Global| May 21 2019

Global| May 21 2019U.K. CBI Metrics Go South

Summary

The CBI orders fell sharply in May and were last weaker in October 2016. That observation is an outlier. But from October 2015 through April 2016, orders were persistently weaker than their current reading. Export orders fell more [...]

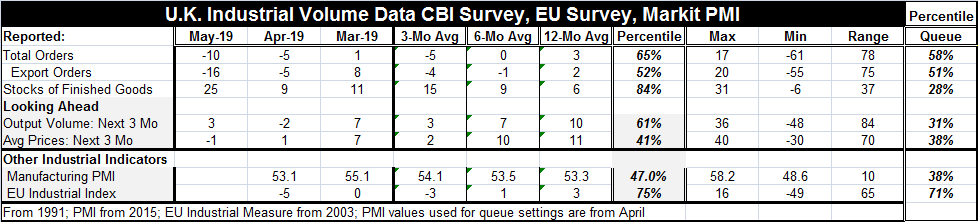

The CBI orders fell sharply in May and were last weaker in October 2016. That observation is an outlier. But from October 2015 through April 2016, orders were persistently weaker than their current reading.

The CBI orders fell sharply in May and were last weaker in October 2016. That observation is an outlier. But from October 2015 through April 2016, orders were persistently weaker than their current reading.

Export orders fell more sharply in May; they were last weaker in July 2016. Still, the rank standings for total orders and export orders are still above their historic medians with ranking in their 58th and 51st percentiles, respectively.

The looking ahead a portion of the survey sees a stronger value for May than April but May is still below March. The queue or rank standing is at the 31st percentile which puts it well below its median in the bottom one-third of its historic ordered queue of data.

Prices for the next three months slipped in May. They mark at a lower 38th percentile standing, well below their historic media.

Industrial metrics from other surveys are in the lower panel. The April manufacturing PMI for April is comparable in its standing to these May readings. The EU industrial survey reading is a lot stronger with a 71st percentile standing, but that is also for a reading that is a month older and we can see there has been substantial erosion this month (May). One month ago CBI orders had the exact same 71st percentile as for the industrial index in April. On balance, the various surveys seem to be consistent with one-another.

The U.K. is reaching a very difficult decision point. Theresa May’s talks with labor have broken off to no avail. She is on the verge of having to give up her office. She has one more Brexit proposal to put forth, but the early talk is that it too will be unacceptable.

The U.K. factions on Brexit are really dug-in and tearing at one another. The hard Brexit group seems to be in control because if there is no deal they get what they want but in a very disruptive package. Still since they can engineer that by failing to agree and support any other plan. That makes it likely that the U.K. will in fact wind up with a hard Brexit and one that is every disruptive.

Europe (EU, EMU, other) is already reeling. And financial conditions already are touch-and-go. An ever larger proportion of euro area bonds continue to come with negative yields on them. This is really not a good time for the EU to absorb such a shock either, but both sides now seem to be on auto pilot over the negotiations to which the EU has taken a ‘take it or leave it’ attitude for some time.

The only good news on the trade front globally has been the U.S. agreeing to put aside for six months the consideration of auto tariffs. China blew up the U.S.-China talks and now the state of play for those talks cannot be easily determined. China wants to have its egg foo young and eat it too. China has been disruptive, unreliable, and outlaw, unwilling to protect copyrighted material, trademarks and has forced firms operating there to turn over their technology. Now when the U.S. wants a trade bill to ensure the end to such practices, China acts as if it is being singled out for restrictive treatment. Well...of course it is. And it is because the U.S. now requires absolute safeguards to be sure there will be no return of the practices China once engaged in but has been willing to negotiate away. But China no longer is willing to offer safeguards. If China is willing to negotiate away some of the things it has been doing, why is it not also willing to provide real assurances? The excuse of a need to save face does not cut it.

This simply points up how difficult trade negotiations are. In many ways, it validates Trump’s decision to go at it bilaterally since a multilateral approach like this would be impossible. And the U.S. still has trade talks to start with the EU and Japan. There is plenty of opportunity for more shocks. But for now the mess being made of Brexit is quite enough. And it seems to be thoroughly disturbing to U.K. industry. And that’s not the end of it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief