Global| Feb 09 2018

Global| Feb 09 2018U.K. Manufacturing Breadth and Strength Are Moving Together

Summary

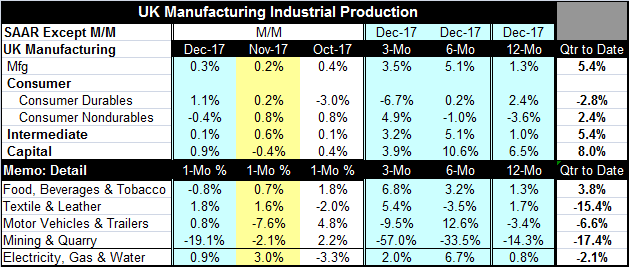

U.K. output advanced again in December, marking six straight months in which manufacturing IP has risen month-over-month. Manufacturing output is sold at a gain of 3.5% over three months; it is not as strong as it is over six months [...]

U.K. output advanced again in December, marking six straight months in which manufacturing IP has risen month-over-month. Manufacturing output is sold at a gain of 3.5% over three months; it is not as strong as it is over six months where the pace is 5.1%. Still, three-month output growth is ahead of its year-on-year pace of 1.3% in manufacturing.

U.K. output advanced again in December, marking six straight months in which manufacturing IP has risen month-over-month. Manufacturing output is sold at a gain of 3.5% over three months; it is not as strong as it is over six months where the pace is 5.1%. Still, three-month output growth is ahead of its year-on-year pace of 1.3% in manufacturing.

By sector, durable goods output is declining over three months and on a clear decelerating profile from 12-month to six-month to three-month.

Just as clearly nondurables output is on an accelerating path, putting declines over 12 months and six months behind it to log a strong 4.9% pace over three months.

Intermediate goods and capital goods show mixed results. Both show positive growth rates. But for intermediate goods, output accelerates over six months then decelerates over three months, but growth over three months is much higher than its pace over 12 months. For capital goods, the growth rates are stronger than for intermediate goods with acceleration over six months, deceleration over three months and a three-month rate of growth slower than its impressive 12-month gain. Capital goods output shows consistent strength in its growth rates, but it does not show any tendency to accelerate.

The quarter-to date (QTD) shows a very strong 5.4% rate of output expansion. Growth QTD is very strong at an 8% pace for capital goods. Intermediate sector growth matches headline growth. Both consumer goods categories fall short of the overall mark with durable goods output actually declining. Consumer goods output is not strong here. Nor is it strong in December in Italy or in Germany or in France where durable goods trends have fallen to a rag-tag trend. Consumption still seems to be a weak spot in the EMU. EMU nations are producing for the capital goods sector more than anything else. And that is a fact about developing growth that is a bit unsettling. Globally, supply has been abundant for some time. It is demand, especially consumer demand that has been lacking globally. It is not really on stream yet despite some growth optimism. In the U.S. where the consumer has revived, it seems to be on some false or temporary trends. Consumer staying power is still a question for this expansion.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief