Global| Nov 21 2017

Global| Nov 21 2017U.K. Industrial Survey Shows Some Strength As Dueling Brexit Forces Play Out

Summary

A number of U.K. reports or actions of interest have come to light over the past day or so that give us some insight into how the U.K. economy is coping with Brexit. The CBI industrial survey released this morning shows strong total [...]

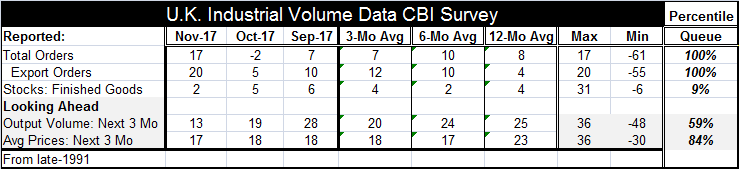

A number of U.K. reports or actions of interest have come to light over the past day or so that give us some insight into how the U.K. economy is coping with Brexit. The CBI industrial survey released this morning shows strong total and export orders readings with both at their highest levels since late-1991. There is a moderate but still positive look ahead for output volume that is nonetheless reduced from its October level and is sharply lower compared to its September level. In fact, its percentile standing has fallen from its 96th percentile just two months ago to it 59th percentile in November. Average prices are simply stuck, but in the high end of their range at the 84th percentile. This report either shows that U.K. industry is coping well based on strong orders or it features an alarming fall off in expectations for the period ahead. How are we to view it?

A number of U.K. reports or actions of interest have come to light over the past day or so that give us some insight into how the U.K. economy is coping with Brexit. The CBI industrial survey released this morning shows strong total and export orders readings with both at their highest levels since late-1991. There is a moderate but still positive look ahead for output volume that is nonetheless reduced from its October level and is sharply lower compared to its September level. In fact, its percentile standing has fallen from its 96th percentile just two months ago to it 59th percentile in November. Average prices are simply stuck, but in the high end of their range at the 84th percentile. This report either shows that U.K. industry is coping well based on strong orders or it features an alarming fall off in expectations for the period ahead. How are we to view it?

The May government is now saying that it is willing to pay more to exit the EU, but it wants something in return. We are waiting to see exactly what these demands are, but the Brexit negotiations with this step would seem to be closer to being real instead of being a pairing of talking heads talking past one-another without true dialogue.

On the same Brexit note, a German group yesterday, an alliance, dubbed a New Deal for Britain, pressed for the U.K. to stay in the EU. This alliance includes three ex-presidents of the Federation of German Industry. One of the three, Heinrich Weiss, said: "With Britain, the EU is losing its most important ally in the fight for competitiveness."

Additionally, the Belgian port city of Zeebrugge, often referred to as one of 'Britain's biggest ports,' is worried about Brexit. Zeebrugge, of course, is a Belgian port not a British port, but it services so many U.K. ports that it is importantly locked into the U.K. trade cycle and is worried about what business it will do in the aftermath of Brexit. Joachim Coens, CEO, Zeebrugge Port Authority, said that "There's no country that can really replace the U.K. for us."

It has long been recognized that pain from Brexit would be a two-way street, but stories on the pain largely have bypassed Europe or have been subjugated to reports about how the U.K. will suffer. On that score, there were stories in the press yesterday about which EU cities would attract the EU agencies currently housed in the U.K. Paris has won a battle to host the European Banking Authority (EBA). It will relocate from London after the U.K. leaves the European Union. The French capital's victory follows a win earlier for Amsterdam, which will host the London-based European Medicines Agency (EMA).

Clearly, Brexit is a stew of winners and losers and conundrums with the U.K. - Irish border question being an important remaining conundrum. But then there are the knock on effects from the U.K. leading and no telling its psychological role in Catalan decision to play a game of chicken with Spain over its autonomy and sovereignty.

Amid all these swirling and shifting relationships, pluses and minuses, and appeals to rethink Brexit, or to follow through with it, there is the Bank of England which has to make policy in this void without much of a framework. Four of the MPC committee's nine members testified yesterday in front of U.K. lawmakers. Jon Cunliffe, BOE Deputy Governor who was one of the two MPC members who voted against a rate hike, may have summed the BOE's dilemma up best. He said he shared the "overall framework" of the MPC's views on the economy but pointed out that members had different tolerances for above-target inflation. There may also be a question of exactly how the inflation process works in this more globalized economy. U.K. workers responded to uncertainties about the outlook by showing even more flexibility in their wage demands since the EU referendum, said BOE Deputy Governor Dave Ramsden. So there is a question of whether the rules have been bent beyond what economists' inflation tolerances might be. The U.S. is making policy off its low unemployment rate based on inflation 'fears' despite a clearly broken down and severely flattened Phillips Curve. That is just another example of this same dilemma. How does policy work? What are our tolerances for missing our policy targets? These are widespread central banking themes of the post crisis period; the Brexit situation has exaggerated the tradeoffs for the BOE.

Meanwhile, in Germany, Angela Merkel has been unable to establish a workable coalition that leaves her in control despite an economy that she presided over with the lowest unemployment rate since German reunification. How could such stellar economic performance fail to return her to power? Not only are economic forces working differently, but the connections between economics and politics also appear to be strained.

Brexit is no simple matter to sort out. The CBI survey suggests that British industry is weathering the storm of uncertainly quite well. However, beyond the strong orders results, there is a weaker and weakening expectation for the future. We can't be sure if that connects the dots to Brexit or not, but there is a good a chance that it does. The previous, sharp, post Brexit-vote monetary easing stimulated growth but did so at the cost of undermining the pound and ushering in a wave of inflation. This makes it clear that currency depreciation would be a two-edged sword if relied upon.

Meanwhile, Europe will have its own repercussions from Brexit and they will be a mixed bag of gains and losses. Brexit undoubtedly makes the BOE's job much harder, but there is no evidence that Brexit forces significantly impact the macroeconomic environment among EMU members enough to alter policy at the ECB.

Very clearly change and some rethinking are afoot - better late than never. I do not know if a Brexit rethink (as in revote) is possible, but it is good that Europeans are recognizing that there are two-way effects and for that realization to become part of the bargaining process. Whether the U.K. is a full member of the EU or not, those two entities need one another. It is more like a divorce with children than one without them. Both parties will have to remain civil and have an important relationship after the Brexit-up. Perhaps some of the nastier forces in Europe are beginning to see this or maybe the stiff bargaining posture is melting away to expose reality. However, these seem to be positive and largely constructive developments. And the EU must recognize that this is not just a rejection of it by the U.K. It bears some responsibility for the U.K. leaving whether it wants to admit it or not. The EU can hardly be surprised that the more it pressed into social policy the more it would hit a nerve somewhere among members. It is curious to me that EU policy has been willing to experiment so deeply with elements of social policy and yet has steadfastly kept any but the most meager fiscal integration off the books save for that which comes from dictating debt and fiscal deficit levels and what sneaks in through the back door of the ECB. But as Draghi's term draws to a close, there is talk of another German to head the ECB. And with that, the way will be shut again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief