Global| Dec 03 2015

Global| Dec 03 2015Retail Sales Show Their Weak Side; ECB Offers More Stimulus

Summary

Note that the graph presented here is a two-scale plot on the level of vehicle registrations and the level of the retail sale volume index. Both retail sales and motor vehicle registrations are well off peak. MV registrations are back [...]

Note that the graph presented here is a two-scale plot on the level of vehicle registrations and the level of the retail sale volume index. Both retail sales and motor vehicle registrations are well off peak. MV registrations are back to about late 2008 levels, but retailing is back only to about 2011 levels of sales. Moreover, both MV registrations and retail volumes show a multi-month period of flatness.

Note that the graph presented here is a two-scale plot on the level of vehicle registrations and the level of the retail sale volume index. Both retail sales and motor vehicle registrations are well off peak. MV registrations are back to about late 2008 levels, but retailing is back only to about 2011 levels of sales. Moreover, both MV registrations and retail volumes show a multi-month period of flatness.

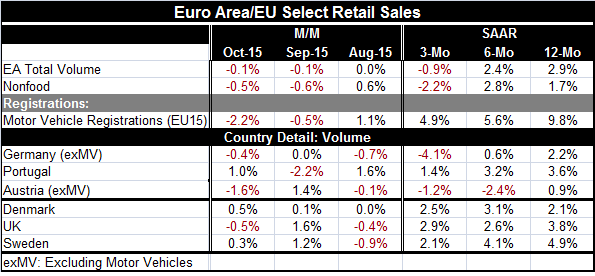

We can inspect the recent weakness using the calculations in the table that look at recent percentage changes. Year-over-year both MV registrations and retail volumes are moving higher. And both are higher on balance over six months. But over three months both MV registrations and retail volumes are shrinking. In fact, both MV registration and retail volumes show a steady deceleration in sales from 12 months to six months to three months. These patterns are not reassuring.

On a country level, we have a batch of early reporters including three EMU members and three non-EMU members. Sweden has the strongest retail volumes with gains of 4.9% over 12 months. Austria has the weakest gains with a rise of just 0.9% over 12 months. Only Denmark has a three-month growth rate in excess of its 12-month growth rate. And only Germany and Austria have sales falling over three months.

The picture for retail sales is not good and is not particularly encouraging because of the fading momentum.

However, the ECB rolled out its stimulus package for December today and it's announced a cut in deposit rates and greater security purchases of a broader array of assets. The program is to be in place until March 2017. ECB President Mario Draghi cited the expansion of the existing QE program because it had been so successful so far.

However, the ECB rolled out its stimulus package for December today and it's announced a cut in deposit rates and greater security purchases of a broader array of assets. The program is to be in place until March 2017. ECB President Mario Draghi cited the expansion of the existing QE program because it had been so successful so far.

Underpinning Draghi's claim we see that both money and credit growth have picked up since the ECB QE program was started. Private sector loans are showing positive growth after a pronounced period of contracting. Of course, a weaker euro has also been the result of this policy although there is little showing for it in terms of stronger export growth since globally demand has been so weak. The euro is likely to be helped lower by the Fed's clear steps to hike rates even as economic data in the U.S. have deteriorated around it. The combination of more ECB easing and Fed tightening should propel the dollar higher and the euro lower.

It is still hard to say how effective more QE will be. The experiences in the U.K. and the U.S. showed that aggressive early application of QE was associated with the best results. Later additions to the program did not always seem to help as much. With interest rates already so low in the EMU area, there is less scope for QE to move rates lower. The shallowness of Europe's securities markets has also hampered the ECB in getting the stimulus in place that it has wanted. The ECB has now broadened the rules for collateral acquisition to help get around this problem. As in all securities offerings we should remember that past results are not an indicator of future performance. That goes double for added rounds of QE purchases. Nevertheless, for now, optimism runs high.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief