Global| Apr 21 2005

Global| Apr 21 2005Sharp Slowdown in UK Retail Trade for Early 2005

Summary

Retail sales in the UK are flagging, according to the most recent couple of months' data from the Office of National Statistics. In March, sales values rose 0.2% from February, the same size gain as for February from January. These [...]

Retail sales in the UK are flagging, according to the most recent couple of months' data from the Office of National Statistics. In March, sales values rose 0.2% from February, the same size gain as for February from January. These moves yielded a 3.0% increase from March 2004, compared with a 4.7% increase for all of 2004.

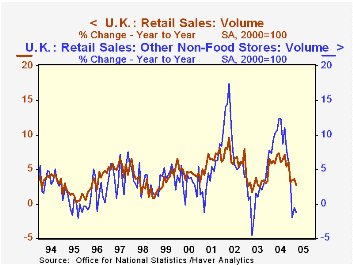

The swing was wider in the corresponding volume results, that is, adjusted for inflation. Sales fell in March by 0.1% and were 3.7% ahead of a year ago. But 2004 as a whole saw 6.0% growth from 2003, making the recent performance a moderation of 2.3 percentage points. By store category, the weakening occurred in nonfood store sales and non-store sales and repair. (Internet sales by retailers having stores are included in the sales of the relevant store group.) Household goods and "other" nonfood stores experienced the greatest degree of slowing.

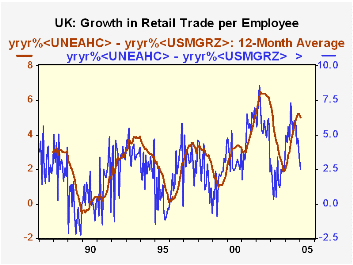

It might be argued that weakening retail sales growth would result from weakening employment. However, employment growth in the UK hasn't changed much in recent months. The 0.8% in the January figure (3-month average, here representing December, January and February) is very much in line with the pace prevailing during most of last year. Thus, the smaller gains in retail trade are resulting from more sluggish spending by individual employees, not fewer employees. See the second graph, which shows a progressive deceleration in sales/employee. We can surmise that this might arise from rising energy costs, which would be absorbing more consumer income. Indeed, detailed National Accounts data through Q4 2004 indicate major increases in the costs of household utilities and vehicle fuels. GDP totals for Q1 will be reported tomorrow, 22 April. But the breakdown of expenditure detail won't be available until the June release of the national accounts. So for the present, our supposition about the role of energy must remain conditional. Then again, the recent slower pattern of retail trade may only be a reaction to more rapid expansion during 2004.

| % Changes | Mar 2005 | Feb 2005 | Jan 2005 | Year Ago | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| Total Value | 0.2 | 0.2 | 0.8 | 3.0 | 4.7 | 2.0 | 5.3 |

| Total Volume | -0.1 | 0.3 | 0.6 | 3.7 | 6.0 | 2.9 | 6.5 |

| Mostly Food | 0.0 | -0.3 | 1.9 | 4.5 | 4.1 | 3.3 | 4.1 |

| Mostly Non- Food Stores | 0.2 | 0.5 | -0.1 | 3.3 | 7.2 | 3.5 | 8.4 |

| Non-Stores | -3.8 | 3.5 | -0.2 | 2.5 | 9.4 | -5.0 | 7.2 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief