Global| Jul 14 2015

Global| Jul 14 2015The Odd Euro Area IP Trends

Summary

In the current month with overall IP falling, it is the rich getting richer as the big four economies show advances in their national manufacturing IP output. But over the past year it is a different story. It is the austerity [...]

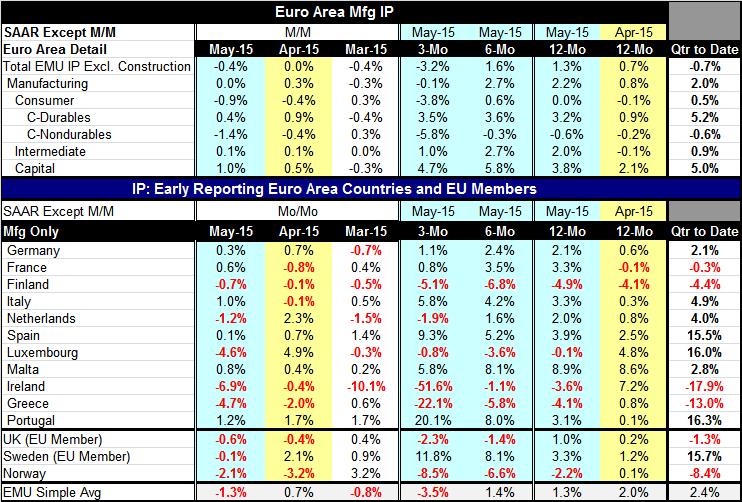

In the current month with overall IP falling, it is the rich getting richer as the big four economies show advances in their national manufacturing IP output. But over the past year it is a different story. It is the austerity countries of Portugal, Spain and Italy that have been growing among the fastest in the euro area and, best of all, with manufacturing IP accelerating steadily unlike any other country listed in the table.

In the current month with overall IP falling, it is the rich getting richer as the big four economies show advances in their national manufacturing IP output. But over the past year it is a different story. It is the austerity countries of Portugal, Spain and Italy that have been growing among the fastest in the euro area and, best of all, with manufacturing IP accelerating steadily unlike any other country listed in the table.

IP in the euro area fell unexpectedly in May. Manufacturing output increased in each of the euro area's four largest economies, Germany, France, Italy and Spain, yet overall euro area output fell.

Output in May saw declines in five of the EMU countries listed in the table. Of those, four show declines on all horizons of three-month, six-month and 12-month. Those are Finland, Luxembourg, Ireland and (of course) Greece. Oddly, output is the strongest on these sequential growth horizons in Italy, Spain and Portugal where IP is showing progressive acceleration. These austerity countries are doing exceptionally well. Greece, of course, has become the exception to the notion of austerity countries doing quite well. But Greece had been making progress until it went off the tracks and demanded changes. Not all change is for the better.

Overall EMU output in May is advancing strongly in capital goods. Intermediate goods output is up by just a tick. But consumer goods output, led by weakness in the nondurable goods sector, which is off very strongly in May, drags manufacturing output to a standstill while overall output falls into decline.

In the quarter to date (two months into Q2), overall output is falling by 0.7% but manufacturing output is up at a 2% pace as consumer goods, intermediate goods and capital goods output all expand. But within consumer goods, nondurables output is still a laggard and is still declining.

Global changes in the economic and geopolitical environment are still ubiquitous. There is a new nuclear deal with Iran that will now have to be ratified by the individual participating countries' legislatures. Greece, of course, has a deal but markets are beginning to sway, wondering if that deal will be able to pass the Greek parliament. The minority party in the current government has said that it will support the proposals that previously were on the table implying that it will NOT support the new conditions that were placed on Greece to make it a deal in the end. If the Greek parliament does not pass this proposal, very likely there will be chaos and Greece will be forced to reissue the drachma. That possibility is still very much on the table since the deal, one that must be passed in record time, is complicated and onerous to Greece. We may not have head the last word from Greece yet. And if there is another, it might not be `Opa!'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief