Global| Nov 22 2017

Global| Nov 22 2017The German Trade Surplus Expands Again; Highest Surplus Since April 2016

Summary

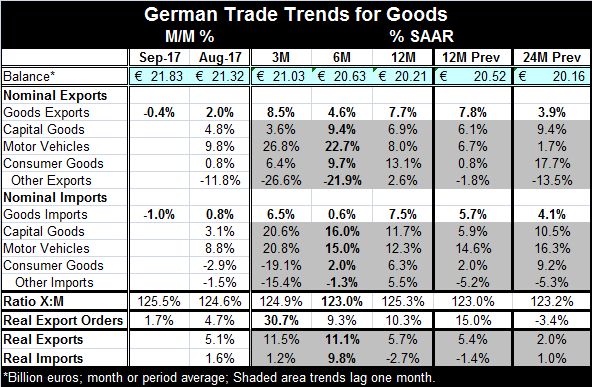

The German trade surplus in September continued to push to a higher level. The 21.83 billion euros surplus rose from 21.32 billion euros in August. It is the highest surplus since April 2016. Since January 1999, the surplus ranks as [...]

The German trade surplus in September continued to push to a higher level. The 21.83 billion euros surplus rose from 21.32 billion euros in August. It is the highest surplus since April 2016. Since January 1999, the surplus ranks as the fourth highest on record. German clearly is making no effort to address its building surplus although over the past several years Angela Merkel has rebuffed criticism of Germany's surpluses and she has insisted that the surplus is on its way lower. The question is whether Merkel has been referring to this reality or to an alternate reality. In this reality, her statements about the path of the German surplus have been completely misleading.

The German trade surplus in September continued to push to a higher level. The 21.83 billion euros surplus rose from 21.32 billion euros in August. It is the highest surplus since April 2016. Since January 1999, the surplus ranks as the fourth highest on record. German clearly is making no effort to address its building surplus although over the past several years Angela Merkel has rebuffed criticism of Germany's surpluses and she has insisted that the surplus is on its way lower. The question is whether Merkel has been referring to this reality or to an alternate reality. In this reality, her statements about the path of the German surplus have been completely misleading.

German surplus backed into its increase in September as exports fell by 0.4% and only a bigger drop in imports propelled the surplus higher. Imports fell by 1% in September. Both imports and exports had advanced in August with exports up by 2% and imports rising by 0.8%. Sequential growth rates from 12-month to six-month to three-month have no clear pattern for either exports or imports. However, both exports and imports are accelerating over three months compared to six months, but only exports have a three-month growth rate ahead of its 12-month growth rate. Export momentum appears to be still solidly in place.

The components of exports and imports lag by one month. On that basis, sequential growth rates show strong acceleration is in train for motor vehicle exports and imports alike. Also for both exports and imports, the categories 'other exports' and 'other imports' are sequentially decelerating. For imports, however, consumer goods imports also are decelerating and falling at a 19% annualized rate over three months on data up to date through August. That's not encouraging.

Of course, German real export orders continue to be strong. They accelerate sharply over three months gaining 30% on an annualized basis, compared to growth rates of about 10% over 12 months and six months.

With oil prices having been volatile, import prices, in particular, have undergone movement that could disguise easily the actual trend in import volumes. Taking 'price' out of the picture, real imports in fact have turned weak on growth at just a 1.2% annualized rate over three months That is down from a 9.8% pace over six months but a pickup from their drop of 2.7% over 12 months. However, on that same timeline, German real exports have been exceptionally strong rising at an annualized pace of 11.5% over three months, 11.1% over six months, and 5.7% over 12 months. Real exports are still accelerating for Germany as of August.

The German trade picture remains strong. Its various elements show positive momentum, more growth for real exports than for nominal exports and still strong real order growth, signaling a bright future. Germany continues to have a huge current account surplus and its strong growth and low unemployment belie the weakness in German demand for goods made abroad. Germany, despite its strength and solid domestic growth, simply is not importing to any extent at all. Instead of contributing to the spread of growth, Germany is skimming off demand growth from abroad and using it to advance its own domestic results. At a time when global growth is so weak and Germany is doing so well, it ought to have a much larger international profile contributing to the stimulus of global growth instead of living high off of demand originating in countries weaker than itself and with more budget constraints and fewer options to create growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief