Global| Feb 18 2016

Global| Feb 18 2016Prices Sag in Euro Area As OECD Turns Up Heat for Action

Summary

The price level in the euro area dropped again in January as core prices ticked higher. But even core inflation is only at 1% and has virtually no momentum. Headline inflation, the only inflation rate truly `targeted' by the ECB, is [...]

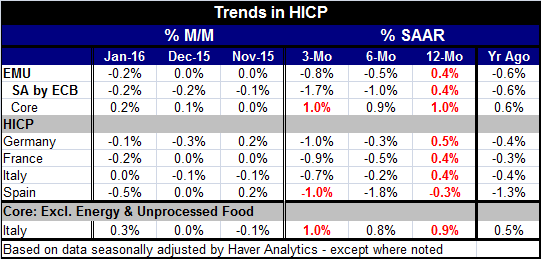

The price level in the euro area dropped again in January as core prices ticked higher. But even core inflation is only at 1% and has virtually no momentum. Headline inflation, the only inflation rate truly `targeted' by the ECB, is at a -0.8% pace over three months, falling faster than its -0.5% pace over six months which compares to a 0.4% gain year-over-year. Inflation momentum clearly is cumulating in even weaker price pressures.

The price level in the euro area dropped again in January as core prices ticked higher. But even core inflation is only at 1% and has virtually no momentum. Headline inflation, the only inflation rate truly `targeted' by the ECB, is at a -0.8% pace over three months, falling faster than its -0.5% pace over six months which compares to a 0.4% gain year-over-year. Inflation momentum clearly is cumulating in even weaker price pressures.

Today the OECD cut its forecast for growth in 2016 by 10% to 3% from 3.3% and issued a call to action to combat slowing growth and financial instability. Its previously released leading indicators had been showing some slow erosion, but the OECD until now had been content with the view that the conditions broadly were stable. Now it no longer sees things that way and it is urging members to take action.

In a statement today, the ECB noted that its modest recovery was progressing but it pointed to risks that were on the rise. It mentioned that low energy prices could feed through into other prices. If that happened, it would move the ECB even farther away for reaching its goal of just under 2% inflation, a goal it has been undershooting for 35 consecutive months with no sign that its target is in sight. That is nearly exactly three years of unrelenting misses on the downside with more to come.

Enforcement of the Maastricht fiscal rules in the EMU has been holding back Europe and has kept there from being any fiscal response since the financial crisis hit. As a result, an inordinate burden has been placed on euro area monetary policy which, of course, is not only not suited for the job it is not tailored for it. The ECB's ONLY mandate is to keep to its inflation target as it carries no direct responsibility for growth. Yet, the euro area has woefully missed and continues to miss its inflation objectives while the Bundesbank has done all it can to slowdown any extra effort while it has tried to keep the ECB on the straight and narrow relative to its charter. In retrospect, this opposition, which has required hearings and formal approvals at various stages, has slowed the implementation of stimulus and helped to undermine its effectiveness as well as to increase its ultimate costliness. The severe undershoots of its inflation target show that the need for the ECB to do more by whatever means to reach its mandated price objective have been manifest and that opposition to these moves ultimately has undermined ECB credibility.

The urging today by the OECD finds the ECB still ready to more in March. But the OECD is looking for immediate action. Fiscal policy is probably still out of the question in the EMU. Japan already has moved to a policy of negative interest rates. Japan's move seems initially to have backfired as the yen rose in the wake of the adoption of negative rates. The U.K. has gone to a neutral policy with no longer any expectation of when rates might rise; the lone U.K. policy dissent favoring a tighter policy is gone. But none of that is really new stimulus, is it? Only in the U.S. is policy not clearly stated. The Fed last went on a mission to hike rates and laid out expectations of about four rate hikes underlining it with statements from the Vice Chairman early in the year. At that time, he warned markets that they were not pricing in enough Fed tightening. The subsequent financial market meltdown was in train as Fed Chair Janet Yellen was testifying on monetary policy; neither the Fed in its February meeting nor Yellen in her testimonies gave any signal that the Fed was yet off its tightening path.

The OECD seeks to put more stimulus in play. Inflation is still too low in the EMU, Japan, the U.K. and the U.S. But policy has been ineffective in all these places and has been unable to raise inflation. The weakness in prices early in 2016 has doubled the bet that inflation would continue to undershoot longer than previously was expected. Policy moves to resist that undershoot continue to be underwhelming despite a legacy of target-missing. Central banks are still reluctant to really try to get out in front and take aggressive actions to hike prices and are too quick to step back when some smoke appears. If they were cave men trying to start a fire with flint, they would never get one going.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief