Global| Jul 08 2015

Global| Jul 08 2015OECD LEIs Show Moderate Growth But Not Upbeat

Summary

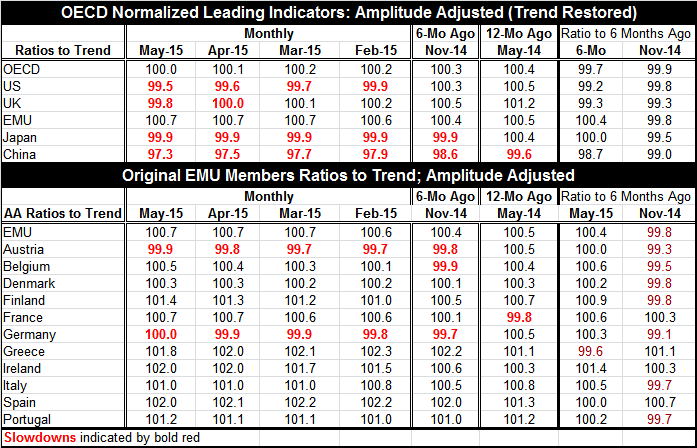

The U.S. is seeing its OECD LEI sink as it has been eroding since June 2014. China has been declining since June 2013. The EMU has been on an upswing and is higher year-over-year. Japan has been stuck with a sub-100 reading for 10 [...]

The U.S. is seeing its OECD LEI sink as it has been eroding since June 2014. China has been declining since June 2013. The EMU has been on an upswing and is higher year-over-year. Japan has been stuck with a sub-100 reading for 10 months.

The U.S. is seeing its OECD LEI sink as it has been eroding since June 2014. China has been declining since June 2013. The EMU has been on an upswing and is higher year-over-year. Japan has been stuck with a sub-100 reading for 10 months.

The EMU region is one of the stronger ones among the largest economies and regions of the world. Yet, among its original members, the highest country reading last year is 102.4. And that reading is from Spain, a country having been recovering rapidly from a very depressed base but still having a long way to go. Despite all the angst about Greece and its economic circumstance, it has been on one of the strongest upswings in the EMU according to its OECD LEI performance. Nevertheless, Greece's LEI has begun to curl lower over the last few months. Conditions in Greece will get worse in the wake of its intransigence and the imposition of capital controls and domestic cash rationing. Prior to that, Greece, however, was making progress.

The U.S., the U.K., Japan, and China all have OECD LEI readings below the neutral value of 100. Among the earliest EMU members, only Austria has an LEI value below 100.

The EMU as a whole is on an upswing but a weak upswing. Germany, the strong economy of Europe, has only an OECD LEI reading of 100. While Germany's index is higher over six months, it is lower over 12 months. Of the 11 EMU nations in the table, 10 are net higher over six months, but only four are higher over 12 months.

The OECD likes to use its indicators by looking at their signal over six months. On that basis, the EMU readings are moving up, but they are still net weaker over 12 months. While the indicators for the EMU and beyond are still consistent with the idea of continuing moderate growth, the momentum is not good and its assessment depends on the horizon of study. That is not reassuring.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief