Global| Sep 12 2017

Global| Sep 12 2017U.K. Inflation Moves Even Higher

Summary

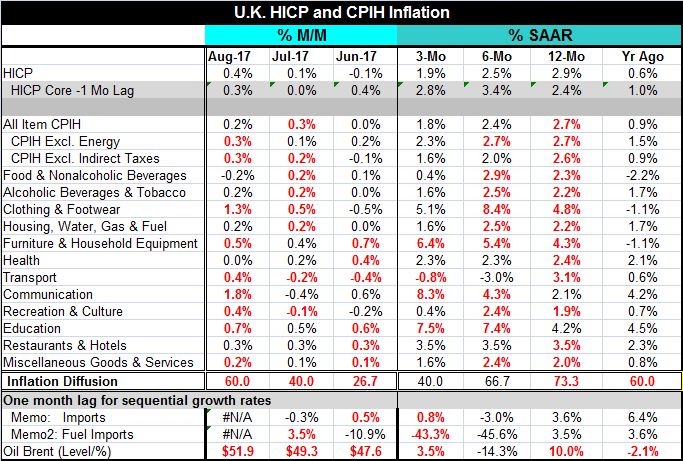

The U.K. CPIH inflation rate rose by to 2.7% over 12 months from 2.5% last month. The HICP headline rose to 2.9% from 2.6% last month. The CPIH also gained 0.2% in August with the ex-energy rate up to 0.3%. HICP U.K. inflation gained [...]

The U.K. CPIH inflation rate rose by to 2.7% over 12 months from 2.5% last month. The HICP headline rose to 2.9% from 2.6% last month. The CPIH also gained 0.2% in August with the ex-energy rate up to 0.3%. HICP U.K. inflation gained 0.4%. Both headline rates are below 2% over three months, at 1.9% for the HICP and 1.8% for the CPIH. But both headlines show an excessive pace of inflation over six months and 12 months as those rates of change exceed the 2% speed limit. Still, there is evidence of some cooling down as the CPIH headline and core show various degrees of deceleration.

The U.K. CPIH inflation rate rose by to 2.7% over 12 months from 2.5% last month. The HICP headline rose to 2.9% from 2.6% last month. The CPIH also gained 0.2% in August with the ex-energy rate up to 0.3%. HICP U.K. inflation gained 0.4%. Both headline rates are below 2% over three months, at 1.9% for the HICP and 1.8% for the CPIH. But both headlines show an excessive pace of inflation over six months and 12 months as those rates of change exceed the 2% speed limit. Still, there is evidence of some cooling down as the CPIH headline and core show various degrees of deceleration.

Exchange rates continue to bedevil the BOE in its inflation-quest. The upsweep in U.K. inflation is breathtaking. It has followed mostly from the sharp drop of the pound sterling in the wake of the Brexit vote. That drop caused import prices to surge sharply. This month clothing and footwear prices rose at the fastest pace since the CPI series began in 1997, up 4.6% year-on-year in August. The jump was largely due to a weaker pound as the sector is highly import-intensive, according to the Office for National Statistics. Still, wages in the U.K. have lagged behind inflation. Real wages are being eroded. And there are other signs that the economy is slowing down even though the unemployment rate is still extremely low.

These facts put the Bank of England in a difficult spot. The rise in the inflation rate has given a bump to sterling as markets are beginning to handicap the prospect of a BOE rate hike. And while one may indeed be coming, the BOE still may choose to wait out the impact of a slowing economy and of eroding real wages. After all, is there any real reason to expedite the economy's trend lower? It is clear that inflation is imported and has not generally spread to domestic prices and wages. Whether the BOE cuts rates sooner or not, the slowing U.K. economy is going to bring down inflation pressures; the import price bump is an artifact of a one-time exchange rate drop. The impact on import prices will dissipate. Once that goes away, the BOE will only be dealing the special effects of oil. Brent oil prices have moved up in each of the last two months, but oil-price volatility has been reduced.

U.K. inflation and EMU inflation rates go their own way in the short run

U.K. inflation and EMU inflation rates go their own way in the short run

U.K. inflation has followed the same broad pattern as inflation in the EMU, as this chart shows. The inflation cycles are highly similar, but U.K. inflation (CPIH vs. HICP) runs about a percentage point hotter on balance in the U.K. Having its own exchange rate has given the U.K. some policy flexibility to run a slightly different policy than the the ECB. For example, the BOE took its latitude to cut rates as the end of its participation in the EU was announced. Inflation rates between the EMU and the U.K. have been the most different around turning points and it seems that we find ourselves there again. Some may pessimistically think that the U.K. has not yet got control of inflation, but it seems to me that the opposite is true. Despite the uptick in the headline rate, the slowing economy and erosion of real wages all spell the end (either here and now or soon) to the upcycle in inflation. Inflation itself is already losing momentum.

The details in the U.K. CPIH series show that inflation did accelerates in a broad-based way in August with prices rising in 60% of the CPIH categories compared to rising in only 40% in July and in 26.7% in June (see Inflation Diffusion). Prices are also advancing faster year-over-year in 73% of the items, but for only 40% over three months compared to 66% over six months. The 73% figure seems pretty decisive, but one year ago CPIH inflation was only rising at 0.9% rate; it is not surprising that with the rate up to 2.7% inflation's breadth is widespread. Inflation's breadth has gradually narrowed, however, from 12-month to six-month to three-month as the metric inflation diffusion shows us.

While oil may still be a risk to the outlook, oil price moves have been contained and even the hurricane buffeting the U.S. and affecting its prime petroleum region has failed to get much of a stir out of oil prices. Longer term, there is some evidence that OPEC may be lining up its ducks somewhat better to achieve some output restriction; but that still appears to be a slow process.

At the end of the day, the central bank has to make policy using the things it can control while making judgements about the impact of its past actions and about the things it does not control. Despite being in a patch in which inflation has gone rogue, it has not gone wild and run away. Its damage has been contained and has failed to spread in several important respects and those facts would seem to offer the BOE a chance to continue to bide its time with rate hikes. But the BOE does meet this week and we will find out more about the way it feels as we see how its members vote. Are they getting more concerned that inflation is a problem or more convinced that inflation will end on its own terms? Stay tuned for the BOE meeting this week.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief