Global| Apr 19 2018

Global| Apr 19 2018U.K. Retail Sales Fall

Summary

U.K. GDP is expected to cool its jets when the first quarter GDP number is released. The National Institute of Economic and Social Research (NIESR) estimates that U.K. GDP rose by 0.2% in Q1 2018. That translates into an annualized [...]

U.K. GDP is expected to cool its jets when the first quarter GDP number is released. The National Institute of Economic and Social Research (NIESR) estimates that U.K. GDP rose by 0.2% in Q1 2018. That translates into an annualized quarterly gain of less than 1%.

U.K. GDP is expected to cool its jets when the first quarter GDP number is released. The National Institute of Economic and Social Research (NIESR) estimates that U.K. GDP rose by 0.2% in Q1 2018. That translates into an annualized quarterly gain of less than 1%.

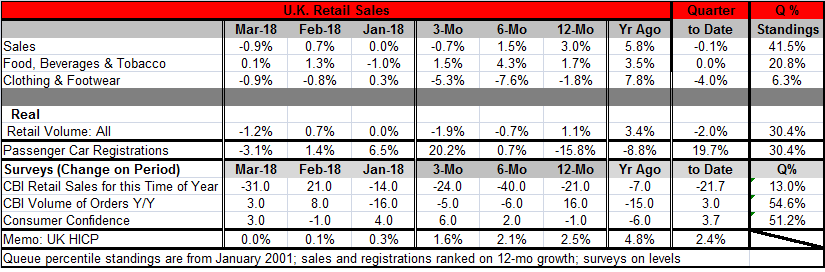

We see that weakness evident in U.K. retail sales that have fallen by 0.9% in March and are falling at a 0.1% annual rate in Q1 2018. In volume terms, U.K. retail sales are very weak, falling by 1.2% in March and dropping at a 2% annual rate in Q1 2018.

U.K. real and nominal retail sales are showing clear decay in their sequential rates of growth. Real sales grow by 1.1% over 12 months then contract by 0.7% over six months and are falling even faster at a 1.9% annual rate over three months.

Sales in the U.K. are not unraveling, but there is a clear slowing in place. The U.K. is battling several different sorts of problems. The post-Brexit sharp drop in the pound sterling introduced inflation causing the Bank of England to reverse course and start to hike rates. While the rate hike process has begun, the BOE has hiked rates only once and has been showing restraint in offering up another hike. The Brexit process is still in transition and no one is quite sure where it will lead. The government is currently involved in interparty warfare over the right approach. It goes without saying that U.K. businesses do not have a clue at this point what the future will offer them. Theresa May wants to break out of the EU customs union and be free to cut her own trade deals while parliament wants to explore options of staying in the EU’s customs union arrangement.

The Confederation of British Industry (CBI) retail survey shows a sharp drop this month for sales at this time of year. That measure shows substantial declines as well over three months, six months and 12 months. The CBI survey for the volume of orders measured on a year-over-year basis has risen in each of the last two months. But it is lower on balance over three months and six months but higher over 12 months. The CBI readings are survey metric, not growth rates. Consumer confidence on the GfK measure has been edging higher, but the reading is lower on balance over 12 months.

Turning to broader measures, the percentile standing parameters place each of the economic diagnostic measures in a queue expressing the position as a percentile standing among all other observations. All the retail sales measures are below the 50th percentile mark. That means that all of them are below their respective median year-on-year percentage gains since January 2001. The all-important retail volume reading is in its 30th percentile, with its annual gain in the bottom one third of its historic que of year-on-year percentage changes. Passenger car registrations are in step with this weakness as well. The queue standing for the consumer confidence and the CBI readings are weak, but generally better than for retail sales. Confidence and the volume of orders have standings marginally above their respective 50th percentiles. The ranking of retail sales for ‘this time of year’ is lower on 13th percent of the time. That is not encouraging.

Retail sales are weak and they are losing momentum. U.K. GDP has slowed. Inflation has slowed as well, but it remains above the BOE objectives. Growth is moderate and the future is unclear. The U.K. economy has lost momentum and faces an uncertain future with clear challenges ahead. Interest rates already are low. And the Bank of England has seen how dangerous it is to try to use interest rates to leverage the economy. While U.K. economic performance to this point has been remarkably good considering the circumstance, it is beginning to look like the future is becoming less hospitable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief