Global| May 03 2016

Global| May 03 2016PPI Drops Abate in March But Continue to Decelerate from 6-Mo to 3-Mo

Summary

The euro area PPI excluding construction rose by 0.1% in March but its progression from 12-month to six-month to three-month continues to show increasingly rapid deceleration. With a rise in prices in March, that decelerating trend is [...]

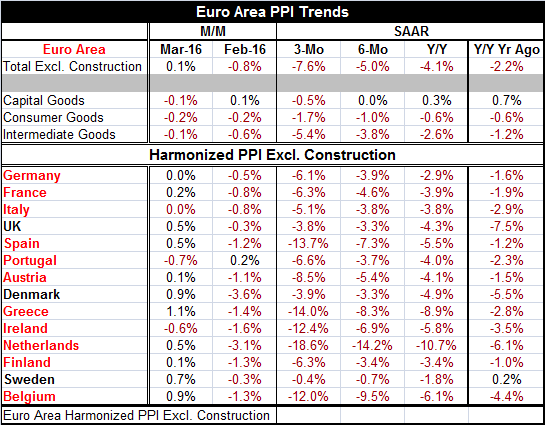

The euro area PPI excluding construction rose by 0.1% in March but its progression from 12-month to six-month to three-month continues to show increasingly rapid deceleration. With a rise in prices in March, that decelerating trend is going to come to an end in a month or so unless prices execute a reversal.

The euro area PPI excluding construction rose by 0.1% in March but its progression from 12-month to six-month to three-month continues to show increasingly rapid deceleration. With a rise in prices in March, that decelerating trend is going to come to an end in a month or so unless prices execute a reversal.

A slowdown for price drops in March but still plenty of weakness

For now, both the harmonized index of consumer prices (HICP) and the PPI (harmonized excluding construction) are still showing decelerating trends. PPI prices are decelerating in all sectors. Price weakness is still the main characteristic of producer prices even with the slight rebound in March.

Of the 14 countries listed in the table, only two show prices lower in March and only two more show prices unchanged in March. Two others show prices up by just 0.1% month-to-month. Seven show monthly prices gains of 0.5% or more month-to-month.

Broad price weakness in EMU/EU

But all countries show prices falling over three-month, six-month and 12-month. All but one show prices falling faster over three-month than over six-month (Sweden). Seven of 14 still show faster price drops over six-month than 12-month. Price weakness is widespread across countries in the EMU and the EU and across sectors.

EU Commission cuts outlook

It is no surprise with this ongoing price weakness established that today, the EU Commission cut its growth outlook again. This time it has trimmed the outlook for 2016 to 1.6% from 1.7%, a minor haircut. For 2017, the outlook similarly has been trimmed to 1.8% from 1.9%. This underscores the point we have been trying to make about the Federal Reserve and its shift in language. The Fed did what it did for the monetary policy it wants to run. But the Fed in the U.S. did not give an all-clear signal for growth or economic conditions on the broad global front- far from it.

Other weakness reported

China's manufacturing PMI today in the Caixin survey fell to 49.4 in April from 49.7 in March, as manufacturing continued to contract in China. Malaysia, Ireland and the U.K. also reported worsening in their respective manufacturing surveys.

Mood swings

The dollar continued to retreat moving to a one-year low while stock markets in Asia fell as some sort of growth pessimism has begun to set in. Of course, stock market mood swings come and go. Bipolarism is a common stock market condition and it is not curable.

Still uncertain times

International concerns and downward price pressures are still in play. Oil prices have bounced from their lows and are now range-trading, but there is still no-telling where prices go next or how long they stay there. Markets are wary that OPEC oil producers are playing cat and mouse with them. Small producers are wary of the next big trend. Oil prices are back up where a lot of production makes sense (and dollars) again, but there is still no certainty about how long prices will stick in this region. Starting up, then closing back down can be costly; small firms are wary. The oil patch in the U.S. has become a banking sector disaster; however, with a little bit of higher prices, banks could be extricated from their pain. Still, not that much production has been taken off stream and globally demand is still very slow to recover. The oil glut lingers despite higher prices. Prices are up on speculation not on changed supply-demand conditions.

Global risks linger in the wings

While the global economy is no longer in the middle of an oil and commodity price collapse, a dollar melt up, or a stock market rout, the risks of all those events remain palpable. All the Fed needs to do is to turn on the tightening switch and much of that could come right back. It is not clear if the Fed really accepts that this is true since a number of Fed members still are in denial about why markets had their early year selloff. The Fed does not want that blood on its hands yet if it does not face the cold hard facts that could happen again. And several Fed members are still looking for multiple rate hikes in 2016. Next time the market recovery might not be so swift.

Limits of policy

There is a lot of talking about what can and can't be done. In the end, markets have not been encouraged. Knowing that bankers can always do more QE and that some profess to believe in it has not been much of a backstop to market confidence. Negative rates are too much of a two-edged sword to be wielded with any more gusto. There is a broadening mood swing that seems to grasp that we are in our final days of what bankers can do. If real economic recovery does not catch on soon, the recovery slog could continue to be very slow and extremely protracted. Markets have been positioning for that eventuality for some time despite central bankers' dogged attempts to cheer us up with their gallows humor about using QE and negative rates. Somehow that talk simply has not resonated.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief