Global| Oct 18 2018

Global| Oct 18 2018U.K. Retail Sales: Doing Well-As-Can-Be-Expected Despite September Drop

Summary

The U.K. is being buffeted by many forces these days. But the pummeling it is taking over Brexit is surely the number one feature being watched by the U.K. consumer/worker/citizen. Still, U.K. retail sales and growth have all held up [...]

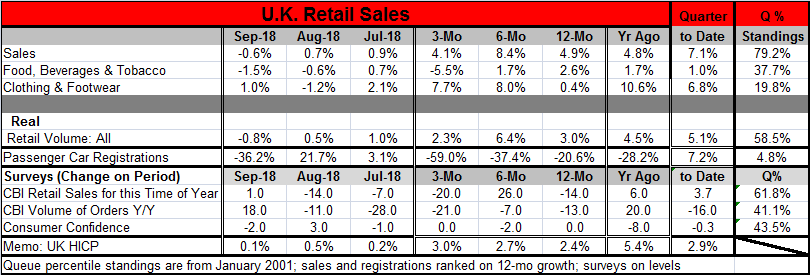

The U.K. is being buffeted by many forces these days. But the pummeling it is taking over Brexit is surely the number one feature being watched by the U.K. consumer/worker/citizen. Still, U.K. retail sales and growth have all held up remarkably well- so far. Depending on the deal that the U.K. gets, the jury is still out on what happens to investment in the U.K. although in banking a lot of firms already have left. Still, retail sales in September are up by 4.9% over 12 months and sales volume is up by 3%. Both of those are very respectable results. But in September, the monthly result is more of an eye-opener. Nominal September sales fell by 0.6% after a 0.7% rise in August. What’s worse is that sales volumes fell by 0.8% in September after a smaller 0.5% rise in August.

The U.K. is being buffeted by many forces these days. But the pummeling it is taking over Brexit is surely the number one feature being watched by the U.K. consumer/worker/citizen. Still, U.K. retail sales and growth have all held up remarkably well- so far. Depending on the deal that the U.K. gets, the jury is still out on what happens to investment in the U.K. although in banking a lot of firms already have left. Still, retail sales in September are up by 4.9% over 12 months and sales volume is up by 3%. Both of those are very respectable results. But in September, the monthly result is more of an eye-opener. Nominal September sales fell by 0.6% after a 0.7% rise in August. What’s worse is that sales volumes fell by 0.8% in September after a smaller 0.5% rise in August.

Still, in the quarter just completed (Q3 2018), nominal sales are up at a 7.1% pace and sales volumes are up at a very solid and strong 5.1% pace. If there is some slowing from those parameters, it is not a surprise or a problem. But retail sales are by their nature unruly, and despite the context whenever a sales figure moves lower abruptly, it rightly gains attention and garners some concern. No one knows what next month with bring. Will sales rebound or is there a problem, even one long in the making, cumulating?

U.K. passenger car registrations also have fallen sharply in September, but this was after a strong gain in August. Moreover, this is a European wide phenomenon as new emissions tests and standards are being phased in. Automakers ran promotions ahead of the new incentives to clear out noncompliant stocks. This had the effect of boosting August sales and robbing from September. So this is not a separate U.K. effect, but it is nonetheless real. It just is not part of a signaling mechanism about the health of the U.K. economy.

The CBI sales survey has been more suspect about retail sales with a small rise in September after two months of heavily negative readings for both nominal sales and sales volumes.

For their part, consumers are more of a drag in terms of their attitudes. Consumer confidence (GfK measure) fell in September but is unchanged over three months and 12 months. But the standing for the level of confidence is only in the 43rd percentile of its historic queue of values, a below-median showing. Clearly, consumers have been spending better than how they have been feeling.

Beyond sales trends and Brexit conditions

With the U.K. in a stare-down contest with the EU over the terms of the Brexit divorce, there is persisting concern about how the economy is behaving in the presence of all the uncertainty that is generated. The reality is that the coming break up is more like Tammy Wynette’s heart rending ‘D-I-V-O-R-C-E’ than like Neil Sedaka’s light-hearted ‘Breaking up is hard to do.’ The Sedaka tune is intended more for a teenager with little at risk and a novice at love; while the Wynette song brings to bear all the separation anxiety of a pair joined for a long time with a lot of mutual assets and friends with clear dislocations to be dealt with. Surely, that is a better rendering of the conditions of separation under Brexit.

As for the Bank of England, it has steadied itself recently. Inflation seemed to be topping up, but it is now up by ‘only’ 2.4% over 12 months, an excessive rise that is made less painful by the fact that the inflation gauge rose by just 0.1% in September.

U.K. trends for spending are a bit up in the air. The year-on-year trends look good, but the monthly result is weak and the three-month trend results are held up by previous months. So we can view retail sales as in play from a policy standpoint. There might be enough weakness to cause the BOE to have some forbearance in the event of continuing inflation overshooting.

Brexit in motion

The British Brexit talks have not gone well. But even the Swiss have been finding the EU an immoveable object in their quest to become a full-blown EU member with four years of haggling under their belt and little to show for it. The EU is concerned with the potential for ‘rogue states’ within. Clearly, this set of negotiations being conducted by bureaucrats who are afraid of what comes next and are very aware that there is a lot of internal dissent in the EU. Their fear is a new song entitled ‘P-R-E-C-E-D-E-N-T.’ The U.K. referendum on leaving was a lone act not followed in any other EU member nation. And while a lot of polls show that EU/EMU members generally want to stay together despite some very deeply held concerns, the U.K. pre-referendum poll had offered up much the same of what turned out to be bad analysis. No EU member is eager to test those waters at home. In fact, many of them still are ‘angry’ that the U.K. offered its people such a choice and put each of them on the spot as well.

There is also a hot internal conflict currently underway in the EMU and the European Commission seems determined to firmly establish and enforce its authority. This one is in a somewhat subtle yet very much a knock-down drag-out fight with Italy over budget rules. Early in the EU, both Germany and France violated budget rules in 2003 and then banded together to avoid sanctions and then acted to up the ante should anyone else transgress (here). They escaped any sanctions. Conversely, Italy has been under and long yoke of austerity and has said ‘basta.’

The U.K. left the EU because of its border rules. Italy is angry over the excessive burden of migrant care it has been left to absorb, buttressed by little support from the EU as well as with the legacy of austerity and what that has done to the Italian economy; net shrinking in GDP ten years after the financial crisis and Great Recession. In Alice in Wonderland, Alice had it easy she possessed a pill to shrink and another to reverse it. Italy does not possess a reversal pill.

In Germany Angela, Merkel’s coalition has gone to dust over migrant issues and the EU is nowhere close to solving its migrant problems. The EU Commission’s solution/approach is a heavy handed strict enforcement of rules that benefit some members and bury others. Italy, one of the two countries most buried by this rules enforcement scheme, has just lodged a complaint with France because French police drove two ‘foreigners’ over the border and dumped them in Italy…Ciao, Bella! President Macron has been very critical of Italy and of is closing its borders to any more migrants especially by sea. What is the trade-off here: two if by land, thousands if by sea?

The U.K. Brexit wrap

The EU is apparently offering the U.K. an extra year extension to negotiate, but Teresa May only thinks a few months might be necessary. It all depends on what can be agreed too. May apparently feels a deal is close at hand while her EU counterparts apparently are not about to give in on what have been the last sticking points. And the EU is apparently very concerned lest it be viewed as putting up a weak front that might encourage other members to leave and take an external deal like the one the U.K. ‘might yet get’. So take all of this, package it up, and put in the consumer’s knapsack and ask what does it all mean to him or her? With all this going on, it is surprising that the U.K. consumer has done as well as he and she have done. And it is not surprising the confidence has been suppressed. As time passes, the future hardly gets any easier to see. It is strange to see what passes for progress here.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief