Global| Aug 01 2019

Global| Aug 01 2019PMIs Show Preponderant Weakness and Reveal Risks

Summary

The manufacturing PMIs show a great deal of weakness. The quarterly data show clear weakness as the percentage of countries with diffusion readings improving (momentum improving…) is 26% or less over three months, six months and 12 [...]

The manufacturing PMIs show a great deal of weakness. The quarterly data show clear weakness as the percentage of countries with diffusion readings improving (momentum improving…) is 26% or less over three months, six months and 12 months. In addition to that, in the current month, momentum change is neural with a 50% assessment on those improving vs. those deteriorating (the unweighted average reading ticks higher by 0.1 month-to-month). But the number of readings that have a country or regional level diffusion below the 50% mark in July is 11 out of 14. The exceptions are not very strong either: they are Vietnam (52.6), India (52.5), and the United States (51.2). There are nine reading below 50% in June and 8 in May. This has been a rough patch. As yet it is not getting better; it is getting worse. There are no good remedies in sight despite Fed’s recent rate cut since the Fed’s ‘heart’ is not in it.

The manufacturing PMIs show a great deal of weakness. The quarterly data show clear weakness as the percentage of countries with diffusion readings improving (momentum improving…) is 26% or less over three months, six months and 12 months. In addition to that, in the current month, momentum change is neural with a 50% assessment on those improving vs. those deteriorating (the unweighted average reading ticks higher by 0.1 month-to-month). But the number of readings that have a country or regional level diffusion below the 50% mark in July is 11 out of 14. The exceptions are not very strong either: they are Vietnam (52.6), India (52.5), and the United States (51.2). There are nine reading below 50% in June and 8 in May. This has been a rough patch. As yet it is not getting better; it is getting worse. There are no good remedies in sight despite Fed’s recent rate cut since the Fed’s ‘heart’ is not in it.

Over three months the PMI reading averages below a 50% reading in 9 countries/regions; six over six months and five over 12 months. Having five of 14 countries with average PMI readings below 50% for a period of 12 months is not a good situation. Over 12 months the EMU reading itself comes close to being in that group with an average at a dead stop marker of 50.0. The countries with 12-month averages below 50 are China, Malaysia, Taiwan, South Korea, and Turkey. There are a lot of trade-dependent countries in that group.

However, we also rank all the manufacturing PMI data since January 2015. The euro area and Germany (Germany we do not count in our tabulations since it is included in the EMU reading) have their lowest readings of the period in play. The U.K. reading has been weaker only 1.9% of the time. South Korea’s reading has been weaker only 3.7% of the time. Japan has been weaker 14.8% of the time. Taiwan and Turkey have been weaker only 16.7% of the time. There are only three readings at or above their historic medians (with a rank standing of 50 or more) since January 2015.

Against this background we can understand that the Fed, looking at the international scene, sees problems and threats to global growth that could pose a drag on the U.S. economy. However, there has also been yuan weakness that allowed China to avoid a lot the tariff pain from the U.S. although the yuan has since firmed. And there is expected stimulus from the ECB that already has weakened the euro and the pound sterling has been weak as Brexit fears have weighed on it. Currency values are in play. While they mostly seem to be the sort of reactions that have responded to domestic monetary policy, a number of countries, especially the U.S. under Donald Trump, are very wary of the impact of currency movements. Trump came to office in the U.S. promising to fix the broken U.S. trade deficit and to bring jobs back to the U.S. So he has skin in the game over trade results.

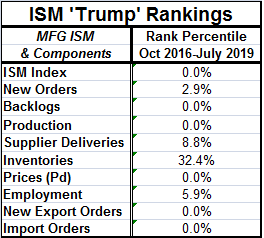

Trade conflict is still in play. The U.S. and China still have tariffs and retaliatory tariffs engaged. China seems to be hurting but let me also show you something about the U.S. economy. The table to the left ranks the just-released ISM index and its components from October 2016 just before Trump was elected. In the six months before Trump’s election, the ISM manufacturing index averaged 51.5. After Trump was elected the ISM began to rise, even before he took office, which is why I rank the ISM linking it to the Trump election date. And since that time, it has been strong. In October 2017, the ISM fell off of its readings as high as 59 and 60 where it has been oscillating for a number of months. It sank to 54 by end-2018. And now it has slipped to 51.2 in July, its weakest reading since August 2016 when Obama was still in office and the economy was moribund. Clearly, the ISM is not performing as it was and the Trump economy is losing momentum and doing so as elections approach. It is not surprising that Mr. Trump is trying to make Mr. Powell the fall guy for this. But U.S. trade war and its spreading influence is an important part of the problem.

Trade conflict is still in play. The U.S. and China still have tariffs and retaliatory tariffs engaged. China seems to be hurting but let me also show you something about the U.S. economy. The table to the left ranks the just-released ISM index and its components from October 2016 just before Trump was elected. In the six months before Trump’s election, the ISM manufacturing index averaged 51.5. After Trump was elected the ISM began to rise, even before he took office, which is why I rank the ISM linking it to the Trump election date. And since that time, it has been strong. In October 2017, the ISM fell off of its readings as high as 59 and 60 where it has been oscillating for a number of months. It sank to 54 by end-2018. And now it has slipped to 51.2 in July, its weakest reading since August 2016 when Obama was still in office and the economy was moribund. Clearly, the ISM is not performing as it was and the Trump economy is losing momentum and doing so as elections approach. It is not surprising that Mr. Trump is trying to make Mr. Powell the fall guy for this. But U.S. trade war and its spreading influence is an important part of the problem.

This comment is not mean to be political as much as it is meant to reveal the underlying dynamics. Mr. Trump is proud of his economic achievements and now the U.S. data show the vaunted job market data are weakening (a relatively weak ADP this week, again). The U.S. has been an important source of global demand and that is now diminished quite apart from the impact of tariffs.

But Trump’s gambit on Free Trade may be the best bet we have to keep growth going if he can win it. Countries have manipulated exchange rates and the U.S. has run unrelenting current account deficits since the early 1980s. That’s over 35 years of deficits. Critics will say that the deficit does not matter. I will respond that that it WOULD NOT MATTER WERE exchange rates determined by market forces. But they are not. That critically changes the analysis and those pat knee-jerk denials. Countries accumulate mounds of foreign exchange reserves to keep from selling their dollars on the exchange market because they do not wish to weaken the dollar and boost their own currency. This may be a more subtle form of market manipulation, but it has been consistent and persistent manipulation that has run amok for over 35 years with great impact on the dollar and on the U.S. economy, an economy that is now wheezing under various strains even as ‘people’ describe it and its mangled job market as ‘strong.’ ‘Strong’ it might have been, but it is no longer.

Now monetary policy is nearly played out in many key money-center countries. Most of Europe, Japan and the U.S. have huge piles of debt that limit the use of fiscal policy…even though it may not seem to be limiting the role of fiscal policy either in fact or in the plans of various administrations (Italy for example, France to some extent, the U.S. for sure) and potential contenders (thinking here of all the Democrat contenders new programs…that will be paid for by taxes…sure they will). China also is now on the excessive debt list. So where will growth come from when you can’t cheat and get it from the U.S. using exchange rate trickery or cut rates anymore or use fiscal policy?

A return to trade policies with lower tariffs and free-market rules and less foreign exchange meddling is probably the best shot we have at real, lasting, stimulus. But in many circles, Trump is a pariah. The Chinese can see that and seem to be dragging their heels in negotiations hoping to bargain with a Democrat eventually instead of with Trump. That, if it is true, will keep the drag from tariffs in play through the elections. Tariffs might even worsen on this sort of ploy. And that could be the death knell for growth in the U.S. and in the global economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief