Global| Jan 15 2021

Global| Jan 15 2021The EMU Trade Surplus Stabilizes

Summary

The graphic tells a clear story of recent trends. Both exports and imports have been regaining momentum after they reached a 12-month growth-rate low in March. Growth rates for exports and imports are reviving with exports leading the [...]

The graphic tells a clear story of recent trends. Both exports and imports have been regaining momentum after they reached a 12-month growth-rate low in March. Growth rates for exports and imports are reviving with exports leading the way over the last six months. Despite the revival, we are seeing a growth rates that still are showing export and import declines year-over-year. The trade surplus is stabilizing, not quite at its highest levels pre-covid-19, but at levels that are nonetheless higher relative to most of the pre-covid-19 period.

The graphic tells a clear story of recent trends. Both exports and imports have been regaining momentum after they reached a 12-month growth-rate low in March. Growth rates for exports and imports are reviving with exports leading the way over the last six months. Despite the revival, we are seeing a growth rates that still are showing export and import declines year-over-year. The trade surplus is stabilizing, not quite at its highest levels pre-covid-19, but at levels that are nonetheless higher relative to most of the pre-covid-19 period.

Trade in November

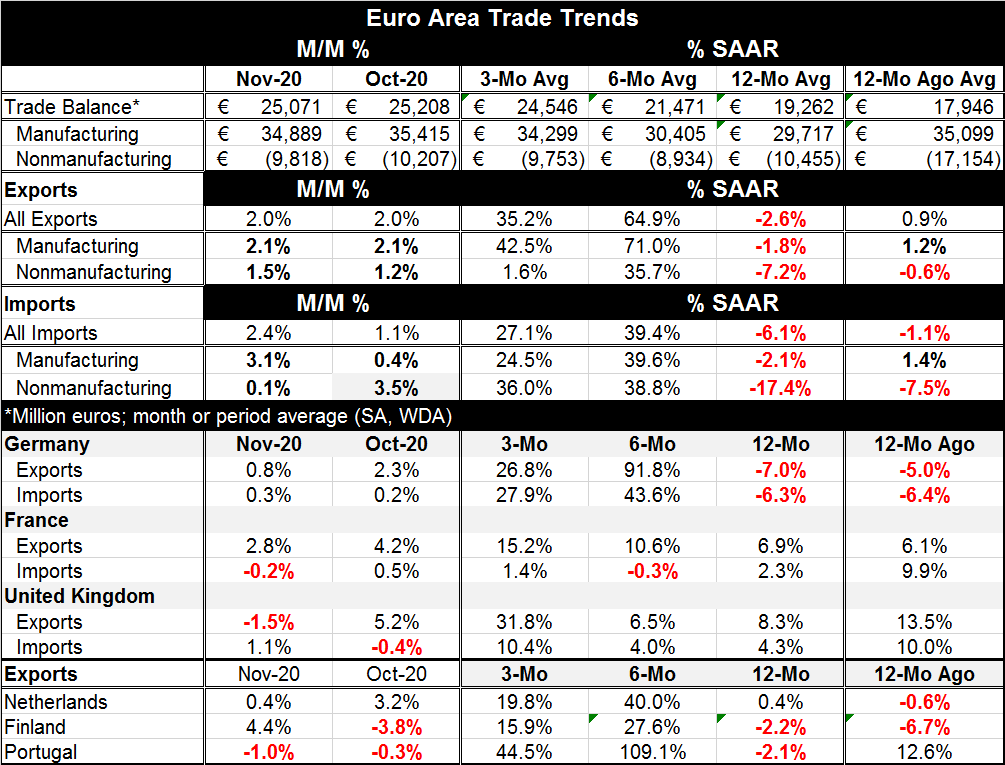

In November, both exports and imports rose with imports rising a bit faster on the month at 2.4% compared to 2.0% for exports. Underlying this overall result were trade flows in manufactured goods imports that were stronger, rising by 3.1% on the month as exports gained 2.1%. Nonmanufactured exports rose by 1.5%, outdistancing nonmanufactured imports that rose by a skinny 0.1%.

Trade trends

Trade trends are clear in the chart for year-on-year patterns. The table looks at sequential growth rates (12-months to six-months to three-months). There we see both exports and imports are falling over 12 months. Even though they have revived steadily since March, both flows are still showing net contraction. However, over six months exports surge at a 64.9% annual rate with imports surging too but lagging exports with their own 39.4% annual rate rise. Over three months, both flows continue to grow fast, but both slow compared to their respective six-month pace and exports continuing to outpace imports.

Trade patterns in manufactured goods for exports and imports mimic those same trends with annual flows contracting, six-month flows accelerating, and three-month flows slowing but keeping to a strong pace with imports generally a step or more behind exports.

For nonmanufactures, the patterns echo once again with a key difference that over three months nonmanufactured exports slow sharply while over three months imports hold their six-month pace and greatly outpace exports over three months.

Trade by country

The trade patterns for Germany follow these same patters as for the EMU with the difference that over three months both export and import flows settle down to nearly identical and strong rates of growth.

In France, neither exports nor imports fall over 12 months; exports accelerate over six months while imports weaken and decline. Over three months, imports claw back losses to attain weak growth while exports continue to accelerate.

In the United Kingdom, like France, neither exports nor imports decline over 12 months. And both flows decelerate mildly from 12-months to six-months. Over three months, both U.K. exports and imports accelerate, but exports accelerate much faster.

Export trends for the Netherlands, Finland and Portugal show flows weak or in decline over 12 months. There are strong accelerations over six months with significant deceleration over three months yet with flows retaining strong growth in double digits. On balance, their export profile is a lot like that of the EMU overall.

Trade and the virus

Trade flows seem to be less affected by the pace of the virus spreading than other statistics. That could change in December and January when a new fast spreading strain was found in the U.K. and borders were temporarily shut. How much concerns about that fast-spreading virus affected shipments we will see in coming months. But current data trends to not reveal any tight connection with the virus spreading or slinking back into hiding.

Summing up

Still, the virus has spread- is spreading- again in December and in January; there are widespread lockdowns in Europe and especially affecting the U.K. We may over the next several months see some impact although these months were also rife with concerns about whether the U.K. and the EU would be able to strike a post-Brexit trade deal…and eventually they did. So over the next two months, there could be virus effects and other effects stemming from actions taken by firms to secure supplies in the event of a ‘no trade’ deal by the U.K. post-Brexit. Fortunately, that did not happen, but trade flows still may have been distorted. And in the wake of the trade deal that was struck trade relations still will be different from what they were and that should impact some trade flows.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief