Global| Jun 22 2017

Global| Jun 22 2017Pull Back in French Total Business Climate

Summary

Climate backs off in month as year-on-year gains continue their small pick up The French industrial climate gauge backtracked slightly to 108.4 in June from 108.8 in May. The rank or queue standing of the index falls into its 78th [...]

The French Service Sector Flashes Some Warning Signs

Climate backs off in month as year-on-year gains continue their small pick up

The French industrial climate gauge backtracked slightly to 108.4 in June from 108.8 in May. The rank or queue standing of the index falls into its 78th percentile, a moderately firm reading. The rank standing places the month's number in a queue of values since February of 1990 while the "range standing" positions the monthly reading in the high-low range for the period. The queue standing provides more information about the relative strength of the reading as it uses information from all prior readings. A 78th percentile standing is solid.

The French industrial climate gauge backtracked slightly to 108.4 in June from 108.8 in May. The rank or queue standing of the index falls into its 78th percentile, a moderately firm reading. The rank standing places the month's number in a queue of values since February of 1990 while the "range standing" positions the monthly reading in the high-low range for the period. The queue standing provides more information about the relative strength of the reading as it uses information from all prior readings. A 78th percentile standing is solid.

Mixed trend view

The recent trend for production, a backward-looking gauge, rises sharply in June to 17 from 7 in May this boosts the reading to the 86th percentile of its historic queue of data. However, the likely trend, a gauge that looks forward more than backward, saw slippage to 13 from 16 and has a queue standing at its 75th percentile, a positive reading but one that is more modest.

Orders and demand are solid

Orders and demand saw an improvement in June to -3 from -5. Despite an overall raw-score negative reading that measure has an 82nd percentile standing (it is this high or higher only 18% of the time). Foreign orders and demand saw a raw score minus-two reading that has been in place for three-months running. That reading has a similar though slightly weaker 78th percentile queue standing.

Prices still modest

As for prices, the likely sales price trend is evaluated weaker this month at a +6 reading down from +7 in May but still above the April-March reading of earlier this year. Clearly inflation expectations have firmed but are not off to the races. This gauge has a 71 percentile standing a relatively modest standing and the most modest among other gauges in the table. The fears of deflation are in the past and prices may be looked upon as firmer but by no means are they expected to be "strong."

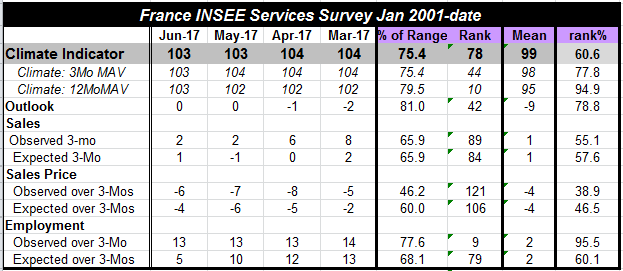

The French service sector is more modest than for industry with its overall climate indicator flat on the month but below its March-April level. The rank percentile standing (far right column in the table) is only at its 60th percentile, illustrating a much weaker service sector standing than for industry. The 12-Mo climate gauge has a 94 percentile ranking and the 3-mo gauge has a 77th percentile standing illustrating that France has come through a period of some pick up which has since lost momentum.

There is clear deterioration is the rank standings of climate from 12-Mo to 3-Mo this month (from 94.9 to 77.8 to 60.6, respectively).

Outlook

Still, the outlook has improved slightly over the last few months with the gauge now flat for two months running at a standing in its 78th percentile.

Observed and expected trends

There is not much difference in the ranking for the observed 3-Mo trend in sales and the expected trend over the next three-months. The observed trend has a 55 percentile standing, while the expected trend has a 57 percentile standing. The pattern for the raw diffusion reading on observed sales is like that for climate over all as it shows deterioration in recent months compared to March and April. Expectations show some variation but little trend.

Sales prices

Sales pries show some improved firmness month to month as each has ticked slight higher (to a smaller negative reading). Both the "expected" and "observed" readings this month are stronger than their (respective) April readings and weaker than their (respective) March readings. But the momentum is small. Observed prices show a weak 38th percentile queue standing while expected prices show a bit more firmness with a 46 percentile standing. Both standings are below the key 50% mark and therefore are below their respective medians.

Dark clouds... no silver linings

The employment gauge is perhaps the most worrisome aspect of these reports. The service sector, of course, is the key employment sector for the economy. The past "observed trend" is flat this month at a +13 reading that is more or less in step with recent months. It has a strong 95 percentile standing indicating that it is this high or higher less than 5% of the time. That's impressive. However, the expected 3-Mo reading fell to +5 in June from +10 in May and has been slipping since March. The rank standing of the expected employment metric is only in its 60th percentile. It is the weakest raw diffusion reading since June of last year. Since December 2000 a period of 199 months this is the 15th sharpest decline in the expected employment gauge month-to-month for the French service sector. Obviously that is a big deal. The indicator drops this much or more only about 7.5% of the time marking this as a potentially significant event.

Summing up... "wanna be" optimism isn't the same as real optimism

Today the ECB made a declaration about the health and likely sustainability of the EMU economy. The EMU economy is improving and various forecasts for key EMU members have been lifted this year. However, the forecast lifting has been modest. There is an air of "wanna-be-optimistic" that is not quite the same as really optimistic. I think that stems from the many disappointments from various economies in this business cycle. And while the French industrial survey is still quite solid, the assessment for the services sector is much more problematic. Maybe France is not as far out of the woods as it thought? This will be something to keep an eye on.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief