Global| Oct 18 2005

Global| Oct 18 2005September PPI Up 1.9%: Spillover Effects?

by:Tom Moeller

|in:Economy in Brief

Summary

The overall Producer Price Index jumped 1.9% last month, easily surpassing Consensus expectations for a 1.1% increase. The gain was the largest since January 1990 and was led by a 7.1% leap in energy prices which also was the [...]

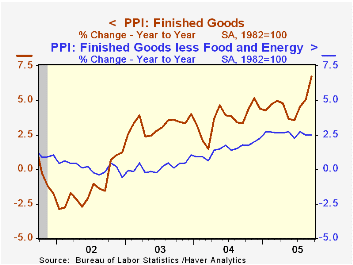

The overall Producer Price Index jumped 1.9% last month, easily surpassing Consensus expectations for a 1.1% increase. The gain was the largest since January 1990 and was led by a 7.1% leap in energy prices which also was the strongest since 1990.

The so called "core" PPI index is focused on since it provides an indication of the degree to which pressures on energy or food prices may be "spilling over." Finished goods prices less food & energy increased 0.3% in September. The rise beat Consensus expectations for a 0.2% increase and followed no change in prices during the previous month.

And these spillover effects may indeed be now more apparent than earlier for several reasons. 1) The y/y change in core prices held at 2.5%, up from 0.1% and 0.2% during 2002 and 2003, respectively. 2) Prices for core consumer goods rose 0.2% and the y/y gain held at 2.6% versus a 0.1% increase in 2003. 3) Capital equipment prices rose 0.3%. The y/y gain rose to 2.3% from -0.4% during 2002 despite a 22.1% y/y decline in computer prices. That drop was comparable to the 22% and 25% price declines during 2001 and 2002.

Consumer durable goods prices rose 0.4% (+1.5% y/y) led by increases in floor coverings (7.5% y/y), household furniture (3.6% y/y) and jewelry (3.8% y/y). Core consumer nondurable goods prices rose 0.2% (3.6% y/y).

Gasoline prices jumped 12.8% (63.6% y/y) while fuel oil prices surged 11.3% (57.1% y/y). Natural gas prices also posted a strong 8.1% (24.7% y/y) increase and in October the spot gas price has pushed nearly to $14.00/mmbtu, more than double the year ago level.

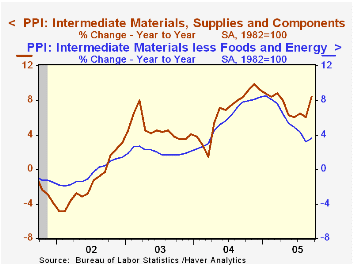

Intermediate goods prices surged 2.5%, the strongest monthly increase since 1980 while core intermediate goods prices rose 1.2%, the strongest gain since April of last year.

A 16.9% (64.4% y/y) spike in crude energy prices lifted overall crude goods prices by 10.2%.and that pulled the y/y gain to its highest since early 2003. Core crude prices jumped for the third straight month. During the last thirty years "core" crude prices have been a fair indicator of industrial sector activity with a 48% correlation between the six month change in core crude prices and the change in factory sector industrial production.

Federal Reserve Board Chairman Alan Greenspan's speech on Energy is available here.

Inflation Expectations: How The Market Speaks from the Federal Reserve Bank of San Francisco can be found here.

| Producer Price Index | Sept | Aug | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Finished Goods | 1.9% | 0.6% | 6.7% | 3.6% | 3.2% | -1.3% |

| Core | 0.3% | 0.0% | 2.5% | 1.5% | 0.2% | 0.1% |

| Intermediate Goods | 2.5% | 0.7% | 8.4% | 6.6% | 4.6% | -1.5% |

| Core | 1.2% | -0.1% | 3.5% | 5.7% | 2.0% | -0.5% |

| Crude Goods | 10.2% | 2.3% | 28.5% | 17.5% | 25.1% | -10.6% |

| Core | 5.3% | 4.6% | 6.5% | 26.6% | 12.4% | 3.8% |

by Tom Moeller October 18, 2005

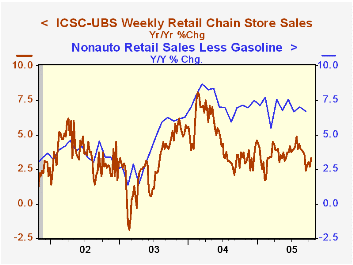

Chain store sales rose for the fourth consecutive week. Last week's 0.4% increase, according to the International Council of Shopping Centers (ICSC)-UBS survey, lifted sales 1.3% above the mid-September low.

During the last ten years there has been a 56% correlation between the y/y change in chain store sales and the change in non-auto retail sales less gasoline, as published by the US Census Department. Chain store sales correspond directly with roughly 14% of non-auto retail sales less gasoline. The leading indicator of chain store sales from ICSC squeaked out a 0.1% (-2.5% y/y) increase.The ICSC-UBS retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

| ICSC-UBS (SA, 1977=100) | 10/15/05 | 10/08/05 | Y/Y | 2004 | 2003 |

|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 450.6 | 448.9 | 3.3% | 4.6% | 2.9% |

by Louise Curley October 18, 2005

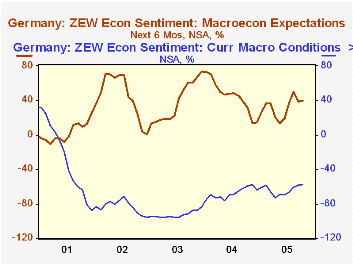

The results of Germany's latest ZEW survey, released today, were below consensus, showing only a slight improvement in October in the balances between optimists and pessimists among German institutional investors and analysts regarding current economic conditions and those expected six months ahead. The disappointing results of the survey may be due, in part, to the uncertainty arising out of the inconclusive election held last month. A coalition government between the CDU/CSU (Christian Democratic Union, and Christian Social Union), with their narrow victory of four seats, and the SPD (Social Democratic Party) has been agreed upon with Angela Merkel as Chancellor.However, the process of selecting a cabinet, now underway is revealing what may be potentially serious differences among the possible candidates. The process is not expected to be over much before November 17 when the Bundestag formally installs the new Chancellor and pronounces the new government operational.

Pessimists continue to outweigh optimists in their appraisal of current conditions. The balance between those expecting current conditions to improve and those who expect them to worsen rose a mere one-tenth of one percent from -58.1% to 58.0%. When they look ahead, the respondents to the survey are more optimistic. The balance between those expecting better conditions six months ahead and those expecting worse conditions rose by 0.8% in October to 39.4% from 38.6% in September. The contrast between the respondents' appraisal of current conditions and their appraisal of expectations six months ahead is shown in the first chart.

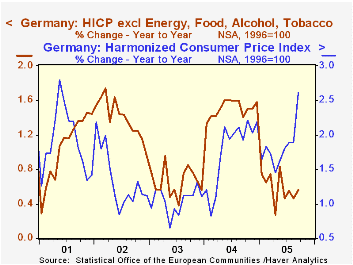

Inflation is another factor that may be influencing sentiment among institutional investors and analysts.Eurostat published today the Harmonized Consumer Prices Index for the Euro Zone and the individual countries of the area. In addition, indexes of core inflation, defined as the total index excluding, energy, food, alcohol and tobacco, are also published. For Germany, the year to year increase in the total index was 2.61%, up from 1.89% in both August and July. Although core inflation also rose, it remains at low levels, lower than in some of the earlier months of the year. Core inflation was 0.56% in September, compared with 0.46% in August and 055% in July. The Harmonized Consumer Price index and its related Core Inflation index are shown in the second chart.

| Percent Balance of Opinion German ZEW Survey | Oct 05 | Set 05 | Aug 04 | M/M Dif | Y/Y Dif | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|---|

| Current Conditions | -58.0 | -58.1 | -58.9 | 0.1 | 0.9 | -67.7 | -92.6 | -83.3 |

| Expectations 6-months ahead | 39.4 | 38.6 | 31.3 | 0.8 | 8.1 | 44.6 | 38.4 | 45.3 |

| German Harmonized Consumer Price Index | Y/Y % | Y/Y % | Y/Y % | Y/Y % | Y/Y % | Y/Y % | Y/Y % | Y/Y % |

| Sep 05 | Aug 05 | July 05 | Jun 05 | May 05 | Apr 05 | Mar05 | Feb 05 | |

| Harmonized CPI total | 2.61 | 1.89 | 1.89 | 1.81 | 1.63 | 1.45 | 1.72 | 1.82 |

| Harmonized CPI core | 0.56 | 0.46 | 0.55 | 0.46 | 0.84 | 0.28 | 0.74 | 0.65 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief