Global| Aug 21 2018

Global| Aug 21 2018U.K. Factory Orders Remain Solid...If Clueless

Summary

U.K. order books continue to hold ground, according to the industrial trends survey issued by the Confederation of British Industry (CBI). Their net position slipped in August to 7 from 11 in July and 13 in June. Their August level is [...]

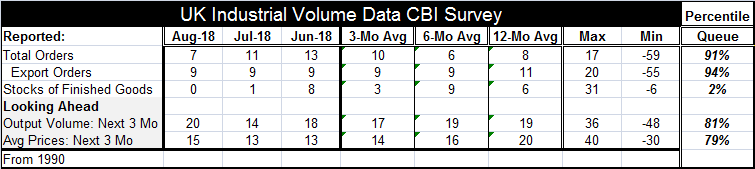

U.K. order books continue to hold ground, according to the industrial trends survey issued by the Confederation of British Industry (CBI). Their net position slipped in August to 7 from 11 in July and 13 in June. Their August level is below their past 12-month average (of 8), but it is still a solid reading. The queue percentile standing is at its 91st percentile, a relatively strong position despite some recent slippage.

U.K. order books continue to hold ground, according to the industrial trends survey issued by the Confederation of British Industry (CBI). Their net position slipped in August to 7 from 11 in July and 13 in June. Their August level is below their past 12-month average (of 8), but it is still a solid reading. The queue percentile standing is at its 91st percentile, a relatively strong position despite some recent slippage.

As Brexit negotiations have raged in the background and made little progress, U.K. export orders have been rock-solid with a net reading of 9 for three months running and in four of the last five months. Export orders are below their 12-month average of 11 but with an even stronger queue standing than overall orders at their 94th percentile.

Stocks of finished goods have a net reading of zero and have been slipping; stock level ratings are below their 12-month average and have a queue standing only in their 2nd percentile.

Looking ahead, output value expected over the next three months is increasing. The net reading is at 20, up from reading levels in the past few months and a tick above its 12-month average of 19. While that reading and trend is positive, the queue standing of the gauge is a bit lower than for orders in its 81st percentile, roughly a decile of standing points lower.

Average prices expected three-months ahead log a net reading of 15, a slightly stronger reading than in recent months but below the 12-month average of 20. The standing of the reading is in its 79th queue percentile, a relatively firm position.

The Brexit ultimatum

Just about everything that is done or reported for the U.K. these days is seen through the lens of Brexit and filtered by the question of what happens next. The reporters to the survey see current conditions as quite solid and rank the future- out to three months- as still quite positive and solid. On this short leash, British industry is doing well. But what about after Brexit? Since there are no deals yet cut and the Irish border seems to be a giant sticking point, it is hard to tell.

However, in a bit of unrelated news, the U.K. fiscal budget balance ballooned to post its largest surplus for July since 2000. While the BOE may be marking time to its next rate increase and set to withdraw stimulus, the fiscal situation puts more policy flexibility into the hands of the government.

Having some policy flexibility as the Brexit negotiating period drags on is good news. But more important is that the U.K. get a Brexit deal and provide a clear framework for the conduct of business in the future. As things stand, I’m not sure that we learn too much from the CBI surveys since businesses can’t really know what lies ahead. They are not in position to handicap the future with any degree of accuracy and certainly to the extent that they do it, they do it without much foresight.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief