Global| May 26 2009

Global| May 26 2009Orders in Near Collapse then (Negative) Growth Rates Stabilize

Summary

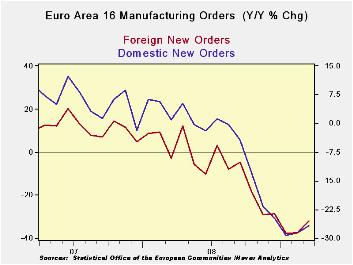

Order trends have deteriorated for both EMU domestic and foreign orders but each series also shows signs of a turn. Three month rates of growth are not as bad as six month rates of growth although six month rates of growth are worse [...]

Order trends have

deteriorated for both EMU domestic and

foreign orders but each series also shows signs of a turn. Three month

rates of growth are not as bad as six month rates of growth although

six month rates of growth are worse than Yr/Yr rates of growth.

February had posted some positive rates of growth for EMU in the month.

Those turned negative in March. But that has been enough to blunt the

slide in the growth rates. Still it is not a picture of growth, rather

it’s a hint of putting the worst behind us – a rather common theme by

now.

Order trends have

deteriorated for both EMU domestic and

foreign orders but each series also shows signs of a turn. Three month

rates of growth are not as bad as six month rates of growth although

six month rates of growth are worse than Yr/Yr rates of growth.

February had posted some positive rates of growth for EMU in the month.

Those turned negative in March. But that has been enough to blunt the

slide in the growth rates. Still it is not a picture of growth, rather

it’s a hint of putting the worst behind us – a rather common theme by

now.

We can also learn something of the EMU situation from the new

details released on German GDP in 2009-Q1

German GDP was rocked in 2009-Q1 by a huge pullback in capital

spending a flow that receded at a 50% annual rate. Exports shrank at a

stunning 34% annual rate and imports fell at nearly a 20% annual rate

(buffering the slide in GDP). The theme of weak investment was extended

by housing where investment fell at a comparatively tepid 10% pace. The

weakness in capital formation spending dropped domestic demand at

nearly a 6.8% annual rate.

Over the past year GDP fell by nearly 7%, a huge Yr/Yr drop,

led by capital formation and export weakness. In the quarter consumer

spending rose but over one year it is lower by just a tick. Germany’s

weakness is not a product of consumer weakness. And with strong social

welfare spending programs the likelihood of keeping a spillover to the

consumer in check is good.

Germany, an important exporting nation, clearly it is

importing a great deal of its weakness from abroad. In that respect it

is encouraging that Germany has seen its orders jump by 3% in March.

That hardly means that the episode of weakness in over. But it suggests

that forces that will put an end to contraction may be in train. That

is just another version of the same story that things are better than

they were but not yet showing growth. Still that is the nature of

recessions as they turn to recovery. You have to look for a gradual

cessation of the slowing and a switch to a period of what will probably

appear to be sporadic growth which then could develop more vigor. We

are now just at the cusp where the declines in growth slow and we only

seen a few scattered signs of growth. We are a ways from seeing

consistent growth and any sort of strength.

| Euro Area 16 and UK Industrial Orders | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Mar-09 | Feb-09 | Mar-09 | Feb-09 | Mar-09 | Feb-09 | ||

| Euro Area Overview | Mar-09 | Feb-09 | Jan-09 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| Total Orders | -0.8% | 0.0% | -2.0% | -11.0% | -38.8% | -44.5% | -48.4% | -31.3% | -32.0% |

| E-16 Domestic MFG orders | -1.5% | 0.8% | -1.2% | -7.2% | -30.3% | -38.6% | -44.9% | -26.8% | -28.5% |

| E-16 Foreign MFG orders | -0.4% | 1.1% | -7.2% | -23.5% | -42.4% | -48.2% | -49.8% | -32.0% | -37.3% |

| Countries: | Mar-09 | Feb-09 | Jan-09 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| Germany (MFG): | 3.3% | -3.3% | -8.0% | -28.8% | -55.2% | -47.4% | -58.1% | -34.5% | -37.5% |

| France (Ind): | -6.7% | 6.7% | -2.5% | -11.3% | 13.8% | -33.7% | -27.9% | -23.9% | -23.2% |

| Italy (Ind): | -2.7% | -2.1% | -3.9% | -29.6% | -27.5% | -39.8% | -39.4% | -29.8% | -31.2% |

| UK (Engineering Ind): | -1.1% | 17.3% | -32.5% | -62.5% | -3.0% | -48.6% | -16.0% | -14.6% | -23.3% |

| German GDP | ||||||||

|---|---|---|---|---|---|---|---|---|

| Consumption | Capital Formation | Domestic | ||||||

| GDP | Private | Public | Total | Housing | Exports | Imports | Demand | |

| % change Q/Q; X-M is Q/Q change in Blns of euros | ||||||||

| Q1-09 | -14.4% | 1.8% | 1.0% | -50.7% | -9.9% | -33.4% | -19.8% | -6.8% |

| Q4-08 | -8.6% | -1.1% | -0.3% | -18.3% | -5.0% | -28.6% | -15.4% | -0.2% |

| Q3-08 | -2.1% | 1.0% | 0.5% | 1.1% | -0.6% | -1.6% | 17.0% | 5.6% |

| Q2-08 | -2.0% | -2.0% | 2.0% | 2.3% | -13.4% | -0.8% | -6.9% | -4.7% |

| % change Yr/Yr; X-M is Yr/Yr change in Gap in Blns of euros | ||||||||

| Q1-09 | -6.9% | -0.1% | 0.8% | -19.7% | -7.3% | -17.5% | -7.3% | -1.6% |

| Q4-08 | -1.8% | -0.6% | 1.5% | -2.4% | 0.3% | -6.3% | 1.2% | 1.9% |

| Q3-08 | 0.8% | -0.4% | 1.9% | 6.5% | 2.0% | 3.2% | 5.2% | 1.5% |

| Q2-08 | 2.0% | -0.4% | 2.1% | 7.8% | 2.8% | 5.4% | 3.9% | 1.1% |

| 5-Yrs | 0.3% | 0.2% | 1.0% | 2.3% | -0.2% | 3.2% | 4.7% | 0.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief