Global| Sep 18 2014

Global| Sep 18 2014U.K. Retail Sales Rebound

Summary

U.K. nominal retail sales growth bounced back in August, rising by 0.2% after a 0.3% July decline. The sequential growth rates of retail sales have been extremely steady over three months, six months and 12 months around and just [...]

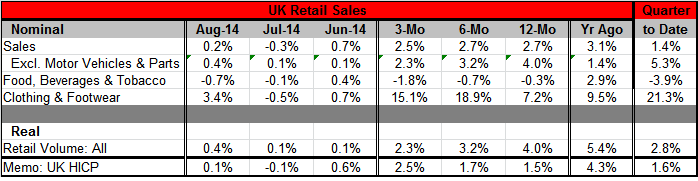

U.K. nominal retail sales growth bounced back in August, rising by 0.2% after a 0.3% July decline. The sequential growth rates of retail sales have been extremely steady over three months, six months and 12 months around and just above the 2.5% pace. Excluding motor vehicles and parts, nominal sales growth has slowed from 4% over 12 months to 2.3% over three months. Food, beverages and tobacco sales have been declining steadily and more aggressively with the decline of 0.3% over 12 months, turning to a decline of 1.8% at an annual rate over three months. Clothing and footwear purchases, however, continue to be quite strong and have accelerated from their 7.2% pace over 12 months. Spending in that category is growing at a nearly 19% rate over six months and 15% pace over three months.

U.K. nominal retail sales growth bounced back in August, rising by 0.2% after a 0.3% July decline. The sequential growth rates of retail sales have been extremely steady over three months, six months and 12 months around and just above the 2.5% pace. Excluding motor vehicles and parts, nominal sales growth has slowed from 4% over 12 months to 2.3% over three months. Food, beverages and tobacco sales have been declining steadily and more aggressively with the decline of 0.3% over 12 months, turning to a decline of 1.8% at an annual rate over three months. Clothing and footwear purchases, however, continue to be quite strong and have accelerated from their 7.2% pace over 12 months. Spending in that category is growing at a nearly 19% rate over six months and 15% pace over three months.

Inflation-adjusted sales volumes are depicted in the chart above. The year-over-year growth rates remain high. In August, sales volumes grew by 0.4%, accelerating from their 0.1% pace in June and July. The volume growth rate has been slipping steadily, however. Volume growth is at 4% over 12 months, 3.2% over six months and 2.3% over three months.

U.K. data have turned a little mixed recently. Today September U.K. industrial orders, in a Confederation of British Industry survey, fell back to indicate a negative balance between the number firms with orders increasing and the numbers with orders decreasing. Mortgage lending still seems to be moving ahead with solid growth rates on mortgage extensions.

Today, however, economic statistics are not going to be in the headlines that investors look to read about the United Kingdom. Today they will be looking for stories and polls about the vote in Scotland as they wonder exactly what the U.K. is destined to be in the future. The polls on the `yes' - `no' balance have been quite close. Some have concerns that they may not have properly weighted the influence of potential younger voters. However, all the speculation is due to come to a halt later today as the actual results of the vote are made known. This poll and any information about it that the press can scrabble up today, is going to be what people are interested in, not economic figures. And that's appropriate. This is an extraordinarily important time for both Britain and for Scotland.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief