Global| Dec 08 2015

Global| Dec 08 2015OECD LEIs Are Stable... But Barely

Summary

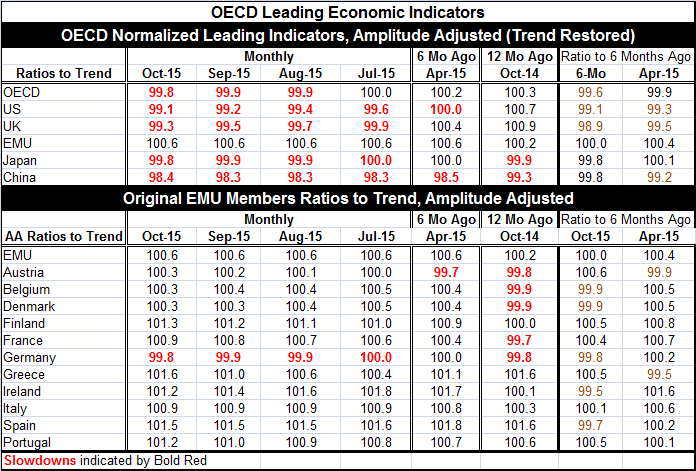

The OECD LEIs show values below the true stable `100' level for the OECD as a whole, for the U.S., for the U.K., for Japan and for China. Only the EMU region has an index above 100, at 100.6 in October. However, the EMU's normal [...]

The OECD LEIs show values below the true stable `100' level for the OECD as a whole, for the U.S., for the U.K., for Japan and for China. Only the EMU region has an index above 100, at 100.6 in October. However, the EMU's normal strongman economy, Germany, has an October reading of 99.8.

The OECD LEIs show values below the true stable `100' level for the OECD as a whole, for the U.S., for the U.K., for Japan and for China. Only the EMU region has an index above 100, at 100.6 in October. However, the EMU's normal strongman economy, Germany, has an October reading of 99.8.

The OECD is holding onto stability' by the grasp of its fingernails. Month-to-month the overall OECD index has slipped as have the indexes for the U.S., the U.K., and Japan. The EMU reading is flat month-to-month. China's index is a tick higher month-to-month but is still the weakest reading of the group.

The EMU region shows values consistently above 100. In fact, its reading has been stable for the last four months and is unchanged from six months ago. All the rest of the countries in the top of the table show a net drop over six months which is the OECD's preferred way to gauge changes in its LEIs. Clearly, there is erosion afoot, but it has been very slow and is only just causing values to decay below the notion of neutrality. The OECD chooses to call this stable, but it is a close call.

Over 12 months all indicators are lower except for the EMU region where the index is higher and for China that is now just a tick higher.

The EMU regions' original members in the table show consistent readings above 100 except for Germany which has been consistently just below 100. However, over six months, Belgium, Denmark, Germany, Ireland and Spain have net lower LEI readings. Over 12 months, Austria and Greece are net lower.

The OECD LEIs help to underline that growth may still be in gear, but that it is walking a fragile line and possibly on a slippery slope. There is no engine of growth in these indicators. Every economy walks a thin line and that is disturbing.

In the EMU, new stimulus has been put on offer, but it did not `wow' the markets. The ECB contends that markets simply have not appreciated what it has done. Clearly, judging from Mario Draghi's remarks, the ECB did all it could do in the presence of opposition from Germany, a country that is already upset by the degree of stimulus the ECB has been able to implement. Of course, the German economy is consistently the best performing economy in Europe. It now has the lowest unemployment rate by far and has one of the highest rates of inflation; Germany does not want more stimulus for itself. The German LEI shows some slowing in train for Germany, but that is a minor consideration for a nation with its lowest unemployment rate since the union was formed.

For the EMU as a whole, including the stellar German results, the unemployment rate has been higher since the union was formed only about one third of the time. But this is largely because of the German weight in the EU. On a country by country basis, only Ireland is doing better than the EMU average standing. Finland's unemployment rate is nearly at the average standing. Austria, France, Italy, Luxembourg, Portugal, the Netherlands -and almost Spain- have their unemployment rates in the top 20% of their historic results since the EMU was formed. Much of the EMU is really in worse shape than the EMU-wide mark.

There is no EMU-wide fiscal policy and many EMU nations are still held to a policy of austerity. More monetary stimulus can only do so much. With the ECB deposit rate already negative and bond yields low, monetary policy would seem to have done about all it can do. But the EMU has no fiscal tools and it has fiscal requirements that disallow most members from taking any stimulative fiscal action.

The Bank of France has just cut its outlook for Q4 growth in the wake of the recent Paris terror attack. There is still a migrant problem to deal with in Europe, and no idea whether countries will be given added fiscal slack for dealing with it. The recent unhinging of oil prices in the wake of last weekend's failed OPEC meeting seems to mean another down draft in oil prices and probably a longer period of oil prices being low and of central banks being below their respective inflation targets. It is not clear what action central banks will take - if any- to counteract this.

Perhaps the most pressing question is whether the Fed, which already is on the glide path to a rate hike, will reconsider now that oil prices have taken a step lower and seem less likely to rise and boost U.S. inflation anytime soon. U.S. inflation is undershooting the Fed's `target' to nearly the same extent that inflation is undershooting the ECB's goal. Has the failed OPEC meeting put Fed policy back in play or not?

A comment yesterday by James Bullard, St. Louis Fed President, was clearly contrary to this idea. Bullard's view is that after the Fed rate hike, the Fed should monitor inflation closely to see if it conforms to its view or not. But why should the Fed raise rates if its policy is not on firm footing? Bullard's comment exemplifies the extent to which the Fed simply wants to act. The Fed may have taken a step too far in the direction of a rate hike to process this new news on oil prices. If so, the Fed has put itself in some dangerous territory. And with the OECD indicators so close to the edge everywhere, a policy mistake in the U.S. would be very costly.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief