Global| Jun 21 2017

Global| Jun 21 2017Sharp Rise in Japan's Sector Indices is Led by Construction

Summary

Japan's sector indices from METI show gains across the board led by a huge rise in Construction. The construction index jumped by 8.1 points in April the largest month-to-month gain in the history of the series that goes back to early [...]

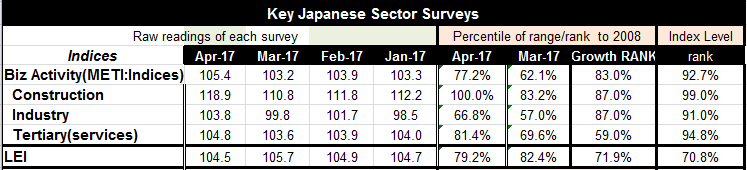

Japan's sector indices from METI show gains across the board led by a huge rise in Construction. The construction index jumped by 8.1 points in April the largest month-to-month gain in the history of the series that goes back to early 2008. It also marks the 13th largest year on year gain by the sector index. The construction index only carries a 5.77% weight in the overall index with the tertiary index (services) accounting for most on the weight (73.45%) and the industrial sector accounting for the remaining 20.78% of the weight. Still, the construction sector gain alone is enough this month to add one half of one point to the monthly headline series which rose to 105.4 in April from 103.2 in March.

Japan's sector indices from METI show gains across the board led by a huge rise in Construction. The construction index jumped by 8.1 points in April the largest month-to-month gain in the history of the series that goes back to early 2008. It also marks the 13th largest year on year gain by the sector index. The construction index only carries a 5.77% weight in the overall index with the tertiary index (services) accounting for most on the weight (73.45%) and the industrial sector accounting for the remaining 20.78% of the weight. Still, the construction sector gain alone is enough this month to add one half of one point to the monthly headline series which rose to 105.4 in April from 103.2 in March.

Over time these indices tend to growth so in the table as a reference I offer rankings of the April values of the METI headline and component pieces on 12-month growth rate basis as well as on the level of index and its respective components.

The headline index level is this high or higher less than 8% of the time. With the huge jump in the construction index it is this high or higher only about 1% of the time; that standing marks this as an all-time (back to 2008) high reading for construction. The industry gauge is this high or higher about 9% of the time on this time line. The tertiary index is this high or higher less than 6% of the time. And the leading index level is this high or higher less than 30% of the time. In terms of level standings the industrial and tertiary indices are strong and the construction sector index has never been stronger. These standings suggest that Japan is making some progress on economic revival.

Evaluated in terms of year-over-year growth, a standing that will give us a better idea of how these indices might be contributing to national growth, not surprisingly, we find a slightly different array of rankings for growth rates than for index levels. The overall business activity index ranks in its top 17 percentile on a growth basis. That is a solid and strong reading, but not eye-popping. Construction has an 87th percentile growth ranking (or top 13%) a reading that has come out of nowhere this month thanks to its strong month-to-month jump. The industry growth rate also has an 87th percentile ranking. But the service sector has only a 59th percentile standing (top 41%). This tells us that the service sector is lagging in relative terms. And, of course, it carries the largest weighting of all sectors. Still, in growth terms the headline and various METI sector indices all (except for services) have a higher growth standing that for the LEI which is an economy-wide gauge. Its 71 percentile growth ranking is solid but not particularly strong.

These evaluations are for the period when a full array of sector indices is available, since January of 2008. That, of course, is not a period of very robust growth for Japan or for the global economy. Still, a Cabinet Office panel of experts recently confirmed that Japan's current economic expansion continued for a 53rd consecutive month in April, making it the third-longest expansion in the postwar period. So having solid, firm or even somewhat strong readings on the levels of the indices on this time line is not necessarily impressive. In fact at this point in such an expansion we should expect that the headline and various sector indices are all very near if not at their peaks in terms of level standings. These data suggest that Japanese economy is making progress but it is not surging ahead except for construction which really has jumped over some hurdles to score a very strong reading this month. Japan's economy continues to make progress. Apparently the government is getting ready to upgrade the economy's performance, a good sign. The industrial sector coupled with recent strong gains form construction are the driving forces in this economy as the service sector has lagged behind.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief