Global| Jul 17 2015

Global| Jul 17 2015Spain Shows Some Strength in Its Volatile New Orders

Summary

Spanish orders and shipments (turnover) show some strength in May, but sequential growth rates for both show some evidence of slowing. Orders popped in May, surging by 3.3% in one month. This was the strongest monthly gain since [...]

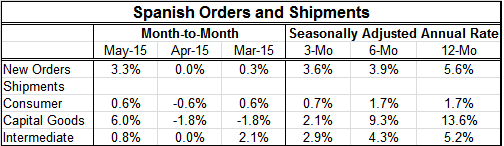

Spanish orders and shipments (turnover) show some strength in May, but sequential growth rates for both show some evidence of slowing.

Spanish orders and shipments (turnover) show some strength in May, but sequential growth rates for both show some evidence of slowing.

Orders popped in May, surging by 3.3% in one month. This was the strongest monthly gain since December. The gain, however, is not necessarily encouraging. In Spain, outsized increases in new orders usually are preceded or followed by large drops. This fact makes us wary of thinking that the spurt in sales in May is real. Since the May spurt is largely responsible for holding three-month growth rates up, we should be skeptical of that as well. However, the good news is that if we look at the gains before and after there are large spikes in orders that three-month cluster of data historically usually leaves a net gain on the books. While the message in May may not be that sales are spurting, it is probably true that they are still advancing. However, when the dust settles, they may still be decelerating.

Monthly shipments are also volatile but about 20% less volatile monthly than orders but only about 10% less volatile on year-over-year growth. They also show growth in May but prevaricate over longer periods.

Shipments show a pick-up in May for all three major categories led by a surge in capital good shipments. However, the sequential growth rate for each shipment category shows a slowdown from 12-month to six-month, and again from six-month to three-month. This echoes the slowdown in overall order trends.

The spike in orders in May belies this slowing trend for orders and shipments. Spanish data are hard to dissect because of this variability. While there is a longing to find some growth acceleration in the euro area, data for Spain just do not seem to be on board with that trend. In addition, there is the issue of Spain as an austerity country. Its Podemos party is trying to undo Spain's commitment to that program.

This is one of the reasons that the EU Commission took such a hard line with Greece. Greece was in the negotiations for itself while the EU Commission was always aware that was in a spotlight and being watched by other austerity countries and setting a precedent for them. The hard line with Greece was at least demonstration to these other countries of what the road would be like if any of them tried to untrack austerity. For that reason, Spain is likely to stay on its austerity path. Podemos may continue to make noise and have its adherents, but the path of austerity would seem likely to remain the overwhelming choice of Spain's policymakers.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief