deflation as well. The bounce in retail sales in September is encouraging and it keeps the growth of retail sales on a firm pace as well. Policymakers need as much stability as they can get in these times of heightened uncertainty. The U.K. retail sector seems to provide that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.