Global| Nov 09 2020

Global| Nov 09 2020OECD LEIs Claw Their Way to a More Positive Configuration

Summary

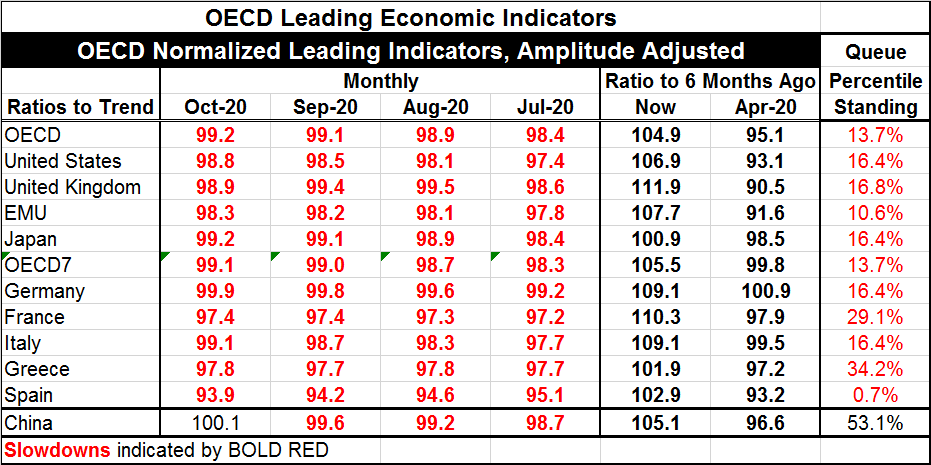

The OECD LEIs remained below 100 in October as they have been for a series of months. Only China poked its head up above the key 100 level in October. China’s index was last above 100 in January 2018. The United States was last above [...]

The OECD LEIs remained below 100 in October as they have been for a series of months. Only China poked its head up above the key 100 level in October. China’s index was last above 100 in January 2018. The United States was last above 100 in December 2018. The EMU was last above 100 in March 2019 (and so on). Clearly the virus is not the only thing that has been causing the OECD LEIs to produce readings that warned of subpar growth. However, the most severe shortfall came in April (February for China) as the virus struck.

The OECD LEIs remained below 100 in October as they have been for a series of months. Only China poked its head up above the key 100 level in October. China’s index was last above 100 in January 2018. The United States was last above 100 in December 2018. The EMU was last above 100 in March 2019 (and so on). Clearly the virus is not the only thing that has been causing the OECD LEIs to produce readings that warned of subpar growth. However, the most severe shortfall came in April (February for China) as the virus struck.

Since their respective low points (mostly April except China and Japan), there has been general recovery across the countries in the table. Spain is the major exception with four declines in a row from July through October. France experienced an LEI drop in October, Greece had one in September. Japan hit its low point in May, not in April. The United Kingdom has had two LEI drops in a row in September and October. Apart from those exceptions, Italy, Germany, the EMU and the U.S. have all seen persistent month-by-month LEI improvement since April; Japan has seen the same since May. China has a string of uninterrupted month-to-month improvements since February – if you trust the data.

Most of the large-scale monthly gains were over by July. August, September and October have produced LEI gains that have been for the most part small and consistent with the exceptions noted above.

The OECD prefers to look at the six-month changes as an indicator or signal. On that basis, this month all countries show gains since April (no surprise there). However, six-months ago every country showed a six-month drop in April (no surprise there either), compared to six-months earlier (except Germany). This month the six-month rule-of-thumb does not get you much insight.

We can also evaluate the current LEI levels with reference to their historic values. The queue standings that rank the October values relative to historic results since mid-1996 find every standing except China’s (where the standing is at 53.1%) is below its historic midpoint (the midpoint is located at the 50% queue ranking mark) and most are below it by quite a bit.

Despite the ongoing and persist nature of recovery the recovery remains far from full. Compared to their best levels since January, only Germany and China are back to best values of the year in October. Italy and Japan are not far behind. Spain, Greece and France lag their peak 2020 LEI levels by the most as of October.

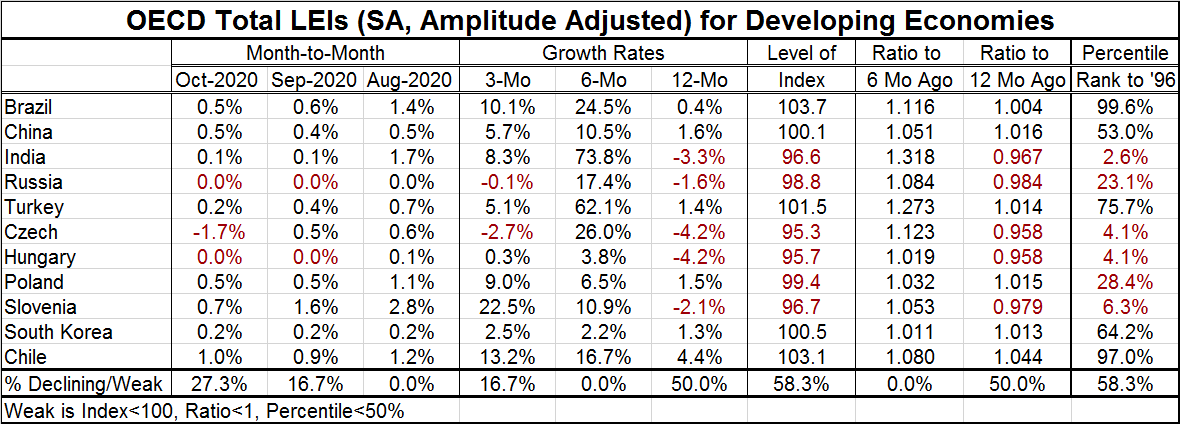

The developing economies show very uneven results. Most show improvements over each of the last three months. Similarly, net improvements over three months and six months are widespread. Performance over 12 months is a mixed bag of results.

The queue percentile rankings of the levels of the LEI readings also finds a mixed bag with six countries substantially below their historic medians and five countries above them with two countries (Brazil and China) with outright strong readings.

Summing up

The bottom line is that the OECD LEIs show that economies, generally developed or developing, are still expanding or were as of October data. Yet, there is a lot of difference on how countries are performing compared to their own historic norms. There is much more weakness than strength. However, the virus has been spreading and counteractions have been taken to try to push the toothpaste back into the tube. We know that there will be some economic slowing as a result of these measures; we just do not know how severe it will be. So far, the LEIs are not calling out much of it as significant. Of course, the actions being taken are designed to be as effective as possible vs. the virus while impacting the economy the least possible. Time will tell how successful these efforts will be. The verdict for now from the LEIs is ‘so far so good.’

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief