Global| Jul 30 2008

Global| Jul 30 2008Rapid Fall Off in EU Indices - Especially for Services

Summary

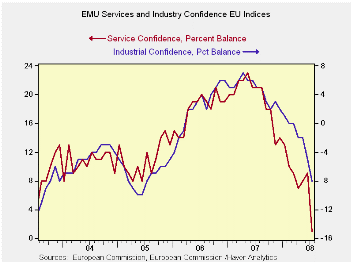

The picture on top captures the path of the industrial sector and the services sector in EMU. Both have turned sharply lower by mid 2008 after having peaked about one year ago. The overall EMU sentiment index is now in the 36th [...]

The picture on top captures the path of the industrial sector and the services sector in EMU. Both have turned sharply lower by mid 2008 after having peaked about one year ago. The overall EMU sentiment index is now in the 36th percentile of its range nearly at the border of the bottom third of its range, a weak enough position that makes it reasonable to talk of downside risks and even recession potential. The two weakest sectors/areas by their percentile standings are services (15th percentile) and Consumer confidence (24th percentile). The industrial and construction sectors are the relative strongest with standings at about the mid 50s percent of their respective ranges.

In July all sectors fell and most fell sharply. Services with a seven point fall and retailing with a six point fall made the largest drops in the month.

The largest EMU and EU countries saw their overall sentiment gauges fall in the month with only the smallest of the large countries (Spain) showing month-to-month improvement. In the case of Spain, however, the ‘bounce’ is a bit of a ‘dead cat bounce’ since among these large European economies Spain’s has the lowest percentile standing for its overall sentiment reading which stands at a very lowly 14 percent. At 26 percent the UK is the next lowest and at 27 percent Italy is the third lowest. France is the relative strongest at a percentile reading of 46, followed by Germany at 44 percent. The EMU relative reading at 37.4 percent is just slightly above the EU reading which is 36.0 percent.

We focus on these percent percentile readings since each industry and country has its own range and dynamic in terms of these net balance readings. By drawing attention to the percentile position of a reading in a range of the EU net balance outcomes we can compare across industries and countries with greater confidence that we are comparing apples with apples or oranges with oranges.

By comparison, look at the raw net balance readings. In July all the sector net balance readings are negative except services, which is at zero. But at zero services is relatively weaker in its range than are the other sector readings (compare their percentiles!). In perusing the data you might be tempted to see services as the strong sector since it is zero while the others are negative. But the fact is that the services gauge is simply less prone to fall into negative territory and at zero it is signaling greater sector weakness in services than a -20 reading would be signaling for consumer confidence.

These EC Commission surveys are very comprehensive, covering the various EU/EMU member countries and all the relevant sectors by country. A full perusal of this month’s data reveals a very weak Europe and one that is in the process of weakening sharply as well. At the same time the topical inflation report for Germany suggests that headline inflation is still pushing higher, something that will keep the ECB back on its heels.

We continue to see the GLOBAL slowdown as a reaction to the rise in commodity prices – especially oil - a gain that has taken a toll on all the major consuming nations. The US slowdown, the global financial tangle and the rise in oil prices are hitting the world economies at the same time. It is no wonder that the global business cycle is back in sync…or should I say sink?

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Jul 08 |

Jun 08 |

May 08 |

Apr 08 |

%tile | Rank | Max | Min | Range | Mean | R-SQ w/Overall |

| Overall | 88.7 | 94.5 | 97.1 | 98 | 36.0 | 225 | 116 | 73 | 43 | 101 | 1.00 |

| Industrial | -8 | -4 | -3 | -2 | 55.9 | 144 | 7 | -27 | 34 | -6 | 0.87 |

| Consumer Confidence | -20 | -17 | -14 | -12 | 24.1 | 227 | 2 | -27 | 29 | -10 | 0.83 |

| Retail | -11 | -5 | -3 | -6 | 37.0 | 212 | 6 | -21 | 27 | -5 | 0.48 |

| Construction | -17 | -14 | -11 | -11 | 53.2 | 154 | 5 | -42 | 47 | -15 | 0.42 |

| Services | 0 | 7 | 6 | 6 | 15.8 | 129 | 32 | -6 | 38 | 17 | 0.79 |

| % m/m | Jul 08 |

Based on Level | Level | ||||||||

| EMU | -5.6% | -2.9% | 0.5% | 89.5 | 37.4 | 222 | 117 | 73 | 44 | 101 | 0.93 |

| Germany | -4.1% | -1.5% | 0.2% | 97.3 | 44.1 | 158 | 121 | 79 | 42 | 101 | 0.64 |

| France | -4.8% | -3.0% | -1.8% | 93.5 | 46.6 | 188 | 119 | 72 | 47 | 101 | 0.81 |

| Italy | -10.1% | -0.1% | 3.3% | 85.4 | 27.6 | 230 | 122 | 71 | 51 | 101 | 0.80 |

| Spain | 1.6% | -7.8% | -0.4% | 74.2 | 14.6 | 238 | 118 | 67 | 51 | 100 | 0.60 |

| Memo:UK | -7.8% | 2.3% | -5.4% | 85.5 | 26.5 | 229 | 132 | 69 | 64 | 102 | 0.41 |

| Since 1990 except Services (Oct 1996): 247 | -Count | Services: | 142 | -Count | |||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief