Global| Jul 28 2017

Global| Jul 28 2017U.K. Consumer Confidence Sinks Again

Summary

The context for understanding U.K. confidence As the chart documents, U.K. consumer confidence has been through a roller coaster. It bottomed in 2008 then jumped in 2009. It then went into a long slide that ended in 2011. Confidence [...]

The context for understanding U.K. confidence

The context for understanding U.K. confidence

As the chart documents, U.K. consumer confidence has been through a roller coaster. It bottomed in 2008 then jumped in 2009. It then went into a long slide that ended in 2011. Confidence firmed slightly though 2012 then went on a tear rising strongly to a peak in 2015. In the wake of the Brexit vote, confidence fell again and it is on another very steep slippery slope at the moment with EU-UK Brexit talks in progress ...and not going very well.

Against this volatile background, it is hard to make sense of consumer confidence and what its current reading level really means. Confidence has simply been all over the map.

The current survey

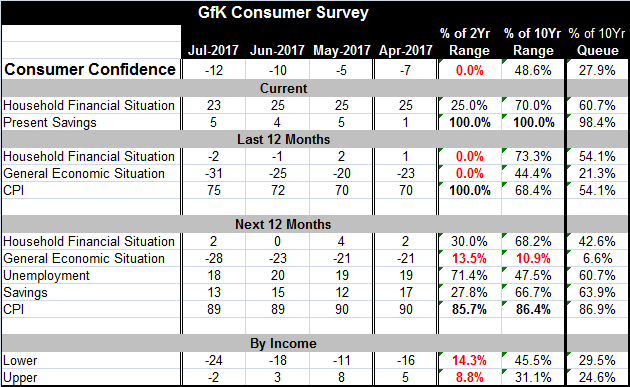

In July confidence has slipped to -12 from -10 in June and -5 in May. Confidence resides at the bottom of its two-year range and in the lower 27th percentile of its 10-year queue (or ranking of values). Still, confidence has been a lot lower than this in the recovery period and in the wake of the financial crisis.

The current financial situation is positioned in the lower 25th percentile of its 2-year high-low range and in the 60th percentile of its 10-year queue. But current savings are at the top of their two-year high-low range and in the 98th percentile of its 10-year queue of values. It looks like consumers are bracing for some bad event faced with poor finical conditions they are building up their savings.

The past 12 months

The household financial situation and the general situation over the past 12 months are both ranked as the worst over the last two years. And these two categories have moderate or weak queue standings over the past 10 years (moderate for the financial situation and weak for the general economic situation). The CPI is ranked at a two-year high and at a middling 54th queue percentile ranked over 10 years.

The next 12 months

Looking ahead over the next 12 months, the expectations are adverse. When placed in a two-year high-low ranking, the U.K. consumer sees the financial situation as in its lower 30th percentile and the general economic situation as in its lower 13th percentile. Unemployment prospects are in their 71st percentile, a relatively high and unfavorable reading. The ability to save is ranked as in the lower 27th percentile. The CPI is in its upper 15th percentile. These are an adverse collection readings and suggests a real challenge for policymakers. The ten-year queue rankings are more moderate, but as the chart reminds us the last 10 years were generally pretty grim times. Even so, the forward-looking general economic situation has a queue standing over that period that has been lower only 6.6% of the time.

By income grouping, both upper and lower income cohorts have rankings in the bottom 15th percentile of their respective 2-year high-low ranges. They also have rank standings in the lower 30th percentile of their 10-year queue standings. Neither high- nor low-income people are pleased with the prospect for economic developments.

Summing up

Clearly, a lot of the angst felt by consumers stems from the oncoming Brexit plan which is still being negotiated amid current conditions in which the EU in playing extreme hardball with the U.K. at a time that U.K. politics are in disarray. Theresa May's government hangs by a thread and seems to be embattled over a new issue almost every day. The Bank of England appears to have done about all that it can at the last round of stimulus which sent sterling reeling and as a result has set a rising inflation rate in motion. The Monetary Policy Committee with a split vote at its last meeting seems undecided about what it should do next. The consumer seems to feel all this angst and uncertainty. At this point, the prognosis is for more deterioration.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.