Global| Aug 16 2018

Global| Aug 16 2018On The Heels of a German Rebound, U.K. Retail Sales Show Life; Is This Revival or Denial?

Summary

U.K. retail sales are advancing and accelerating on the heels of a rebound in sales in Germany. It's an unlikely development as the U.K. faces all sorts of challenges including a program of rate hikes from the BOE, ongoing concerns [...]

U.K. retail sales are advancing and accelerating on the heels of a rebound in sales in Germany. It's an unlikely development as the U.K. faces all sorts of challenges including a program of rate hikes from the BOE, ongoing concerns about Brexit and a government that seems in a persistent state of siege. Yet, here it is. It is a solid rebound whether expressed in real or in nominal terms and passenger car registrations are climbing as well.

U.K. retail sales are advancing and accelerating on the heels of a rebound in sales in Germany. It's an unlikely development as the U.K. faces all sorts of challenges including a program of rate hikes from the BOE, ongoing concerns about Brexit and a government that seems in a persistent state of siege. Yet, here it is. It is a solid rebound whether expressed in real or in nominal terms and passenger car registrations are climbing as well.

It is not just the U.K.'s own environment that is challenging but the context of world growth with slowing data out of Europe and trade wars or at least pressures and threats looming. China is slowing. I get more the sense that something is festering than that growth is evolving.

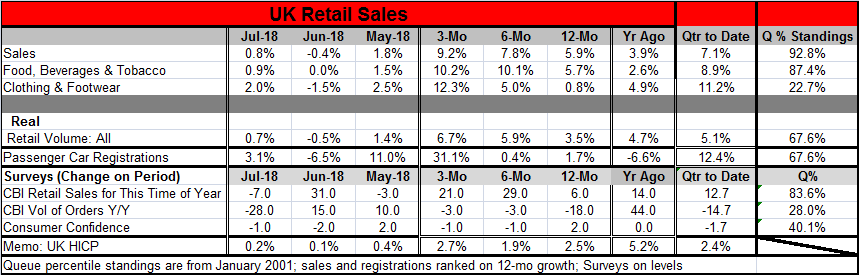

U.K. sales volumes are not on the moon, but they are showing some solid performance. The growth rate of sales on retail volume has a 67th percentile standing among its historic rates of growth. That is solid but not stellar. Passenger car registration's growth rate also has a 67th percentile standing. Nominal sales have a much stronger 92nd percentile standing because inflation is over the top of its range.

Surveys on retail activity show mixed results. The CBI reading on sales for this time of year have a very strong 84th percentile standing. But the assessment on the volume of sales for this time of year is only at a weak 28th percentile. Consumer confidence stands at a well-below-median 40th percentile.

Inflation is at 2.5% over 12 months and at a stronger 2.7% over three months. These metrics may not set the BOE's teeth on edge, but they are not what the bank seeks as a policy goal. The threat/promise of further rate hikes looms.

From stutter to sputter

Global activity data continue to waiver. U.S. data for this week followed the same formula with somewhat surprising strength logged in retail as other measures were faltering like various industrial output gauges and housing. A report that the U.S. and China will have ‘lower level' talks is an indication that the trade restrictions imposed by the U.S. are hurting China and that it is seeking a way out without giving into high profile talks or anything that might look like capitulation. Still, China needs desperately to figure out how to become less strident and standoffish and more of a real member of the international community quite apart from its recent PR stunts- like joining the Paris Accord and pretending purity after defiling the global environment on an unprecedented scale. China's ongoing relations with surrounding countries engaged in its belt and road strategy are another example of disguised Chinese exploitation. Sri Lanka has already surrendered a port to China on a 99-year lease after the Chinese ‘belt and road' improvement debt overwhelmed the country. Beware the belt in the mouth and being railroaded! China is what China does. It seems that the Trump strategy actually may be paying off on China. That is not to suggest that many will admit to liking it, but all too many seem to not even to comprehend what China is doing.

One size fits...none

It's a difficult time to press trade partners over conditions that have existed and evolved in the Post-War period. This economic expansion is relatively long-lived, but it has not been strong. There has been a lot of Post-War evolution that has simply outstripped many of the relationships that have endured. It is inconceivable that the U.S. is still carrying NATO on its back and that Germany is on the sidelines not paying its share and running a fiscal surplus while the U.S. runs a massive fiscal deficit partly because of its huge military expenditures. If there is still a need for a common defense front, it ought to be more of a shared burden… after 50 years? It is also clear that EU and EMU systems that have evolved are not the one-size-fits-all systems that they were touted as. Of course, there have been skeptics from the start. But forcing Italy into a 2% inflation corset has had real costs. The costs to Greece have been more obvious and dramatic. But the social costs in Germany of the noneconomic policies have been enough to untrack the once powerful Angela Merkel and send her to the twilight of her career. One size fits all often turn into one size fits none. But the euro area is in denial and that denial has contributed to these international tensions as well. When the U.K. balked about many of things that continue to vex other EU members, instead of reaching a new agreement the UK voted to exit.

Prospects for growth

As we handicap growth prospects, it is clear that denial remains an important ingredient in all policy. The festering problems of the financial crisis were papered over and a few were dealt with. But credit default swaps are still in full swing and consumer debt levels are high in the U.S. as public debt has soared in China. Despite the obvious message of the financial crisis that the West cannot simply run up debt to absorb output from Asia to drive its growth, Asia keeps trying to shove more down the throat of tiring Mr. Creosote (See Monte Python). Demand in the West can't do that anymore yet China has its belt and road strategy which is designed to grease the skids for Chinese exports not to reorient China's economy for a more developed services sector and improved domestic demand. The financial crisis did not set the world economy on a new course of action has much as it simply diverted the old course by a few degrees. And the election of Mr. Trump in the U.S. and elevation of the Five Star Movement in Italy are part of that diversion. Despite the few obvious changes that have been adopted, all too many of the same old problems and practices remain. Banks are better capitalized. But they are running over the same bumpy roads with improved shock absorbers. And in some places like Italy those improvements were never made, in part, because austerity made it unaffordable. So how long will this run last? Financial crises usually attack the weakest link first then spread. Turkey, anyone? Prosciutto?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief