Global| Mar 23 2016

Global| Mar 23 2016Spanish Price Trends

Summary

Spanish price trends point lower in February. Spain's PPI prices fell year-over-year for overall producer prices led by a drop in intermediate goods prices. Consumer goods barely ticked higher over 12 months (0.2%) while investment [...]

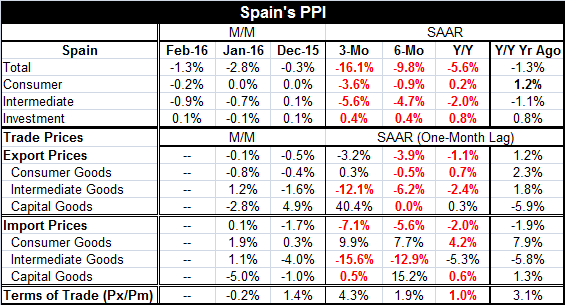

Spanish price trends point lower in February. Spain's PPI prices fell year-over-year for overall producer prices led by a drop in intermediate goods prices. Consumer goods barely ticked higher over 12 months (0.2%) while investment goods prices rose by 0.8%. However, the progressive behavior of prices over shorter periods shows that all price trends weaken over shorter horizons. Overall PPI, consumer goods and intermediate goods prices are falling over three months and investment goods marking an annualized rate of increase of just 0.4%. The monthly data confirm these trends with price drops becoming more common in February than in January and in January vs. December by industry group. Intermediate goods price weakness leads the sectors lower with oil and commodities prices as the main drivers there.

Spanish price trends point lower in February. Spain's PPI prices fell year-over-year for overall producer prices led by a drop in intermediate goods prices. Consumer goods barely ticked higher over 12 months (0.2%) while investment goods prices rose by 0.8%. However, the progressive behavior of prices over shorter periods shows that all price trends weaken over shorter horizons. Overall PPI, consumer goods and intermediate goods prices are falling over three months and investment goods marking an annualized rate of increase of just 0.4%. The monthly data confirm these trends with price drops becoming more common in February than in January and in January vs. December by industry group. Intermediate goods price weakness leads the sectors lower with oil and commodities prices as the main drivers there.

In Spain, the headline and intermediate prices are lower year-over-year as well as for year-over-year one year ago and two years ago. There is a deep legacy of price declines that could affect expectations in Spain and make it harder for the ECB to turn things around. Spain is not alone in the EMU in suffering through such prices weakness. The political party, Podemos, has been gaining popularity and wants to take Spain off the existing austerity program that is contributing to ongoing price declines in Spain and limiting the use of fiscal policy (preventing it). Deflation has been in train for so long; it is creating a backlash. And that is one of the problems with such strident use of austerity. It only works when it is in place. Yet, its use can create a powerful backlash. And if austerity is dismantled, usually that is done with an aggressive overthrow of its application and results in a complete undoing of the progress made while it was in effect, rendering the past sacrifice worthless. German-style austerity is a high-risk approach to restore fiscal balance and price stability. We see all these forces in play in Spain.

And we can see that much of Spain's price weakness is homegrown. We present export and import prices which show for both year-on-year price declines by split export and import results for year-ago prices. Domestic prices have been more persistently weak than have been export and import prices. Spanish export prices have been stronger than the PPI in recent years and stronger than import prices leading to a rise in the terms of trade. Competitiveness has been maintained by a weakening exchange rate. That has been an aid to Spain's ability to earn foreign exchange and in the trade of goods. A rising terms of trade ratio means that a nation is being paid more for its exports than it has been paying for its imports compared to the past. That helps to boost its welfare.

Still, Spain has been under enormous political pressures although real retail spending has been on the mend and Spanish GDP has been posting consistent gains. Despite its successes, Spain is still a country beset with political tensions amid ongoing economic progress and slow-mending high unemployment. The ECB's inability to get enough growth in gear using tradition then unconventional monetary tools has been disappointing. Monetary policy is at a near standstill in combating the depressing effect of austerity. Inflation is under control or too weak. Growth has been put in gear more readily than has unemployment reduction and those facts remain a sticking point in Spain.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief