Global| Dec 19 2017

Global| Dec 19 2017Surprising Drop in German IFO Survey- As the World Churns

Summary

According to an old expression, 'trees do not grow to the sky.' In that spirit, it can't be 'surprising' that despite strong growth and solid improving conditions in the German economy, the IFO index stepped back this month. Only [...]

According to an old expression, 'trees do not grow to the sky.' In that spirit, it can't be 'surprising' that despite strong growth and solid improving conditions in the German economy, the IFO index stepped back this month. Only diamonds are forever.

According to an old expression, 'trees do not grow to the sky.' In that spirit, it can't be 'surprising' that despite strong growth and solid improving conditions in the German economy, the IFO index stepped back this month. Only diamonds are forever.

The chart shows how the IFO expectations index and the GfK consumer sentiment survey continue to press higher. The small 'set back' in expectations this month is barely a spec in those time series of optimism.

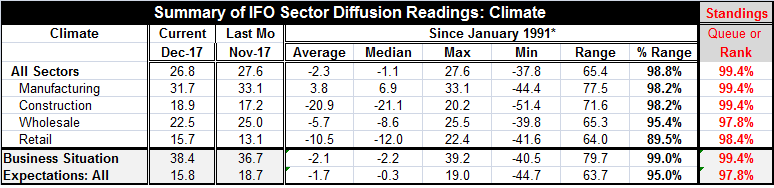

The business situation improved in December, but expectations fell on balance and the all-sector index fell month-to-month. Advancing on the month were the retail and construction sectors. Stepping back on the month were manufacturing and wholesaling. However, the right hand column of the table shows the rankings of this month's readings as percentile standings for each of these IFO metrics. Those rankings are an embarrassment of riches for the German economy. Despite this small drop off in expectations, it's hard not to be very optimistic about the German economy.

Euro area unit labor costs fall in Q3

Still, even with solid and improving growth in the EMU in Q3, euro area unit labor costs continued to soften. Hourly wage costs rose by 1.6% year-on-year, slower than a 1.8% advance in the previous quarter. Growth in the EMU is solid as inflation pressures remain at bay. It's good news for sure, but that sort of development will continue to stoke the fires of policy disagreement at the ECB where the Germans think that no matter how a fine a day it is today, it could always rain tomorrow.

Shifting forecasts

Also today, a number of countries saw their growth outlooks altered. And here we find significant adjustments in place in different directions. The big report is the World Bank's scale back for China. The World Bank sees growth strong in 2017 (fait accompli) at 6.8% (up a tick from 6.7% previously); however, looking ahead, it sees growth of 6.4% in 2018 and of 6.3% in 2019. China is slowing down. According to the World Bank, reducing fiscal and financial vulnerabilities is likely to come at the cost of slower GDP growth in the near term but will improve China's long-term economic prospects. That of course assumes that China will in fact make that switch in its priorities. China has been loath to make those sorts of changes since to it growth equals economic and political stability. China has been unwilling so far to play with that fire. Will it take that step and bear that risk in 2018?

On the plus side, Japan's government lifted its outlook substantially. The Cabinet Office now projects 1.9% for growth in fiscal 2017 and 1.8% growth in fiscal 2018; these rates are up from 1.5% and 1.4%, respectively. Japan's fiscal year ends in March so this is more than just marking numbers to reality.

Sweden lifted its outlook but cut its estimate of growth in 2017. The Swedish government sees only 2.5% growth in 2017 (3.1% previously). Its estimate for 2018 is up to 2.8% (2.5% previously) and for 2019 the estimate is 2.2% (2% previously). Sweden also hiked its inflation outlook for 2017 to 1.7% from 1.6% but cut the outlook to 1.5% in 2018 (from 1.7% previously).

The Swiss also hiked their outlook to 2.3% for 2018 from 2% previously. Growth is expected to slow again in 2019 to 1.9%. The Swiss look for more normal oil prices ahead and expect that will be consistent with inflation averaging 0.5% (no change in that outlook).

Except for China, the big enchilada, growth outlooks are being lifted. And for the most part inflation outlooks are being held in check. Inflation dynamics are simply not anticipated nor are they present in up-to-date-data despite the recent upturn in global growth. But economists' models are based on precepts that see these conditions bringing higher prices so the warnings are still being levied and policies are gingerly beginning to prepare for a future with inflation. But...what if that is wrong?

A lack of inflation but no lack of inflation fear

This recovery has been long in coming. In fact, what we have is not even impressive; it is only incipient. We have no idea how strong or durable it might be; yet, a number of central bankers in Germany and in other hard-money euro-states as well as at the Fed on the FOMC and some at the BOE want harder money polices. What do we want? Tighter policy! When do we want it? Now! Really?

The China uncertainty

The question remains of how China's slowing will occur and how much it will trump faster growth elsewhere. If China slows because it shutters its uncompetitive industries and stops dumping goods on global markets, 'China's slowing' could actually be 'inflationary.' However, it is far from clear that China will do that, or even if it does, how aggressively it might pursue such a policy. It could be one of those moderate policy shifts with little impact- if China follows its prescribed path.

From Barney World to Resident Evil!

I'm connected to you. You are connected to me! We are a connected family! It's a big interconnected world out there. German data today remind us that we can be surprised and also that not all surprises move markets. Not all surprises come in the 'direction' we most fear. By definition, a surprise is a surprise, although many people expect that the 'surprise' this year (if there is one) will come in the form of more growth and more inflation. I guess if 'they' are wrong, it will be 'quite a surprise?' Playing the surprise game can be vexing and dangerous. Convincing yourself that you know where the risk lies can create a false sense of security and breed bravado. For now global growth is on solid footing and inflation is low and stable and why policy can't stay on an even keel and be happy with that is one of the reasons that central bankers are prone to make such bad policy. I love growth. Growth doesn't love me. Inflation is low and that's an anomaly! When the times call for nothing, they are sure it's time to do something. They need to prepare for what's next even though they are incapable of that since they demonstrate time and time again their inability to anticipate future significant events be they recession, financial crisis or commodity price booms or busts. Central bankers are like the feeble hitter in baseball with a 170 (puny) batting average who finds himself at the plate with the game tied, two outs, bases loaded and 3-2 count and yet is determined to swing the bat instead of take the pitch. If central bankers were using 'sabermetrics' to conduct policy, things would be a lot quieter in the halls of the world's central banks these days. The risk that inflation is about to rise up and bite you on the bottom is still pretty small. There is little evidence of rising inflation pressures. But central bankers have dreams and models and in those models - think of them as video games for central bankers - a deadly virus has escaped and is about to infect the world and only central bankers' timely rate-hiking actions can save us. The only question is whether the resident evil will come from the central bankers themselves, bitten in their sleep, or if there is a threat in the real world. Once bitten, forever a zombie inflation-fearing central banker.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief